Stock: Rallies on Cantor Fitzgerald’s Bullish AI Forecast")

- Cantor Fitzgerald initiated CRWV coverage with Overweight rating and $116 price target

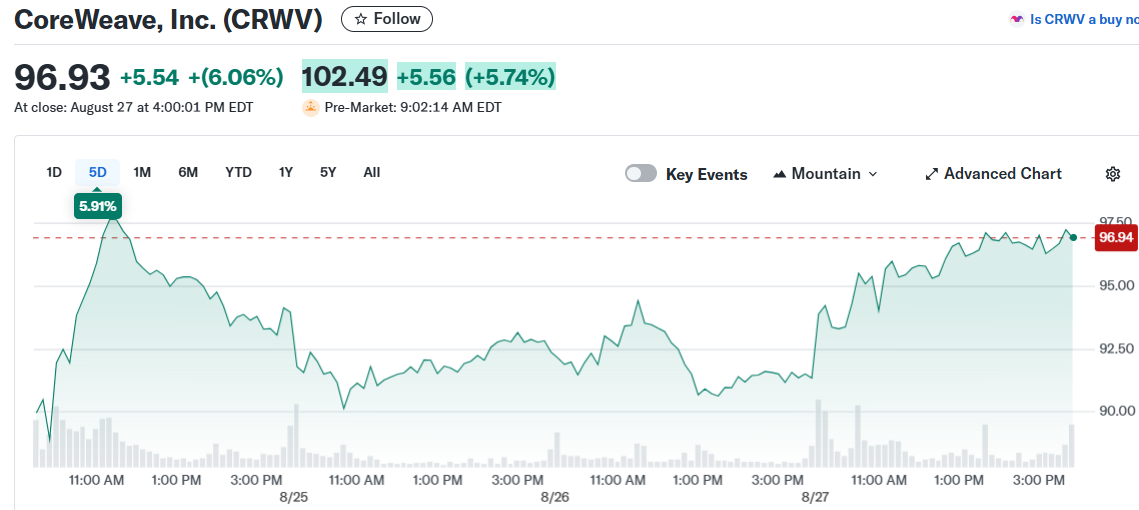

- Stock gained 6% Wednesday after analyst highlighted trillion-dollar AI market opportunity

- CoreWeave specializes in AI cloud infrastructure, generating revenue from language model training

- Nvidia owns 5.1% stake and serves as key partner supplying GPUs for operations

- Wall Street consensus shows Moderate Buy with $120.52 average target, implying 32% upside

CoreWeave stock surged 6% Wednesday following Cantor Fitzgerald’s initiation of coverage with positive ratings. The AI infrastructure company attracted investor attention after the analyst firm’s bullish assessment.

Cantor assigned an Overweight rating with a $116 price target. Analyst Thomas Blakey emphasized the company’s position in the expanding AI market.

The firm identified what it called a balanced investment opportunity. Strong AI market potential exists alongside execution challenges from rapid growth.

CoreWeave’s AI Infrastructure Business Model

CoreWeave operates as a hyperscale cloud platform focused on artificial intelligence applications. The company currently generates most revenue from large language model training services.

Analysts expect inference workloads to drive future growth. This transition could expand market opportunities as businesses increase AI adoption.

The company positions itself at the center of AI infrastructure buildout. Most revenue comes from training large language models for enterprise customers.

Strategic Nvidia Partnership Fuels Growth

Nvidia plays a crucial dual role in CoreWeave’s operations. The chip manufacturer supplies essential GPUs that power the company’s data centers.

Following the recent IPO, Nvidia holds approximately 5.1% ownership in CoreWeave. This creates a unique supplier-investor relationship benefiting both companies.

Analysts estimate Nvidia contributes meaningful revenue to CoreWeave’s business. The partnership positions both firms to capitalize on growing AI infrastructure demand.

Cantor highlighted Nvidia’s vision of trillion-dollar markets in accelerated computing and AI factories. CoreWeave aims to secure a lasting role in this infrastructure expansion.

Stock Performance and Market Outlook

Despite Wednesday’s gains, CoreWeave experienced recent volatility. The stock declined 21% over the past month following disappointing quarterly results.

The company reported larger-than-expected losses in Q2 earnings. IPO lockup expiration allowed early investors to sell shares, creating downward pressure.

However, CoreWeave remains well above its $40 IPO price with 128% gains since going public. Recent analyst upgrades from Arete Research and H.C. Wainwright support the positive outlook.

Wall Street maintains generally bullish sentiment on CRWV stock. Nine analysts rate it Buy, thirteen recommend Hold, and two suggest Sell.

The average price target of $120.52 indicates approximately 32% upside potential from current levels. Blakey’s target reflects 7x enterprise value-to-revenue multiple based on 2026 estimates.

Cantor expects CoreWeave to benefit from secular AI adoption trends. The firm sees particular strength in LLM training and inference applications driving long-term growth.

Recent quarterly results demonstrated both opportunities and challenges facing AI infrastructure companies as they balance growth investments with profitability pressures.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants