Stock: Debut Earnings Miss Sends Shares Tumbling 14%")

TLDR

- Figma shares fell 14% after-hours following first public company earnings report

- Q2 revenue of $221.75M missed company guidance of $247-250M range

- Stock down 41% from IPO peak as high valuation faces scrutiny

- Employee share lock-up expires this week, adding supply pressure

- CEO comments about major AI investments concerned investors

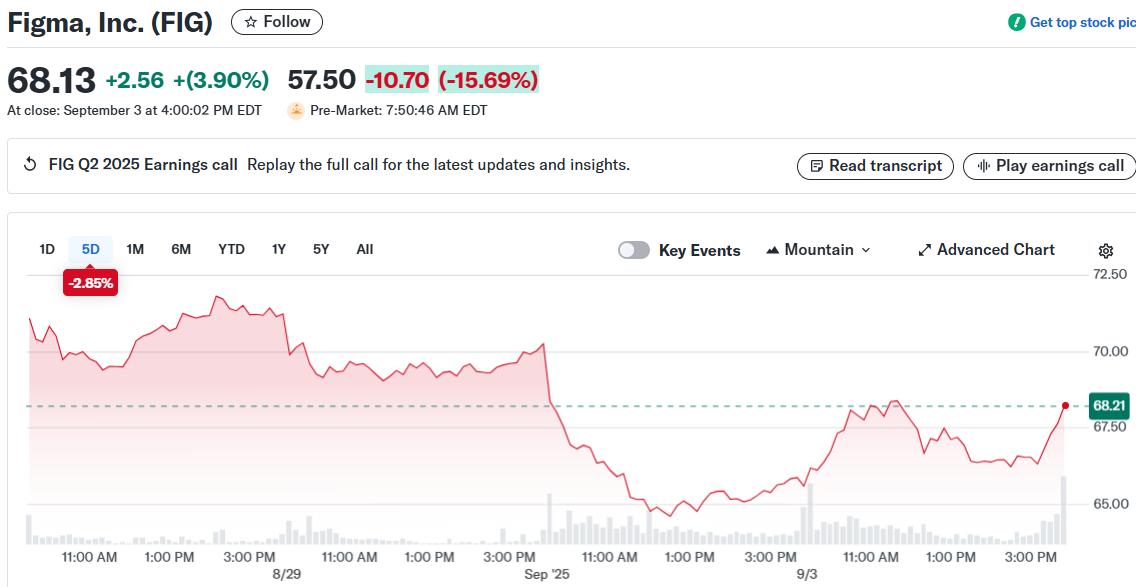

Figma stock dropped sharply in extended trading Wednesday after the design software company’s first earnings as a public entity disappointed investors.

The company reported second-quarter revenue of $221.75 million. This represented strong 61% year-over-year growth from $137.64 million. However, it fell short of Figma’s own guidance range of $247-250 million.

The miss stung particularly hard given expectations around the company’s July IPO. Figma went public at $33 per share but opened trading at $85. Shares peaked at $142.92 the following day.

Since then, the stock has retreated. Figma shares have lost 41% from their peak through Wednesday’s close. The after-hours decline threatens to extend those losses.

Valuation Concerns Mount

Figma currently trades at 299.2 times forward earnings. This multiple dwarfs legacy competitor Adobe at 15.3 times and the broader S&P 500 at 23.7 times.

The rich valuation leaves little room for error. When companies trade at such high multiples, even small disappointments can trigger large stock moves.

CEO Dylan Field acknowledged the company’s ambitious plans during the earnings call. “We do plan to take big swings if and when we see opportunities to invest both organically and inorganically,” Field told analysts.

These comments about major AI investments may have unsettled some investors. Wall Street often prefers measured spending over aggressive investment cycles, especially for newly public companies.

On the positive side, Figma achieved breakeven results on a GAAP basis. This marked a turnaround from the $4.39 loss per share reported a year earlier. Non-GAAP net income grew to $19.78 million from $14.28 million.

Supply Pressure Looms

Timing adds another challenge for Figma shares. Employee lock-up periods expire later this week. This could flood the market with additional supply just as sentiment turns negative.

Currently, only 41% of Figma’s shares trade as free float. The limited supply has contributed to the stock’s extreme volatility since its debut.

Five major venture capital firms remain locked up through mid-2026. But the employee unlock represents the first major test of investor demand.

For the current quarter, Figma projects revenue between $263-265 million. Full-year guidance calls for $1.021-1.025 billion in revenue. These targets roughly align with analyst expectations.

Retail traders showed mixed reactions to the results. Some viewed the post-earnings drop as a buying opportunity. Others questioned whether the company can justify its premium valuation.

Short interest in Figma has climbed to nearly 1% of float, the highest level since its public debut. This suggests some investors are betting against the stock’s near-term performance.

The earnings report highlights challenges facing high-growth companies in public markets. Quarterly reporting cycles create pressure to deliver consistent results. For Figma, maintaining its growth trajectory while managing investor expectations will be crucial as more share supply enters the market.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants