TLDR

- Nvidia controls 90% of AI training GPU market with $41.1 billion in data center revenue last quarter

- IBM has generated $7.5 billion in AI business through consulting services as 95% of AI pilots fail at companies

- Intel struggles in AI accelerators but sees potential in foundry business with Intel 14A process coming in 2027

- Meta gives away free LLaMA AI models while earning $46.6 billion quarterly from AI-powered advertising

- Amazon’s AWS captures 31% of cloud infrastructure spending with AI services driving growth

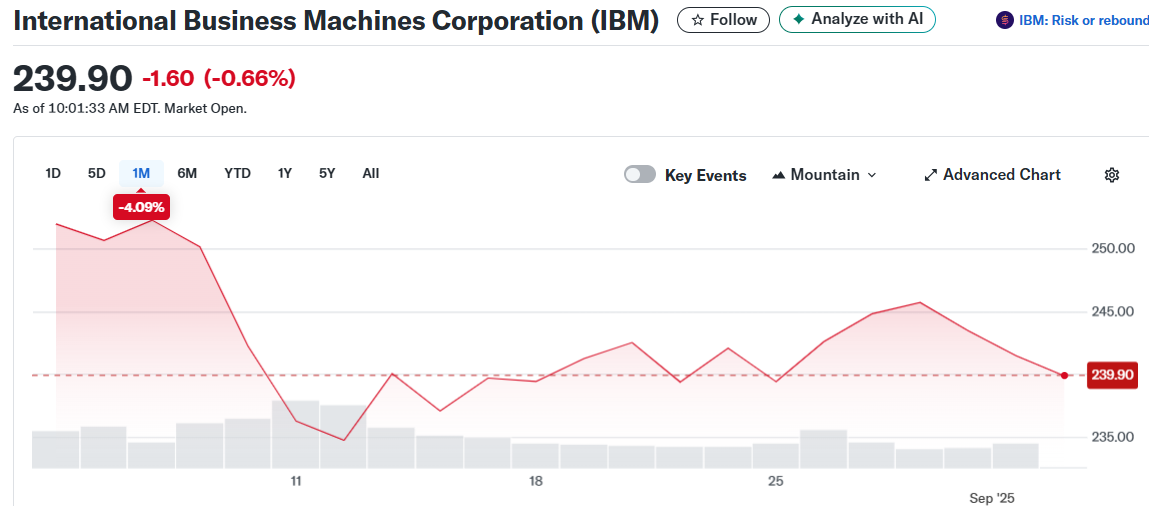

IBM and Intel emerge as compelling AI investment options despite different approaches to the artificial intelligence market. IBM has found success by focusing on practical AI implementation for enterprise clients, while Intel looks toward manufacturing opportunities in the foundry business.

IBM’s strategy centers on solving real-world business problems with AI technology. The company has generated $7.5 billion in AI business, with most revenue coming from its consulting division. This approach addresses a critical market gap, as 95% of AI pilots at companies fail to produce results according to MIT research.

The company pairs consulting services with software solutions to help enterprises implement AI successfully. This combination creates a valuable service offering as businesses shift from experimental AI deployments to projects focused on return on investment.

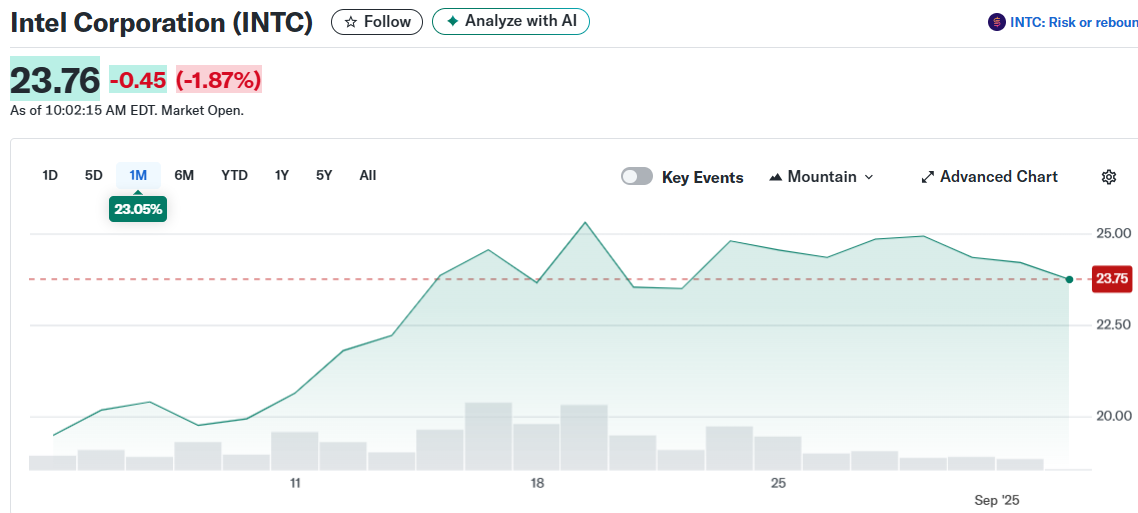

Intel faces different challenges in the AI market. The company’s AI accelerator efforts have struggled, with Gaudi AI chips selling poorly and the next-generation Falcon Shores project cancelled. New CEO Lip-Bu Tan acknowledges Intel may be too late to compete in AI training markets dominated by Nvidia.

Intel’s Foundry Opportunity

However, Intel sees potential in semiconductor manufacturing for custom AI chips. Many technology companies are designing their own AI processors to reduce costs for AI inference workloads. Companies like Alphabet need cheaper alternatives to running AI models in their core services.

Intel’s foundry business could benefit if the Intel 14A manufacturing process succeeds. Expected in 2027, this process represents Intel’s opportunity to win external customers for chip manufacturing. The U.S. government’s investment in domestic semiconductor production could help Intel attract customers.

Market Leaders Maintain Dominance

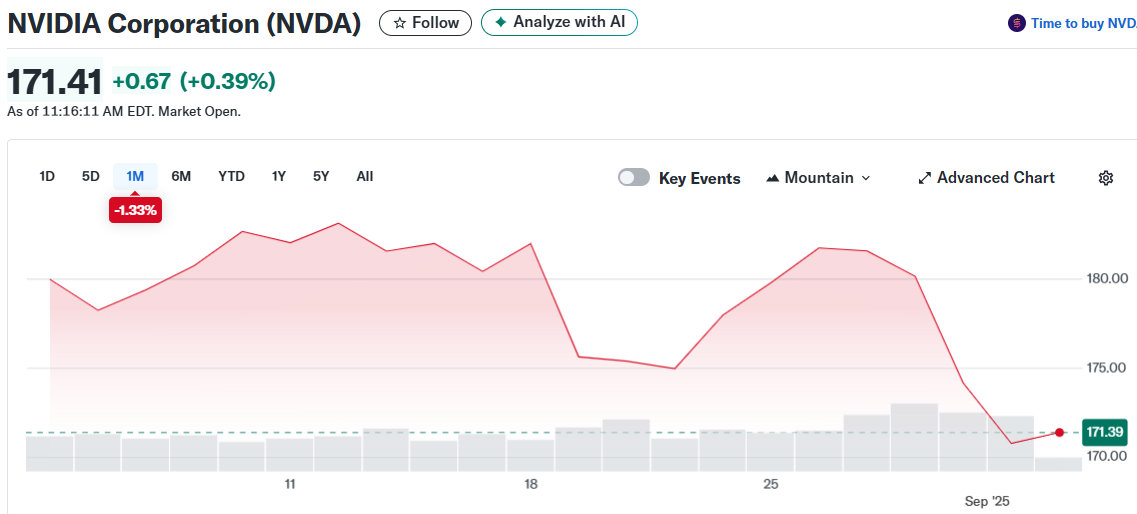

Nvidia continues to dominate AI infrastructure with over 90% of the AI training GPU market. The company reported $46.7 billion in total revenue for Q2 fiscal 2026, up 56% year over year. Data center revenue reached $41.1 billion, driven by strong demand for AI chips.

Nvidia’s Blackwell architecture is sold out through 2026, with major customers including Microsoft, Alphabet, and Meta placing large orders. The company maintains competitive advantages through its CUDA programming platform, which has 5 million trained developers.

Meta takes a different approach by offering free LLaMA AI models while monetizing through advertising. The company generated $47.5 billion in Q2 2025 revenue, with $46.6 billion from advertising. Meta’s 3 billion daily users provide training data that competitors cannot replicate.

Amazon’s AWS leads cloud infrastructure with 31% market share and $30.9 billion in Q2 revenue. The company offers Trainium and Inferentia chips as alternatives to Nvidia processors, providing customers with 40% cost savings. AWS maintains a $195 billion backlog of multiyear contracts.

Intel’s foundry business remains unproven with no major external customers for the Intel 18A process, making the 2027 Intel 14A launch critical for the company’s AI strategy.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants