TLDR

- Dell Technologies stock fell 7% in premarket trading despite beating Q2 earnings expectations with record $29.8 billion revenue

- Company raised AI server shipment guidance to $20 billion from $15 billion for full fiscal year

- Q3 earnings projection of $2.45 per share missed analyst expectations of $2.49

- Non-GAAP gross margins declined to 18.7% from 22.4% year-over-year due to AI server production scaling

- AI server backlog decreased to $11.7 billion from $14.4 billion in previous quarter

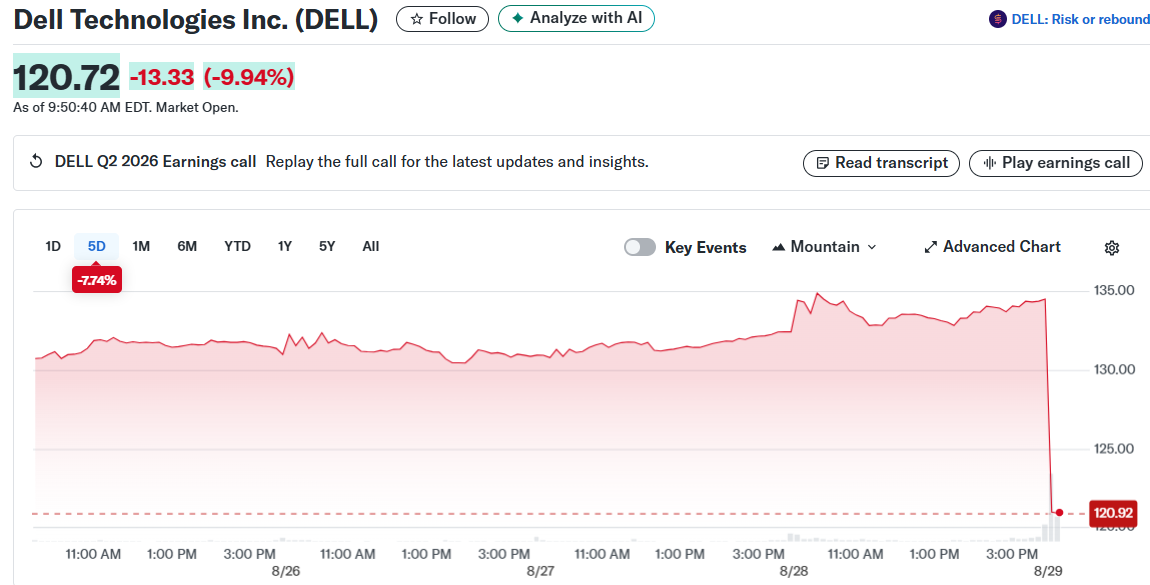

Dell Technologies delivered impressive second-quarter results that should have investors celebrating. Instead, the stock tumbled 7% in premarket trading Friday as Wall Street focused on margin pressure and soft guidance.

The company posted record quarterly revenue of $29.8 billion, representing 19% year-over-year growth. Adjusted earnings per share reached $2.32, beating analyst expectations while cash flow from operations nearly doubled to $2.5 billion.

Dell’s AI server business stole the spotlight with $8.2 billion in quarterly shipments. The company has now shipped $10 billion in AI solutions during the first half of fiscal 2026, already exceeding all of fiscal 2025.

AI Business Drives Growth Despite Market Skepticism

Management raised their AI server shipment guidance to $20 billion for the full year, up from the previous $15 billion target. Chief Operating Officer Jeff Clarke called demand for AI solutions “exceptional” during the earnings call.

Dell ended Q2 with an $11.7 billion backlog of AI server orders. The company was first to deliver Nvidia’s GB300 NVL72 systems to CoreWeave in July, positioning itself as a key player in AI infrastructure.

The servers and networking division grew 69% during the quarter. This segment has become Dell’s primary growth engine as companies rush to build artificial intelligence capabilities.

However, investors zeroed in on concerning signals. Dell’s third-quarter earnings guidance came in at $2.45 per share, below the $2.49 analysts expected.

Margin Pressure Creates Investor Concerns

Non-GAAP gross margins compressed to 18.7% in Q2 from 22.4% a year earlier. The decline reflects the economics of AI server production, where margins run thinner than traditional enterprise products.

Dell’s PC segment also disappointed, with sales falling 3% below consensus forecasts. Citi analysts noted the company “likely lost share in PCs” during the quarter.

The AI server backlog dropped from $14.4 billion in Q1 to $11.7 billion in Q2. While still substantial, the decline sparked questions about whether order momentum might be plateauing.

Traditional server business is expected to grow in the second half but below earlier expectations. This tempers some enthusiasm around the AI-driven gains.

Dell stock entered Friday up 16% for the year before the premarket decline. The company continues ramping production to meet AI infrastructure demand while managing margin pressure and competitive challenges.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants