Stock: Who’s Behind the $10 Billion AI Chip Mystery Order? Cramer Weighs In")

TLDR

- Broadcom secured a massive $10 billion custom AI chip order from a mystery fourth customer, widely believed to be OpenAI

- The company’s AI revenue jumped 63% to $5.2 billion in fiscal Q3, with custom chips making up 65% of total AI revenue

- Overall revenue increased 22% year-over-year to $15.96 billion, beating analyst expectations of $15.83 billion

- Broadcom forecasts Q4 AI semiconductor revenue to surge 66% to $6.2 billion as demand accelerates

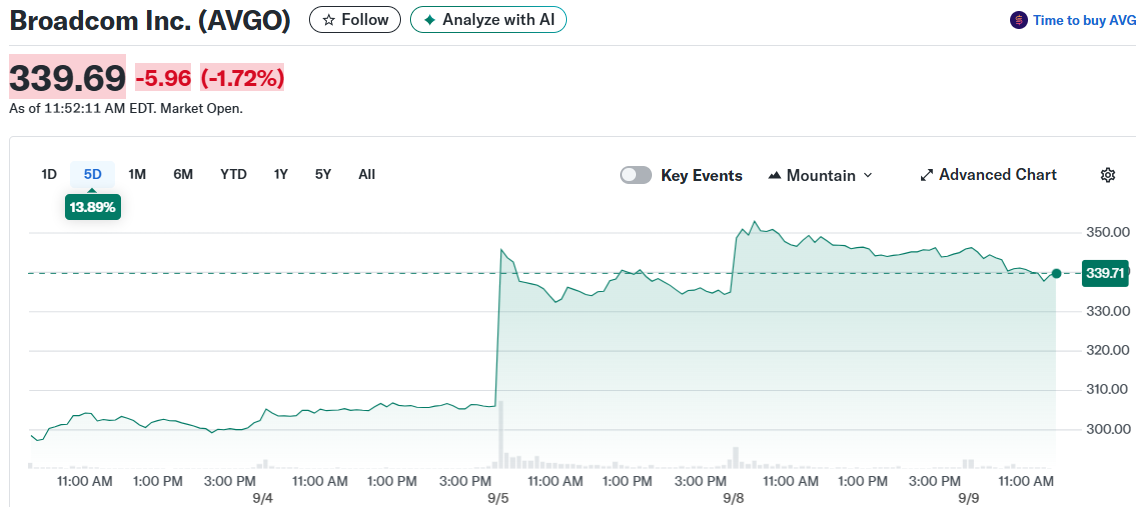

- Stock jumped 13.7% on the announcement but trades at a forward P/E of 40.7, though PEG ratio suggests undervaluation

Broadcom just dropped a bombshell that has Wall Street buzzing. The chip giant revealed it landed a mystery customer willing to spend over $10 billion on custom AI chips.

The announcement sent shares soaring 13.7% as investors tried to decode who this big spender might be. Most analysts point to OpenAI as the likely culprit.

This massive order comes on top of Broadcom’s already impressive AI business. The company worked with Alphabet to create those game-changing tensor processing units that help Google Cloud cut costs and boost performance.

That early success opened doors to more customers. Meta Platforms and ByteDance joined the party, creating what Broadcom calls a $60 billion to $90 billion opportunity by fiscal 2027.

Now this fourth customer just made that opportunity even bigger. The $10 billion order is scheduled for the second half of fiscal 2026.

Strong Quarter Across The Board

Broadcom’s fiscal Q3 numbers tell the story of a company firing on all cylinders. AI revenue rocketed 63% higher to $5.2 billion.

Custom chips drove most of that growth, accounting for 65% of total AI revenue. That’s up from 60% last quarter when AI networking led the charge.

The company’s overall revenue jumped 22% to $15.96 billion. That beat analyst expectations of $15.83 billion by a comfortable margin.

Adjusted earnings per share climbed 36% to $1.69. Wall Street was looking for $1.65, so Broadcom cleared that bar too.

Adjusted EBITDA rose 30% to $10.7 billion. The company continues to mint cash with operating cash flow hitting $7.2 billion and free cash flow at $7 billion.

Software Business Gets A Boost

While semiconductors grab the headlines, Broadcom’s software side deserves attention. Infrastructure software revenue grew 17% to $6.8 billion.

The real story is in the margins. Gross margins jumped to 93% from 90%. Operating margins climbed to 77% from 67%.

The VMware acquisition is finally paying off. That $69 billion deal closed in 2023 and full integration is now complete.

Looking Ahead

Management expects the momentum to continue. Q4 revenue should hit $17.4 billion, up 24% from last year.

Semiconductor revenue is forecast to climb 30% to $10.7 billion. Infrastructure software should rise 15% to $6.7 billion.

The real kicker is AI semiconductor revenue. Broadcom expects that to surge 66% to $6.2 billion in Q4 alone.

The OpenAI Connection

Jim Cramer weighed in on whether OpenAI is really the mystery customer. He noted OpenAI’s long partnership with NVIDIA but said there’s enough business for everyone.

Reports suggest OpenAI has been working with Broadcom since last year on custom chip development. Production appears to be moving faster than expected.

Apple is also in the mix as a newer custom chip customer, though they’re behind the other players in development.

The company ended Q3 with $10.7 billion in cash and $64.2 billion in debt from the VMware deal. That debt load hasn’t slowed down growth investments.

Broadcom trades at a forward P/E of 40.7 based on fiscal 2026 estimates, which isn’t cheap on the surface. But the PEG ratio sits around 0.5, suggesting the stock might actually be undervalued given its growth prospects.

The $10 billion order represents a massive chunk of business considering Broadcom expects only around $13 billion in total AI chip revenue this fiscal year.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants