TLDR

- Axon Enterprise (AXON) reported Q3 2025 revenue of $711 million, up 31% year-over-year, marking the seventh straight quarter of growth above 30%

- Software and Services revenue jumped 41% to $305 million while Annual Recurring Revenue climbed 41% to $1.3 billion

- The company raised full-year revenue guidance to $2.74 billion from the previous range of $2.65-$2.73 billion

- Axon announced acquisitions of Prepared and Carbyne to create Axon 911, entering the emergency call-handling market worth $5 billion

- TD Cowen maintained a Buy rating with a $925 price target following the earnings report

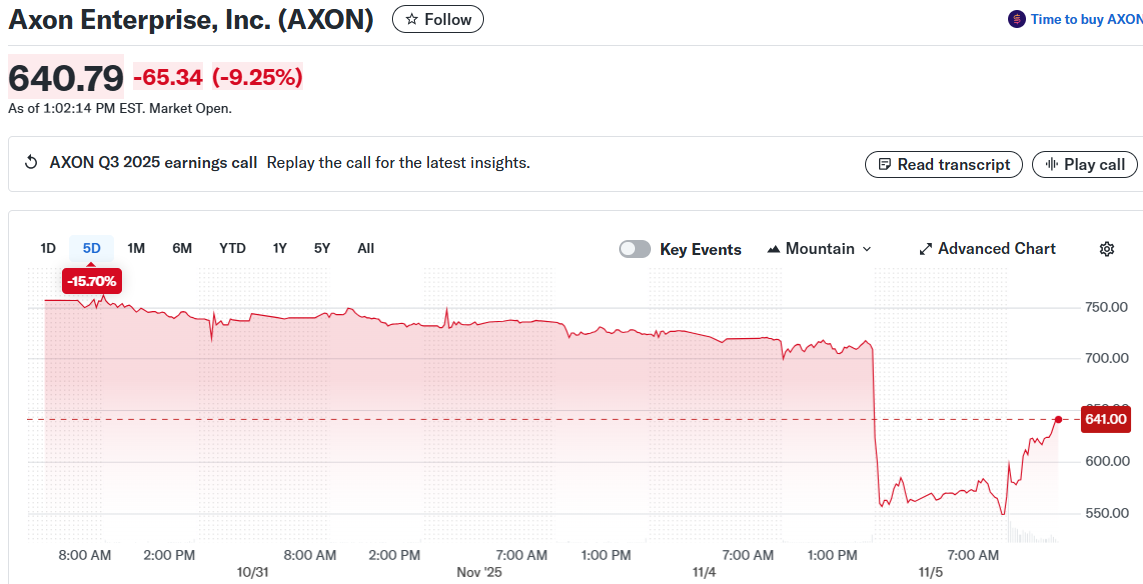

Axon Enterprise posted Q3 2025 revenue of $711 million, representing 31% growth compared to the same period last year. The result exceeded analyst expectations of 29.5% growth.

This marks the seventh consecutive quarter where the company has grown revenue by more than 30%. The performance comes as Axon continues expanding its public safety technology products.

Software and Services revenue reached $305 million, up 41% from last year. Annual Recurring Revenue grew at the same pace to hit $1.3 billion.

Net revenue retention stood at 124% for the quarter. Connected Devices revenue increased 24% to $405 million.

TASER revenue came in at $238 million, up 17% year-over-year. Personal Sensors brought in $107 million, a 20% increase.

Platform Solutions revenue jumped 71% to $61 million. The company reported a GAAP net loss of $2 million, or negative 0.3% margin.

Non-GAAP net income reached $98 million with an Adjusted EBITDA of $177 million. The Adjusted EBITDA margin came in at 24.9%.

New Product Launches and Acquisitions

Axon introduced the Body Workforce Mini in September. The compact camera is designed for commercial environments including retail, healthcare, and logistics.

Early deployments in the U.S. and Canada are expected in the first half of 2026. General availability is planned for mid-year 2026.

The company completed its acquisition of Prepared and signed an agreement to buy Carbyne. These deals form the foundation of Axon 911, a new emergency response system.

Financial Guidance and Market Position

Axon raised its full-year revenue outlook to $2.74 billion. The previous guidance ranged from $2.65 billion to $2.73 billion.

This represents 31% annual growth for 2025. Fourth quarter revenue is expected between $750 million and $755 million.

Fourth quarter Adjusted EBITDA guidance sits between $178 million and $182 million. That represents a 24% margin.

TD Cowen maintained its Buy rating on the stock with a $925 price target. The firm noted the third-quarter beat was smaller than previous quarters due to timing issues.

Management expects full-year bookings growth in the high-30% range. The company’s AI Era plan is projected to represent over 10% of full-year Software and Light bookings.

The Prepared and Carbyne acquisitions add $5 billion to Axon’s addressable market. The combined market opportunity now exceeds $74 billion across all product categories.

Axon held $2.4 billion in cash and short-term investments as of September 30. Outstanding debt totaled $2.0 billion, resulting in a net cash position of $356 million.

Operating cash flow reached $60 million in the quarter, down from $91 million the previous year. Free cash flow came in at $33 million.

Total gross margin was 60.1%, down 70 basis points year-over-year. Adjusted gross margin decreased 50 basis points to 62.7%, affected by global tariffs and product mix changes.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants