Stock: Analysts Eye 25% Rally Following Strong Q3 Performance")

TLDR

- Adobe (ADBE) receives Growth Score of B from Zacks with earnings forecast to grow 12.1% and sales 9.6% year-over-year

- Stock positioned for potential 25% rebound according to analysts, with critical support near $350 price level

- Q3 revenue hit record $5.99 billion with growth accelerating to nearly 11%, driven by 12% increase in Digital Media segment

- Company aggressively buying back shares with 5.3% year-over-year reduction in share count and authorization for several more years

- Remaining Performance Obligation (RPO) grew 13% in Q3, indicating strong future revenue pipeline from AI-enabled services

Adobe stock caught investor attention this week as analysts project a potential 25% rebound from current levels. The software giant delivered solid third-quarter results that exceeded expectations across key metrics.

The San Jose-based company reported record quarterly revenue of $5.99 billion in Q3. Revenue growth accelerated to nearly 11% year-over-year, marking a strong performance for the digital media specialist.

Digital Media, Adobe’s core segment, drove much of this growth with a 12% increase. The Digital Experience division posted slightly slower but still healthy 9% growth during the quarter.

Within the consumer and business segments, growth patterns varied. The Business Pro and Consumer group surged 15% year-over-year. The Creative and Marketing Pro group expanded at a more modest 11% rate.

Margin Pressure Offset by Share Buybacks

Adobe faced margin pressure across all levels during Q3. Net income margin decreased by 150 basis points compared to the same quarter last year. However, this decline came in smaller than analysts had anticipated.

The company’s aggressive share buyback program helped offset margin headwinds. Adjusted earnings per share grew by an accelerated 14.2% thanks to the reduced share count.

Adobe repurchased shares at a pace that resulted in a 5.3% year-over-year reduction in outstanding shares. The company maintains authorization to continue this buyback activity for two to three more years.

Strong Balance Sheet Supports Continued Returns

The balance sheet reflects Adobe’s capital return strategy. Year-to-date reductions in cash and total assets coincided with increased debt levels. Treasury shares increased as the company bought back stock.

Despite the leverage changes, Adobe maintains a fortress-like financial position. Long-term debt sits at approximately 0.5 times equity and 1.25 times cash holdings.

The company generated positive cash flow during Q3. Cash flow growth reached 13.6% with expectations for 11.9% expansion in 2025.

Forward Guidance Beats Expectations

Adobe raised its full-year guidance following the strong Q3 performance. The updated targets for Q4 include both revenue and earnings per share estimates above analyst consensus.

Management expects Q4 revenue growth of approximately 9%. This guidance appears conservative given the current momentum and growing pipeline of contracted business.

Remaining Performance Obligation (RPO) grew 13% in Q3. This forward-looking metric indicates strong future revenue from existing contracts and subscriptions.

Analysts revised their earnings estimates higher following the results. Two analysts increased their fiscal 2025 projections in the past 60 days. The Zacks Consensus Estimate rose $0.02 to $20.65 per share.

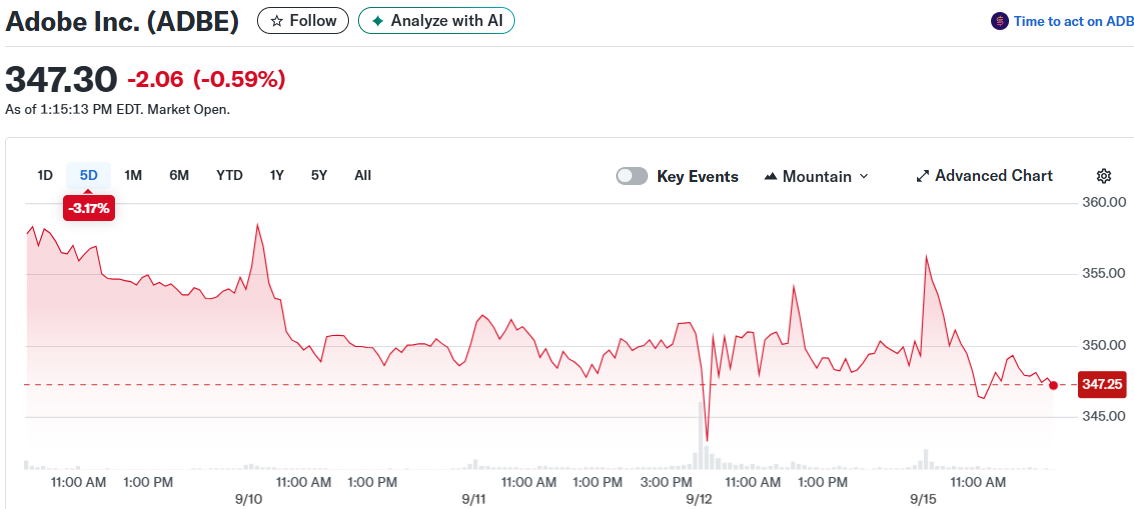

Technical Analysis Points to Support

Chart analysis reveals Adobe stock finding support near the $350 level. MACD and stochastic indicators show bullish signals developing.

The stochastic indicator presents particularly strong signals suggesting buyers have regained control. This technical setup aligns with the fundamental improvements in the business.

Institutional investors own more than 80% of Adobe shares and have been net buyers throughout 2025. This ownership base provides solid support for any potential rebound.

Adobe maintains a Zacks Rank #3 (Hold) rating with a Growth Style Score of B. The VGM Score rates at A, reflecting strong value, growth, and momentum characteristics.

The company’s average earnings surprise stands at 2.5% over recent quarters. RPO growth of 13% in Q3 could accelerate further as AI-assisted features become more mainstream across Adobe’s product suite.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants