Stock Soars as Roche Announces $3.5 Billion Acquisition Deal")

TLDR

- Roche acquired 89bio (ETNB) for $3.5 billion, paying $14.50 per share plus up to $6 per share in contingent value rights

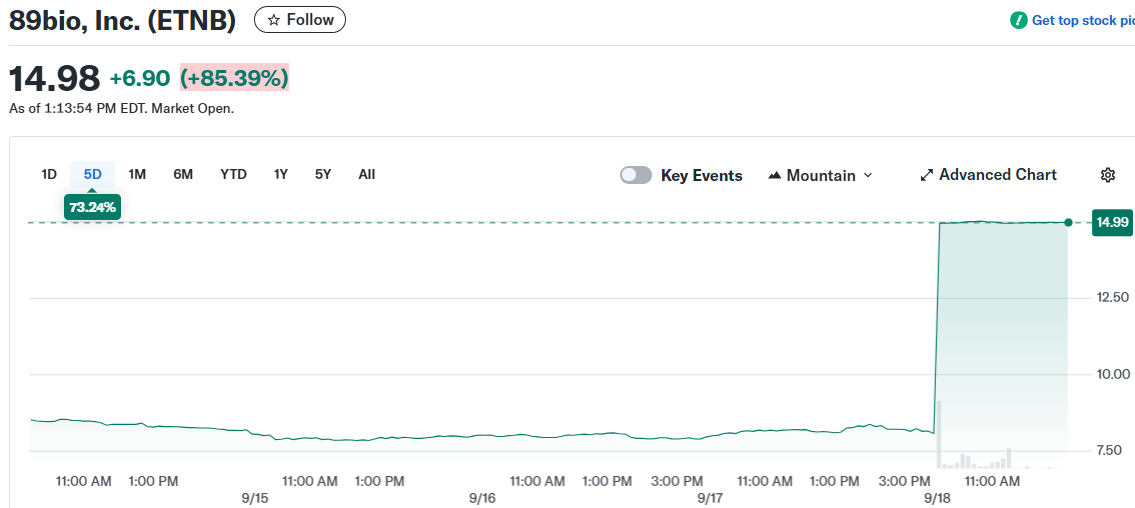

- The deal represents a 79% premium over 89bio’s Wednesday closing price and sent shares soaring 86% on Thursday

- 89bio’s main asset is pegozafermin, a late-stage drug candidate targeting obesity-related conditions like fatty liver disease

- This marks the second major FGF21 therapeutic acquisition after GSK bought Boston Pharma’s similar asset for $1.2 billion in May 2025

- The transaction is structured as a tender offer and expected to close in Q4 2025

Thursday delivered quite the surprise for 89bio shareholders as Roche swooped in with a $3.5 billion acquisition offer. The Swiss pharmaceutical giant agreed to pay $14.50 per share in cash plus contingent value rights worth up to $6 per share.

The deal sent 89bio shares rocketing 86% to $14.99, marking the stock’s largest single-day gain on record. That’s a hefty 79% premium over Wednesday’s closing price, giving investors plenty to smile about.

The upfront cash payment of $14.50 per share totals approximately $2.4 billion. The additional contingent value rights could push the total deal value to $3.5 billion if certain undisclosed milestones are met.

89bio brings one main prize to the table: pegozafermin. This late-stage drug candidate mimics a hormone produced by the liver and targets conditions tied to obesity.

The company has been testing pegozafermin in clinical trials for fatty liver disease and hypertriglyceridemia. While the drug hasn’t secured FDA approval yet, it’s progressing through Phase III studies for Metabolic Dysfunction-Associated Steatohepatitis (MASH).

Roche’s Strategic Play

Boris Zaïtra, head of Roche Corporate Business Development, called pegozafermin a “promising therapy.” The acquisition will fold 89bio into Roche’s pharmaceuticals division once the deal closes.

Roche sees an opportunity to “transform the standard of care” with this addition to their portfolio. The move puts them squarely in competition for the growing obesity treatment market.

UBS analyst Eliana Merle kept her Buy rating and $38 price target on 89bio following the announcement. She views the acquisition as validation of the company’s approach to metabolic diseases.

Market Context

This isn’t the first big move in the FGF21 therapeutic space this year. GSK made waves in May 2025 when it acquired Boston Pharma’s efimosfermin alfa for $1.2 billion upfront.

That deal included up to $800 million in additional milestone payments, showing how competitive this treatment area has become. Both transactions highlight pharmaceutical companies’ appetite for obesity-related therapeutics.

The timing works well for 89bio shareholders who have watched the stock struggle in recent years. The company had been burning through cash while advancing its clinical programs.

89bio’s balance sheet shows more cash than debt, with a current ratio of 15.19 according to recent data. However, the rapid cash burn rate made the Roche offer particularly attractive.

RBC Capital had recently lowered its price target for 89bio to $11 from $12, citing model updates. The bank maintained a Sector Perform rating while noting the ongoing Phase III MASH studies.

Those studies aren’t expected to deliver top-line data until 2027 and 2028, making the immediate Roche buyout a welcome development for investors. The transaction is structured as a tender offer and should close in the fourth quarter of 2025.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants