Stock Receives Strong Buy Rating from 25 Wall Street Analysts")

TLDR

- Broadcom (AVGO) reported strong Q3 2025 results with revenue up 22% year-over-year to $15.95 billion

- AI revenue jumped 63% to $5.2 billion, with CEO predicting $6.2 billion in Q4

- Stock surged 10% after earnings, up nearly 140% over the past twelve months

- Top investor Daniel Sparks warns against expecting Nvidia-like explosive growth

- Analysts maintain Strong Buy rating with 25 Buy ratings and average price target of $375.58

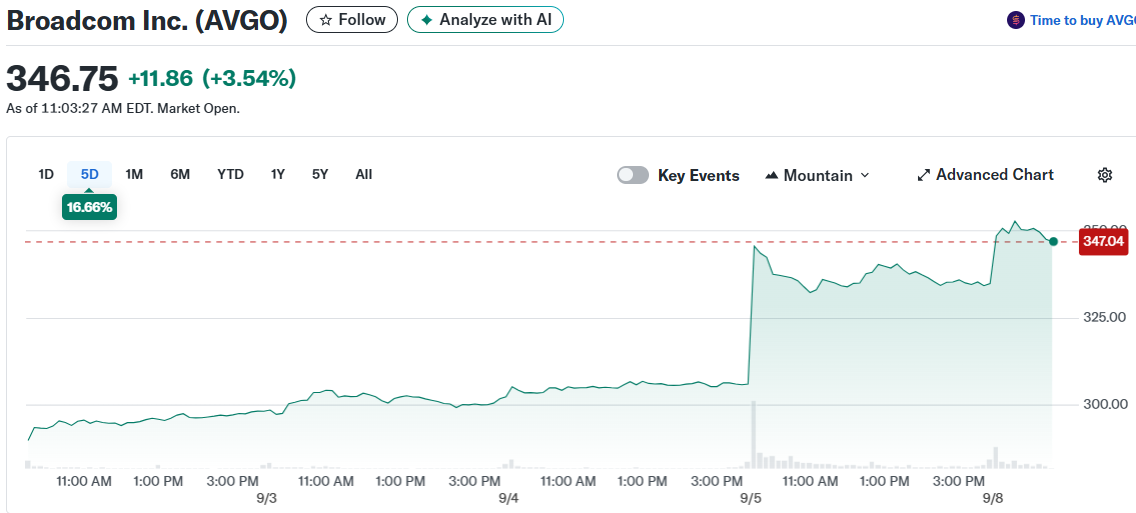

Broadcom delivered impressive third-quarter fiscal 2025 results that sent shares climbing 10% in the days following the earnings call. The semiconductor and infrastructure software company posted revenue of $15.95 billion, marking a 22% increase from the same period last year.

The company’s adjusted EBITDA reached $10.7 billion, representing a 30% year-over-year jump. These numbers reflect Broadcom’s strong positioning in the current technology landscape.

AI revenue emerged as the standout performer in the quarter. The segment generated $5.2 billion, a remarkable 63% increase compared to the previous year.

CEO Hock Tan provided optimistic guidance for the fourth quarter. He predicted AI revenue would climb to $6.2 billion in Q4.

The company’s total Q4 revenue guidance stands at $17.4 billion. This forecast includes the projected $6.2 billion from AI operations.

Broadcom’s stock performance over the past year has been impressive. Shares have gained nearly 140% during the trailing twelve months.

The recent earnings report also highlighted record-breaking free cash flow. This metric demonstrates the company’s ability to generate cash from its operations.

Investor Perspective on Growth Potential

Top investor Daniel Sparks, ranked among the top 1% of TipRanks‘ stock professionals, offered measured optimism about Broadcom’s future. He acknowledges the company is performing exceptionally well with its growing AI revenues.

However, Sparks cautions investors about expecting explosive growth similar to Nvidia. He points out that Nvidia operates on a different scale with recent quarterly revenues of $46.7 billion.

Sparks describes Broadcom as a “cash cow that should provide shareholders with good returns over the long haul.” He notes the company won’t disrupt industries like Nvidia has done.

The investor predicts “more steady compounding than ‘life-changing’ upside” going forward. This reflects the high expectations already built into the stock price after recent gains.

Broadcom’s technological contributions differ from Nvidia’s unique position in the AI revolution. The company focuses on semiconductor and infrastructure software rather than the specialized chips that power AI training.

Market Response and Analyst Coverage

Wall Street analysts remain bullish on Broadcom’s prospects. The stock currently holds a Strong Buy consensus rating from analysts.

Out of 27 analyst ratings, 25 recommend buying the stock while 2 suggest holding. No analysts currently rate the stock as a sell.

The average 12-month price target sits at $375.58. This represents potential upside of approximately 12% from current levels.

Broadcom’s market capitalization has reached $1.575 trillion. The stock’s year-to-date performance shows a gain of 45.23%.

Average trading volume for the stock stands at over 20.5 million shares. Technical indicators currently flash a buy signal for the stock.

The company secured a substantial $10 billion AI chip order. This order provides visibility into future revenue streams and supports the positive guidance.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants