Stock: Surge 19% on AI Growth and Analyst Upgrades")

TLDR

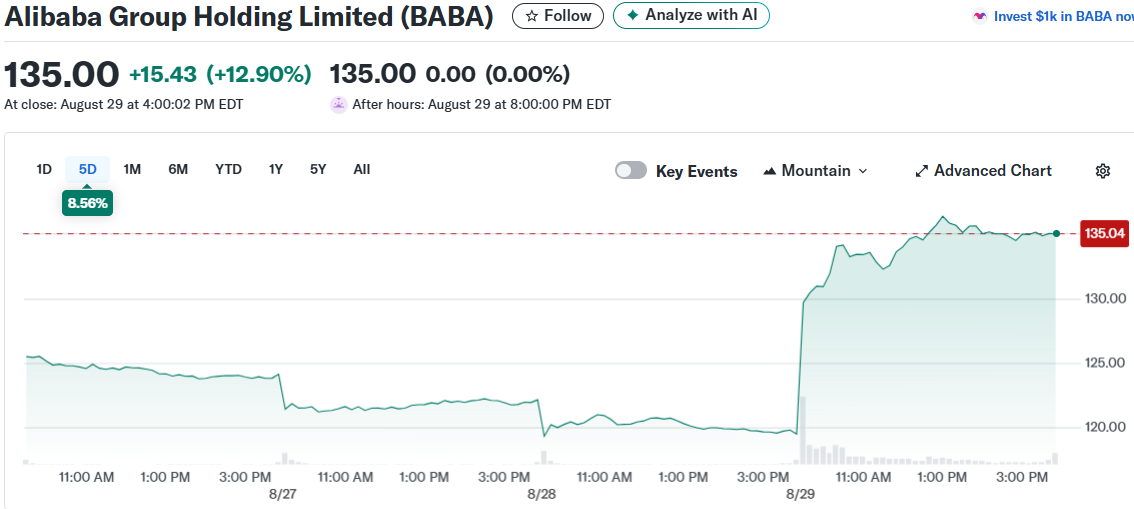

- Alibaba stock jumped 12.9% after Q1 results beat profit expectations with $2.06 earnings per ADS

- Cloud revenue grew 26% to 33.4 billion yuan while AI revenue doubled for eighth straight quarter

- Goldman Sachs, JPMorgan, and Bernstein all raised price targets following strong performance

- New AI chip development report adds momentum to stock’s 19% gain in Hong Kong trading

- Analysts maintain Strong Buy rating with average price target implying 13% upside potential

Alibaba stock rocketed higher after delivering strong first-quarter fiscal 2026 results that showcased the company’s growing dominance in cloud computing and artificial intelligence.

The Chinese e-commerce giant reported adjusted earnings of $2.06 per American depositary share, surpassing analyst expectations of $1.98. Revenue reached 247.7 billion yuan ($34.6 billion), slightly below forecasts but investors focused on the positive growth metrics.

Cloud revenue emerged as the standout performer, climbing 26% year-over-year to 33.4 billion yuan. This growth demonstrates Alibaba’s successful expansion beyond traditional e-commerce into higher-margin technology services.

AI Revenue Powers Growth Engine

Alibaba’s AI segment delivered exceptional results with revenue more than doubling from the previous year. This marks the eighth consecutive quarter of triple-digit percentage growth in AI-related products.

The company competes directly with Chinese tech rivals including Baidu, DeepSeek, and Tencent in developing advanced AI models. Reports suggest Alibaba has created a new AI chip capable of handling broader tasks than previous processors.

This chip development could help reduce dependence on restricted Nvidia hardware, giving Alibaba more control over its AI infrastructure. The timing aligns with China’s push for technological self-reliance in critical sectors.

Wall Street Raises Price Targets

Goldman Sachs analyst Ronald Keung boosted his price target to $163 from $147, maintaining a Buy rating. Keung highlighted Alibaba’s transformation into an “AI + everyday consumption app” and “AI + Cloud hyperscaler.”

JPMorgan’s Alex Yao set the highest target at $170, up from $140, keeping an Overweight rating. Yao expects food delivery losses to narrow as operations reach efficient scale similar to competitor Meituan.

Bernstein’s Robin Zhu increased his target to $160 from $145, noting Alibaba now serves 300 million monthly quick commerce customers with 80 million daily orders processed by over 2 million riders.

Trading Performance and Outlook

Alibaba shares closed up 19% in Hong Kong trading, catching up with Friday’s gains in American depositary receipts. The stock has risen 36% since being featured as a Barron’s pick in October 2024.

Analysts maintain overwhelmingly positive sentiment with 12 Buy ratings and one Hold rating, creating a Strong Buy consensus. The average price target of $152.63 suggests approximately 13% upside from current levels.

Quick commerce customer growth reached 300 million monthly users while Taobao daily users expanded 20%. Food delivery unit losses could be cut in half by October as operational efficiency improves.

The latest results reinforce Alibaba’s strategic pivot from pure e-commerce to a technology-focused conglomerate leveraging AI and cloud services for future growth.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants