TLDR

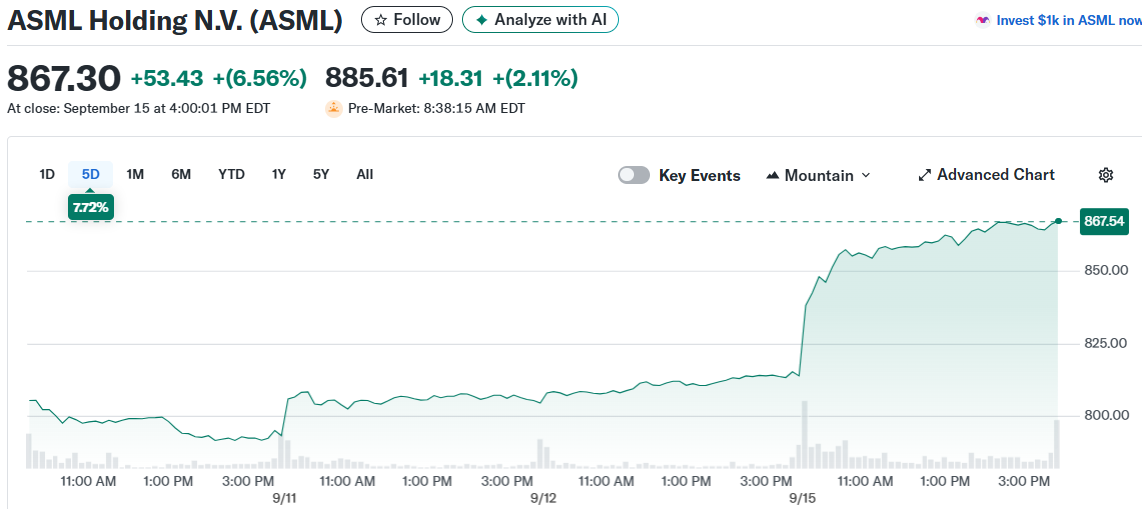

- ASML stock jumped 6.6% Monday following Arete Research upgrade to buy after seven years

- J.P. Morgan maintains top pick status, says worst quarter is behind the company

- Taiwan Semiconductor expected to increase spending from $38-42B to $50B in 2026-2027

- Strong AI demand from Nvidia and hyperscale customers driving equipment orders

- Stock trades below historical valuation despite EUV lithography monopoly position

ASML shares soared 6.6% Monday as Wall Street analysts expressed renewed confidence in the Dutch semiconductor equipment maker. The rally came after Arete Research issued its first buy rating on ASML in seven years.

The upgrade signals a major shift in sentiment for a stock that had underperformed this year. ASML’s monopoly position in extreme ultraviolet lithography technology makes it essential for producing AI chips.

Customer Spending Plans Drive Optimism

The bullish analyst calls center on expected spending increases from key customers. Taiwan Semiconductor Manufacturing is projected to boost capital expenditures to $50 billion in both 2026 and 2027.

This represents a jump from TSMC’s current $38-42 billion spending range. The foundry giant has already shown strong momentum with 37% year-over-year revenue growth through August 2025.

TSMC’s 2-nanometer process ramp and Nvidia’s expected adoption of the A16 process should increase EUV requirements. This creates a direct path for stronger ASML orders heading into 2027.

J.P. Morgan analysts note that ASML’s worst quarter appears behind it. They maintain their top pick status despite ongoing caution around 2026 growth prospects.

Memory Market Provides Additional Growth

Beyond logic chips, the memory segment offers another tailwind. High-bandwidth memory demand continues surging due to AI applications.

DRAM pricing remains strong supported by tight supply-demand dynamics. The environment is expected to persist until new capacity comes online in 2027.

Samsung could provide an additional catalyst. If the Korean company qualifies HBM4 memory with Nvidia, it would trigger increased capital spending that benefits ASML.

Valuation Appears Attractive

ASML’s valuation had fallen to 10-year lows during the summer weakness. The stock trades below its historical 30-35 times earnings multiple despite its dominant market position.

The company’s lithography market share is expected to exceed 80-89%. Higher EUV average selling prices are driving this expansion.

Uncertainty around trade restrictions had weighed on shares. However, no tariffs were imposed on semiconductor equipment shipments into the U.S.

ASML is expected to begin receiving orders for planned U.S. manufacturing capacity. AI spending from Nvidia, Broadcom and cloud providers remains robust.

The shift to High-NA EUV technology starting in 2026 should increase lithography requirements. This supports greater EUV adoption across both logic and memory manufacturing.

J.P. Morgan maintains a 822 euro price target based on 32 times 2027 earnings estimates. Analysts expect the market will focus on 2027 trends once ASML provides 2026 guidance in October.

TSMC reported strong momentum through August with analysts expecting the trend to continue. The foundry’s success directly translates to equipment demand for ASML given their close partnership.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants