TLDR

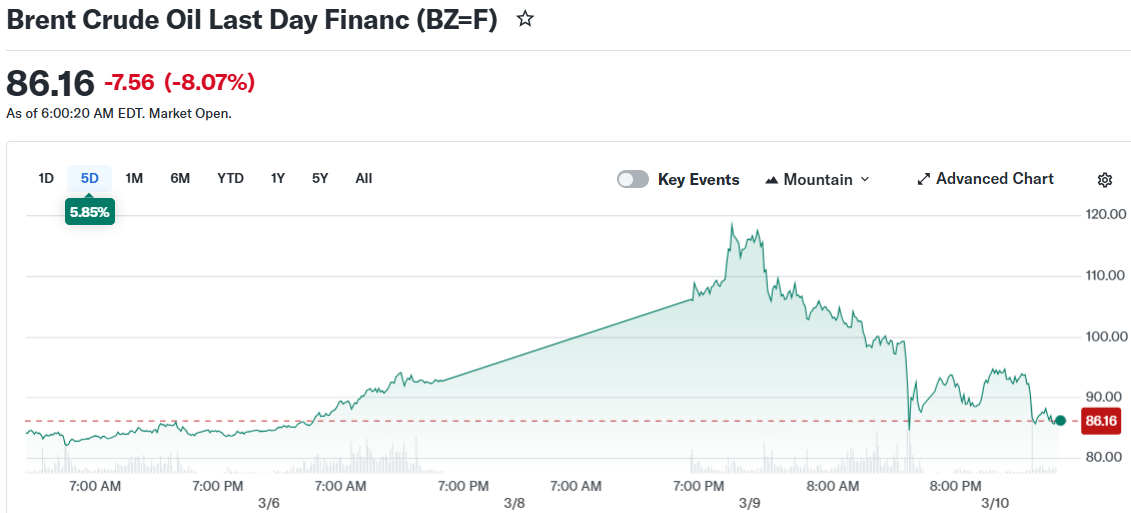

- Brent crude tumbled 6–7% to approximately $92 on Tuesday following Monday’s peak above $119

- President Trump described the Iran conflict as “very complete” and progressing faster than his projected 4–5 week timeframe

- Iran’s Revolutionary Guard dismissed Trump’s assessment and warned of blocking regional oil shipments

- G7 countries announced preparedness to tap strategic petroleum reserves while withholding immediate action

- Goldman Sachs maintained its $66/barrel Brent projection for Q4 2026, acknowledging ongoing uncertainty

Energy markets experienced dramatic volatility this week as contradictory messaging from Washington and Tehran created uncertainty. Brent crude plummeted approximately 7% on Tuesday, settling near $92 per barrel—a stark reversal from Monday’s climb above $100, a threshold not breached since mid-2022.

Monday’s spike resulted from supply disruption concerns. Major producers including Saudi Arabia implemented output reductions as U.S.-Israeli military operations against Iran intensified, driving Brent to $119.50 and WTI to $119.48. Dow Jones Market Data confirmed this represented the highest single-day intraday volatility ever recorded.

The dramatic turnaround followed Trump’s Monday CBS News interview, where he characterized the conflict as “very complete” and stated operations were progressing “very far ahead” of his original four-to-five week projection. This single statement calmed jittery markets and sparked immediate oil selling.

Russian leader Vladimir Putin’s Monday conversation with Trump, during which settlement proposals were discussed, reinforced the de-escalation narrative and accelerated the price retreat.

However, not all parties accepted this conflict resolution narrative.

Iran Pushes Back

Iran’s Islamic Revolutionary Guard Corps declared Tuesday that they alone—not Washington—would “determine the end of the war.” The military organization additionally threatened complete blockades of regional oil exports should American and Israeli attacks persist.

Iran’s top diplomat Abbas Araghchi independently dismissed any possibility of U.S. negotiations during a PBS News interview, the Wall Street Journal reported.

Trump fired back via Truth Social, cautioning Iran that any attempt to obstruct the Strait of Hormuz would provoke American retaliation “twenty times harder than they have been hit thus far.”

Market observers suggested traders may be overreacting in both directions. “While there was an overreaction to the upside yesterday, we think there is an overreaction to the downside today,” commented Suvro Sarkar, DBS Bank’s energy sector team lead.

Sarkar highlighted that Murban and Dubai oil grades continued trading above $100 per barrel, indicating underlying physical market conditions remained relatively unchanged.

What Governments Are Doing

G7 finance officials convened Monday to evaluate emergency petroleum reserve releases. While no immediate action was authorized, their joint statement confirmed they “stand ready to take necessary measures,” including potential stockpile deployments.

Reports indicate Trump is weighing Russian oil sanctions relief as part of broader price stabilization efforts. Multiple sources confirmed this option remains under active consideration.

Phillip Nova analyst Priyanka Sachdeva attributed the selloff to combined factors—potential Russian sanctions modifications, G7 reserve release readiness, and Trump’s optimistic conflict assessment—providing sufficient rationale for traders to exit panic positions.

Goldman Sachs announced no modifications to its oil forecasts. The investment bank continues projecting Brent at $66 per barrel and WTI at $62 per barrel for fourth quarter 2026, acknowledging the situation’s fluid dynamics.

Iran’s IRGC Tuesday statement represents the latest hard evidence that hostilities remain far from resolved.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants