Shares Drop Following Wall Street Downgrade. Here’s Why")

TLDR

- Jefferies downgraded Bloom Energy from Hold to Underperform with a $31 price target

- Stock trades at 31 times estimated 2027 EBITDA compared to 20 times for industry peers

- Company faces 620 MW capacity shortfall even with confirmed Oracle and AEP orders

- Infrastructure constraints like gas pipeline delays limit deployment speed

- Bank of America also cut price target to $24, citing fundamentals don’t support current valuation

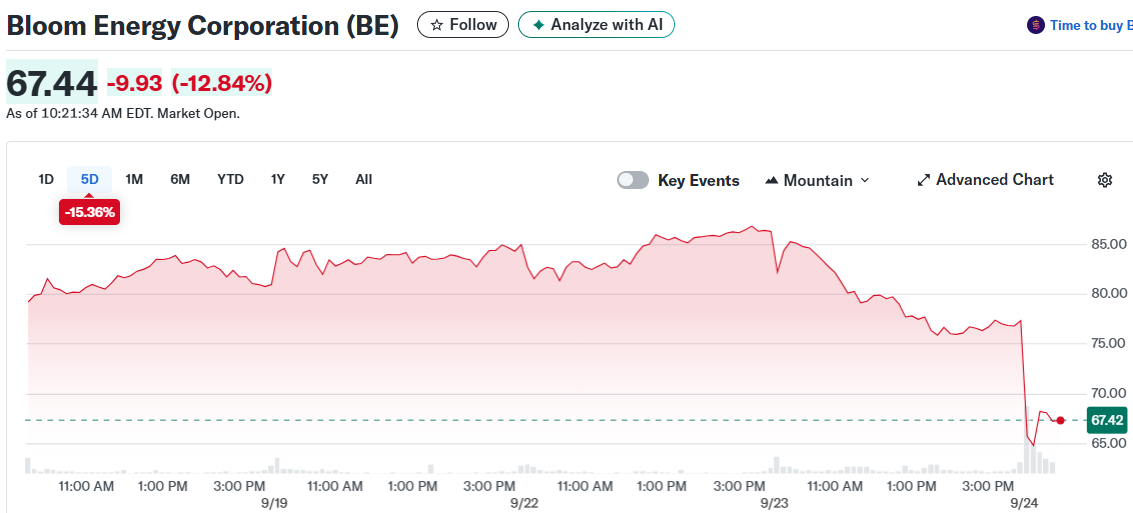

Bloom Energy took a hit Tuesday morning as shares dropped 7% in pre-market trading following a downgrade from Jefferies. The investment bank cut its rating from Hold to Underperform, citing rich valuations that have outpaced the company’s fundamentals.

The fuel cell company has been riding high on AI data center enthusiasm. But analysts are starting to question whether the stock surge makes sense given the business realities.

Jefferies slapped a $31 price target on the stock. That’s well below where shares have been trading recently at around $72.

The investment bank isn’t alone in its skepticism. Bank of America has also turned bearish, slashing its price target to just $24.

Valuation Disconnect

The core issue appears to be valuation. Bloom trades at about 31 times estimated 2027 EBITDA. That’s a hefty premium to hyperscalers and grid equipment peers, which trade around 20 times.

“Given the limited visibility into post-2026 growth and some early signs of over-exuberance, we find that risks to the downside outweigh further upside at the current levels,” Jefferies analysts wrote.

The analysts question whether Bloom can deliver the aggressive expansion needed to justify current prices. Even with major orders from Oracle and American Electric Power, the company faces challenges.

Oracle has committed to 200 megawatts while AEP signed up for 300 MW. But Jefferies calculates this still leaves Bloom about 620 MW short of fully utilizing its 2 GW production capacity.

The firm doesn’t expect Bloom to hit 1 GW in annual sales anytime soon. Their estimate puts that milestone at 1.3 GW by 2029.

Infrastructure Hurdles

Bloom’s fuel cells can deploy quickly – just 90 days for installations up to 50 MW. This speed has impressed investors betting on rapid data center buildouts.

But infrastructure reality is more complex. Gas pipeline constraints are slowing actual deployments.

Take AEP’s Ohio project as an example. The fuel cells can’t go online until a gas pipeline is ready in 2027.

Financial Picture

The company reported trailing twelve-month sales of $1.63 billion. Revenue growth has been modest at 5% over three years.

Operating margins sit at 4.45% while net margins are just 1.45%. The gross margin looks healthier at 30.3%.

Bloom maintains strong liquidity with a current ratio of 4.99. However, the debt-to-equity ratio of 2.56 shows heavy reliance on debt financing.

The stock carries a high beta of 3.79, making it sensitive to market swings. With institutional ownership at nearly 90%, any sentiment shifts can move shares quickly.

Bloom Energy closed Monday’s regular session before the downgrade news hit. The pre-market drop reflects investor concern about stretched valuations in a company that still faces execution challenges despite its data center positioning.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants