Stock: Strong Q2 Earnings Beat Can’t Lift Year-Long Slump")

TLDR

- DocuSign beat Q2 earnings at $0.92 per share versus $0.84 expected, marking fourth straight quarter of beats

- Revenue reached $800.6 million, growing 9% year-over-year and topping estimates by 2.78%

- Evercore ISI raised price target to $92 from $90 following strong quarterly performance

- Stock remains down 15.6% year-to-date despite consistent earnings outperformance

- Full-year revenue guidance increased to $3.19-3.20 billion from previous $3.16 billion estimate

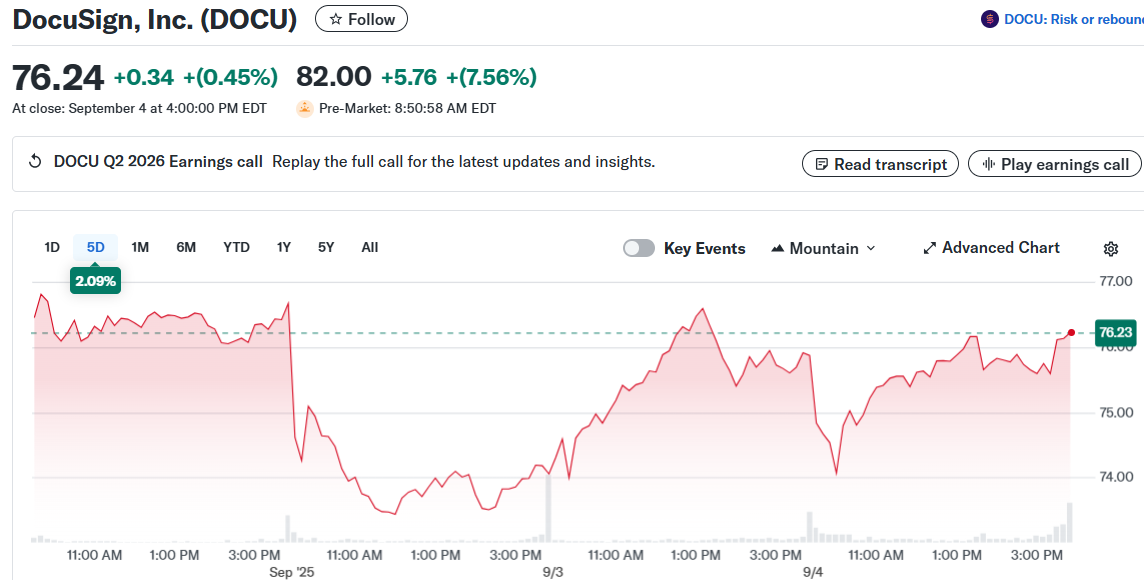

DocuSign continues its streak of beating Wall Street expectations, but the stock can’t seem to catch a break in 2025. The electronic signature leader posted Q2 earnings of $0.92 per share, crushing analyst estimates of $0.84.

This marks the fourth consecutive quarter where DocuSign has topped earnings forecasts. The company delivered a 9.52% earnings surprise, building on last quarter’s 11.11% beat.

Revenue came in strong at $800.6 million for the July quarter. This beat consensus estimates and represented solid 9% growth compared to $736 million in the prior year period.

International Markets Drive Growth

DocuSign’s international business emerged as a key growth driver in Q2. International revenue jumped 13% year-over-year and now accounts for 29% of total company revenue.

The Asia-Pacific region led international growth, becoming DocuSign’s fastest-growing market. This geographic diversification helps reduce the company’s dependence on its core U.S. market.

Net retention improved 100 basis points sequentially to 102%, driven primarily by stronger performance in the core eSignature business. The company also showed progress in Contract Lifecycle Management and Identity Access Management services.

Guidance Raised Despite Market Headwinds

Based on Q2 performance, DocuSign raised its full-year revenue guidance to $3.19-3.20 billion. This represents approximately 7% growth compared to the previous estimate of $3.16 billion.

The guidance increase reflects management’s growing confidence in business momentum. However, operating margins declined 240 basis points to 29.8% due to higher compensation costs and cloud migration expenses.

Evercore ISI responded to the strong results by raising its price target to $92 from $90. The firm maintained its “In Line” rating while acknowledging improved execution in DocuSign’s go-to-market strategy.

Despite four straight earnings beats, DocuSign stock has struggled in 2025. Shares are down 15.6% year-to-date, significantly underperforming the S&P 500’s 9.6% gain over the same period.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants