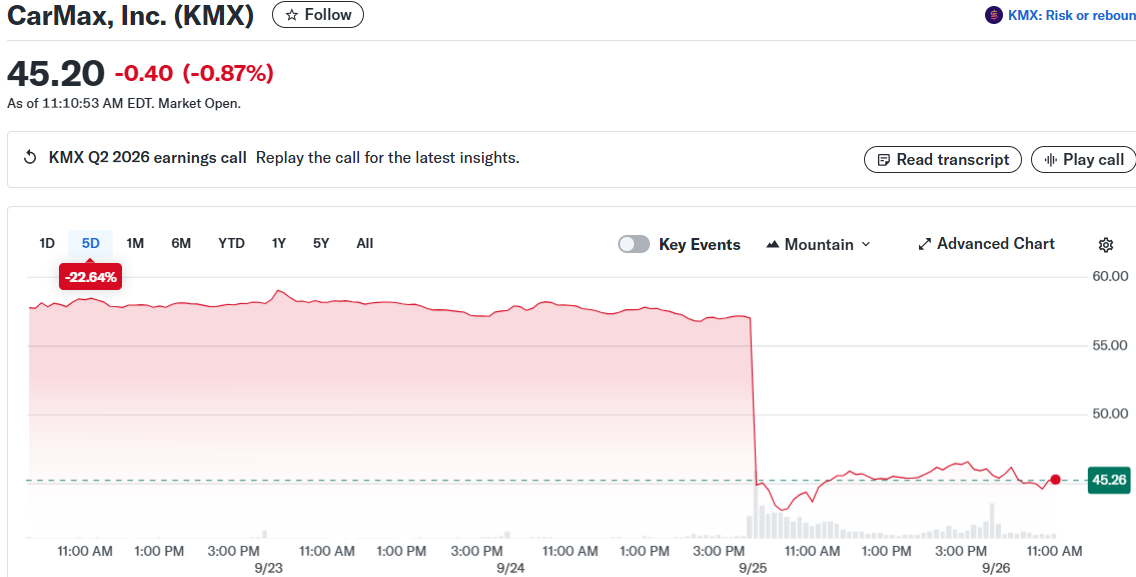

Stock: Hits All-Time Low After Earnings Miss and Analyst Downgrades")

TLDR

- CarMax stock hit all-time low of $42.75 after disappointing Q2 earnings results

- Needham lowered price target from $92 to $60, citing struggles with unit sales and loan losses

- Q2 earnings per share fell to $0.64 vs expected $1.04, revenue missed at $6.59B vs $7.04B expected

- Retail used unit sales dropped 5.4% with comparable store sales down 6.3%

- Multiple analysts downgraded the stock including Evercore ISI and Oppenheimer

CarMax shares plummeted to an all-time low of $42.75 on Thursday following disappointing second-quarter earnings results. The stock closed down 20.07% at $45.60, marking a brutal week for investors.

The used car retailer posted earnings per share of $0.64, falling well short of the expected $1.04. Revenue reached $6.59 billion, missing analyst estimates of $7.04 billion by a wide margin.

Net income declined 28.16% to $95.4 million from $132.8 million in the same period last year. Net sales and operating revenues dropped 6% year-over-year from $7.013 billion.

The company’s operational metrics painted an equally concerning picture. Retail used unit sales declined 5.4% while comparable same-store sales decreased 6.3%.

Analyst Downgrades Hit Stock Hard

The poor earnings triggered a wave of analyst downgrades and price target cuts. Needham lowered its price target to $60 from $92 while maintaining a Buy rating.

The firm cited CarMax’s continued struggles to find consistent footing. They pointed to a return to negative unit comparable sales and elevated loan losses as key headwinds to earnings power.

Needham’s revised $60 price target represents a multiple of 7.5x their fiscal year 2027 adjusted EBITDA estimate. This marks a reduction from their previous 10x multiple, reflecting lower unit growth assumptions in their model.

Evercore ISI downgraded CarMax from Outperform to In Line, citing competitive pressures from rivals like Carvana. Oppenheimer also downgraded the stock from Outperform to Perform following the weaker-than-expected results.

Truist Securities lowered its price target to $47 while maintaining a Hold rating. The firm pointed to the company’s underperformance in used unit comparable sales as a key concern.

Strategic Challenges Mount

Needham noted that CarMax’s broader omni-channel strategy remains unproven. Fears of further economic weakness are creating uncertainty regarding 2024 and 2025 vintage loans, despite solid performance to date.

The analyst firm now projects minimal market share gains for CarMax. However, they see potential for recovery in unit growth given what they consider potentially one-time issues within the quarter.

CarMax President and CEO Bill Nash acknowledged the challenges but remained optimistic about the company’s long-term strategy. “While this was a challenging quarter, we remain confident in our long-term strategy and the strength of the earnings model that we have built,” Nash said.

The company recently launched its new brand positioning campaign “Wanna Drive?” that aims to highlight its omni-channel experience. This campaign underscores the company’s ongoing commitment to empowering customers.

CarMax announced plans to continue driving selling, general, and administrative expenses efficiency. The company is targeting at least $150 million in cost savings over the next 18 months through these initiatives.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants