Stock: Strong AI Growth and Analyst Upgrade Drives 33% Rally")

TLDR

- Baidu stock has climbed 33% since July to $115, driven by AI Cloud growth and robotaxi expansion

- Arete upgraded Baidu from Sell to Buy with a price target increase from $71 to $143

- AI Cloud revenue surged 42% year-over-year to RMB 6.7B, now over 25% of core revenue

- Apollo Go robotaxi service expanded to 15 cities globally with 1.4 million quarterly rides

- Company completed CNY4.4 billion senior notes offering for general corporate purposes

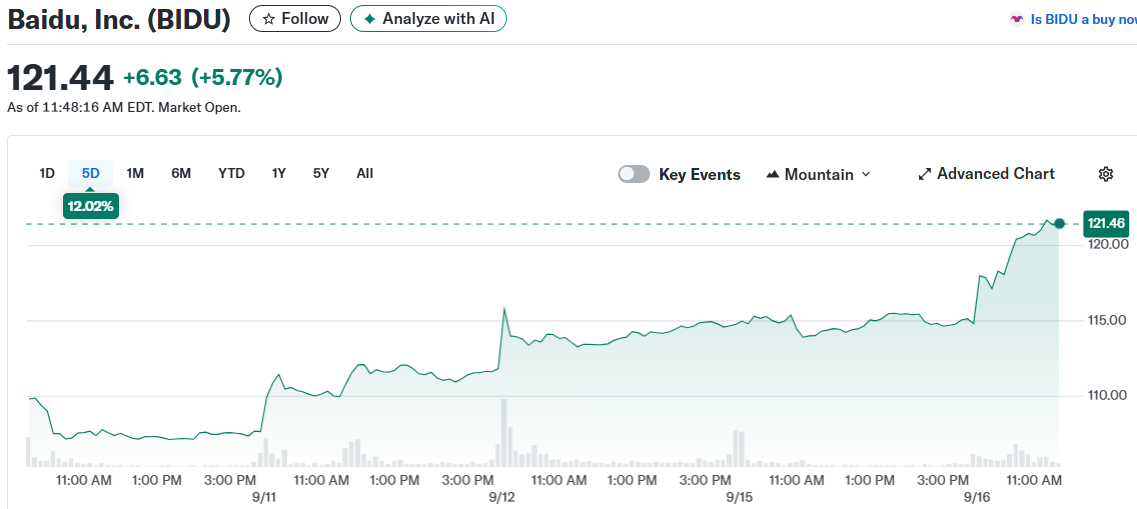

Baidu stock has staged an impressive comeback, climbing more than 33% since July to reach $114.82. The Chinese tech giant’s market cap expanded from $29.9 billion to $40.6 billion during this period.

The rally comes as investors embrace Baidu’s pivot toward artificial intelligence and autonomous driving. Forward price-to-earnings ratio has risen to 12.3x from single digits just two months ago.

Despite the gains, BIDU still trades at a steep discount to U.S. tech peers. Alphabet trades at around 25x forward earnings while Microsoft commands multiples above 30x.

Baidu launched its Ernie X1.1 model in September with improved reasoning accuracy. Management claims the AI model outperforms OpenAI’s GPT-5 and Alphabet’s Gemini 2.5 Pro in key metrics.

Enterprise customers can now access Ernie X1.1 through Baidu Cloud services. This direct monetization path validates the company’s AI strategy pivot.

AI Cloud Business Shows Strong Momentum

AI Cloud revenue jumped 42% year-over-year to RMB 6.7 billion in the second quarter. This translates to roughly $922 million and represents more than 25% of Baidu Core revenue.

The growth rate demonstrates strong enterprise demand for Baidu’s AI services. Cloud computing has become a key revenue driver as traditional advertising struggles.

Baidu’s cloud infrastructure supports both internal AI development and external customer needs. The dual-purpose approach helps maximize return on technology investments.

Robotaxi Operations Scale Globally

Apollo Go robotaxi service reached 1.4 million quarterly rides, up 75% year-over-year. The platform now operates in 15 cities worldwide including new markets in Dubai and Abu Dhabi.

Baidu claims to run the most scaled autonomous vehicle fleet globally. The RT6 vehicle costs under $30,000 per unit to produce, providing a cost advantage over competitors.

The company secured a partnership with CAR Inc. for asset-light monetization. This approach reduces capital requirements while expanding service reach.

Traditional advertising revenue continues to decline as digital marketing shifts. Online marketing revenue fell 15% year-over-year in the second quarter.

Total revenue came in at RMB 32.7 billion, down 3.6% year-over-year. The decline reflects ongoing challenges in Baidu’s legacy search advertising business.

However, the company maintained strong profitability with a 20.9% net margin. Earnings per share reached RMB 10.94 for the quarter.

Analyst consensus for third-quarter EPS stands at 9.96, well below last year’s RMB 16.6. The lower expectations reflect advertising headwinds and increased AI investment costs.

Arete Research upgraded Baidu from Sell to Buy rating this week. The firm also raised its price target from $71 to $143, citing AI momentum and robotaxi potential.

Baidu completed a CNY4.4 billion senior notes offering on September 15. The unsecured notes mature in 2029 and were sold to offshore non-U.S. investors.

Proceeds will fund general corporate purposes including debt repayment and interest payments. The notes are expected to list on the Hong Kong Stock Exchange on September 16.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants