TLDR

- Ark Invest sold approximately 4,000 Palantir shares while maintaining over $660 million in total holdings

- The fund sold around 18,000 Shopify shares across two ETFs, reducing exposure by $3 million

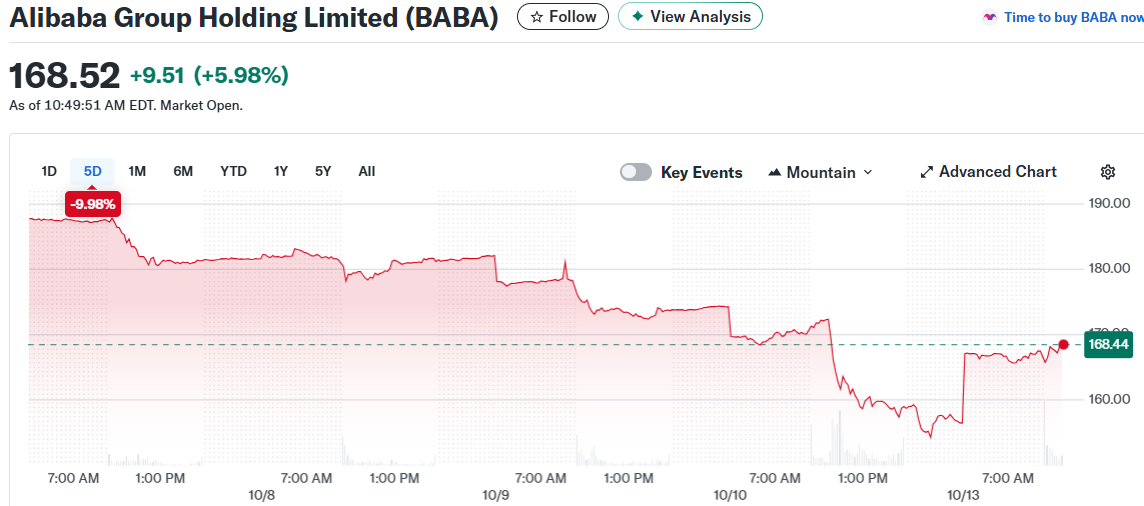

- Ark bought more than 4,000 Alibaba shares, increasing its position to approximately $44 million

- The firm purchased over 10,000 Pony.ai shares following a Buy rating from Jefferies

- Ark also bought 511,049 DraftKings shares as the stock declined 25% over the past month

Cathie Wood’s Ark Invest made several portfolio adjustments last week. The investment firm reduced its holdings in two major technology companies while increasing exposure to Chinese tech stocks and sports betting.

Ark’s flagship Innovation ETF sold about 4,000 shares of Palantir Technologies. The sale came as valuations remained high despite continued AI optimism. The fund still holds more than $660 million worth of the data analytics company.

The investment firm also trimmed its Shopify position. Ark sold roughly 18,000 shares across its Fintech and Next Generation Internet ETFs. This reduced the fund’s exposure by about $3 million. The firm maintains nearly $700 million in the e-commerce platform.

On the buy side, Ark added more than 4,000 Alibaba shares to its ARK Innovation ETF. The purchase raised the fund’s total investment to about $44 million. Ark has been building its position in the Chinese e-commerce company over recent weeks.

Autonomous Driving and Sports Betting Additions

The firm also purchased more than 10,000 shares of Pony.ai through its Autonomous Technology and Robotics ETF. The purchase followed positive analyst coverage from Jefferies, which rated the autonomous driving startup as a Buy.

Ark made another purchase in the sports betting sector. The firm bought 511,049 shares of DraftKings across its actively managed ETFs. The purchase came after DraftKings stock dropped about 25% over the past month.

DraftKings operates digital sports entertainment services including daily fantasy sports, sports betting, and online casino games. The Boston-based company has a market capitalization of $16.2 billion. The stock reached a 52-week high of $53.61 in February but has fallen 39% from that level.

The company reported second quarter fiscal 2025 revenue of $1.51 billion. This represented a 37% increase year-over-year and beat analyst expectations of $1.43 billion. Sportsbook revenue grew 45% annually to $997.87 million while iGaming revenue increased nearly 23% to $429.66 million.

Recent Financial Performance

DraftKings monthly unique payer count grew from 3.1 million to 3.3 million year-over-year. Average revenue per monthly unique payer increased from $117 to $151 over the same period. The company’s adjusted earnings per share surged 73% year-over-year to $0.38.

The stock faces pressure from macroeconomic uncertainties and regulatory challenges. Illinois imposed a 50-cent fee on high-volume sportsbooks operated by major players like DraftKings. Competition has also increased from prediction platforms including Kalshi.

DraftKings reaffirmed its fiscal 2025 revenue forecast of $6.2 billion to $6.4 billion. The company expects to reach the upper end of this range. This guidance is based on favorable sportsbook results and strong revenue contributors.

Wall Street analysts expect the company’s loss per share to narrow 75% year-over-year to $0.15 for the third quarter. For the current fiscal year, earnings per share are projected to surge 179% annually to $0.83. Fiscal 2026 projections show 98% growth to $1.64 per share.

DraftKings received a consensus Strong Buy rating from 31 analysts. Twenty-five analysts rate it Strong Buy, three suggest Moderate Buy, two recommend Hold, and one rates it Strong Sell. The consensus price target of $52.73 represents 61% potential upside from current levels.

In August, DraftKings gained a direct mobile sports betting license in Missouri. This enables the company to operate independently without affiliation to a land-based casino or professional sports team

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants