Stock: Earnings Expectations Point to Potential 65% Upside")

TLDR

- Costco reports Q4 2025 earnings on September 25 with analysts expecting $5.81 EPS and $86.11 billion revenue

- Stock historically rises 65% of the time after earnings with median gain of 1.9%

- UBS and Raymond James maintain Buy ratings with price targets of $1,205 and $1,070 respectively

- Options traders expect 3.7% stock movement in either direction following earnings

- Wall Street consensus is Moderate Buy with average price target of $1,085.40

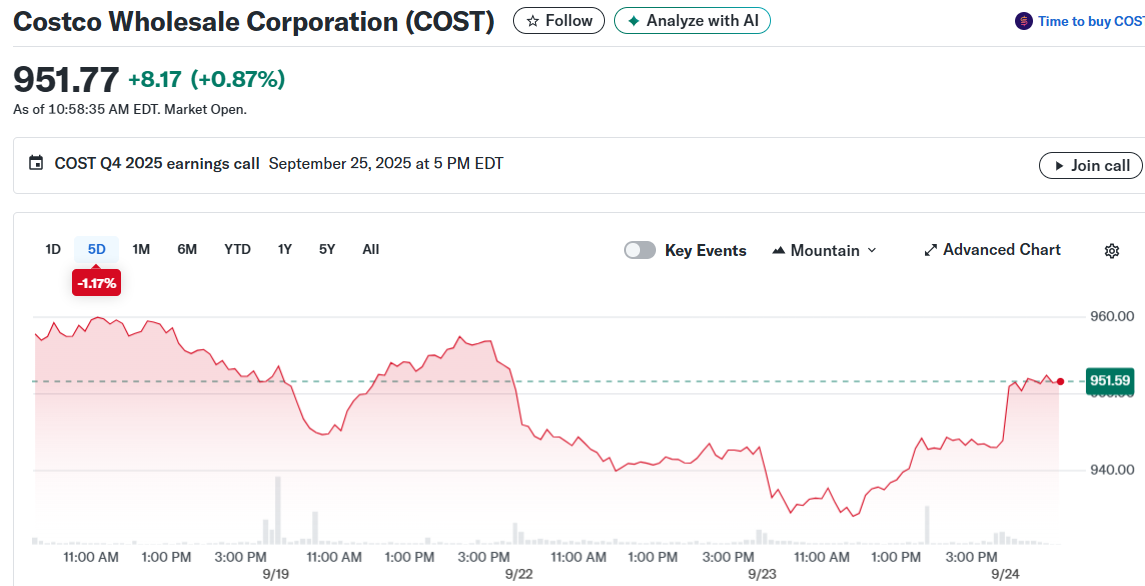

Costco Wholesale prepares to release its fiscal fourth quarter 2025 results on Thursday, September 25. The membership warehouse retailer faces analyst expectations of $5.81 earnings per share on revenue of $86.11 billion.

These projections represent a 10% increase in EPS and 8% revenue growth compared to last year’s $5.29 per share on $79.70 billion. The company’s stock has gained 3% year-to-date as investors await the quarterly report.

Historical data suggests favorable odds for post-earnings performance. Over the past five years, Costco stock has risen after earnings announcements 65% of the time. The median one-day gain during positive sessions reaches 1.9%.

Maximum historical movement peaks at 7% in a single day following earnings. This percentage drops slightly to 64% when examining only the past three years of data.

The warehouse operator maintains a market capitalization of $418 billion. Over the trailing twelve months, revenue reached $269 billion with operating profits of $10 billion and net income of $7.8 billion.

Analyst Sentiment Remains Positive

UBS analyst Michael Lasser maintains a Buy rating with a $1,205 price target. Lasser addresses market concerns about softer comparable sales growth in May and June that raised questions about the stock’s elevated multiple.

The analyst believes these concerns stem from viewing isolated results. Costco’s comparable sales and traffic reaccelerated in July and August, which should ease investor worries.

Lasser expects the company to maintain momentum through best-in-class merchandising and upcoming catalysts. He believes Costco will uphold its premium valuation based on these factors.

Raymond James analyst Bobby Griffin also rates the stock a Buy with a $1,070 price target. Griffin notes the valuation multiple sits near its one-year trough while business fundamentals remain strong.

The analyst points to consistent execution, defensive category mix, and strong member loyalty as justification for premium pricing. Griffin expects 25 net new annual store openings and broad-based market share gains.

Options Market Signals Modest Volatility

TipRanks’ Options tool shows traders expect approximately 3.7% movement in either direction following the earnings announcement. This expectation comes from at-the-money straddle calculations for options expiring after the earnings release.

TipRanks‘ AI Analyst assigns an Outperform rating with a $1,071 price target. This represents about 13.5% upside potential from current levels.

The AI analysis highlights strong financial performance and favorable earnings call insights. However, it notes concerns over high valuation and mixed technical indicators as potential headwinds.

Costco exceeded expectations in Q3 FY2025 with EPS of $4.28 and revenue of $63.2 billion. Comparable sales grew 8% while e-commerce jumped 16% year-over-year.

The company’s size, bulk pricing model, and low-cost approach position it well for potential tariff-related challenges. Membership fee increases are expected to boost results starting in Q4 2025.

Wall Street maintains a Moderate Buy consensus rating based on 12 Buy recommendations and nine Hold ratings. The average price target of $1,085.40 suggests 15% upside potential from current trading levels.

Costco’s Q4 FY25 comparable sales data and traffic trends in July-August showed reacceleration after the May-June slowdown that initially concerned some market participants.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants