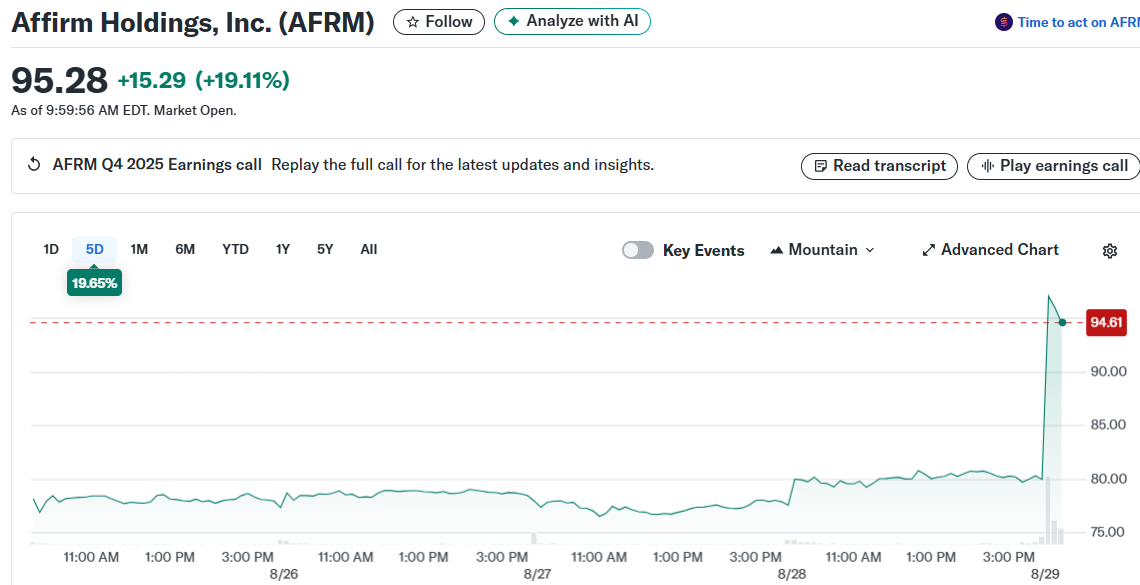

Stock: Surges 15% on Strong Q4 Beat and Bullish 2026 Outlook")

TLDR

- Affirm stock jumped 15% premarket after Q4 revenue of $876.42 million beat estimates of $837.05 million

- Company turned profitable with $69.2 million net income versus $45.2 million loss year-over-year

- GMV grew 43% to $10.4 billion while active consumers increased 24% to 23 million users

- Fiscal 2026 GMV forecast above $46 billion exceeds Wall Street consensus of $45.67 billion

- Brokerages raised price targets with Jefferies lifting target to $110 from $95

Affirm stock rocketed 15% in premarket trading Friday after the buy-now-pay-later company crushed fourth-quarter expectations. The strong results showcase resilient consumer spending and robust platform growth.

The company reported Q4 revenue of $876.42 million, easily beating analyst estimates of $837.05 million. This represents strong momentum for the BNPL platform as consumers continue embracing flexible payment options.

Affirm achieved a major milestone by swinging to profitability. The company posted net income of $69.2 million compared to a $45.2 million loss in the same quarter last year.

Platform Metrics Show Strong Growth

Affirm’s core business metrics demonstrated impressive expansion. Gross merchandise volume surged 43% to $10.4 billion as more consumers used the platform for purchases.

Active consumers grew 24% to reach 23 million users. The merchant network also expanded with 377,000 active partners, up 24% year-over-year.

Direct-to-consumer GMV jumped 61% to $3.1 billion. The Affirm Card drove much of this growth with GMV increasing 132% to $1.2 billion.

Growth came from multiple categories including general merchandise, electronics, travel, and fashion. This diversification shows Affirm’s broad appeal across consumer spending segments.

Bullish 2026 Forecast Drives Optimism

Affirm provided an upbeat outlook for fiscal 2026. The company forecasts GMV above $46 billion, exceeding Wall Street consensus of $45.67 billion.

Revenue is expected to represent 8.4% of GMV in fiscal 2026. First-quarter revenue guidance ranges between $855 million and $885 million.

BTIG analysts remain optimistic about Affirm’s trajectory. They expect GMV growth to continue above 30% annually and believe the company can match traditional credit card providers in size.

Analyst Upgrades Follow Strong Results

Multiple brokerages raised price targets following the earnings beat. Jefferies increased its target to $110 from $95, while J.P.Morgan also boosted its forecast.

The median analyst price target rose to $75 from $66 in May. Currently, no analysts recommend selling Affirm shares according to LSEG data.

Affirm stock has gained 31% year-to-date, outperforming the S&P 500’s 11% advance. If premarket gains hold, shares will reach their highest level in over three years.

CEO Max Levchin emphasized that profitability marks just one milestone in Affirm’s journey. The company continues targeting its massive addressable market opportunity in consumer payments.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants