Stock: Drops as Wall Street Stays Cautious Ahead of Earnings")

TLDR

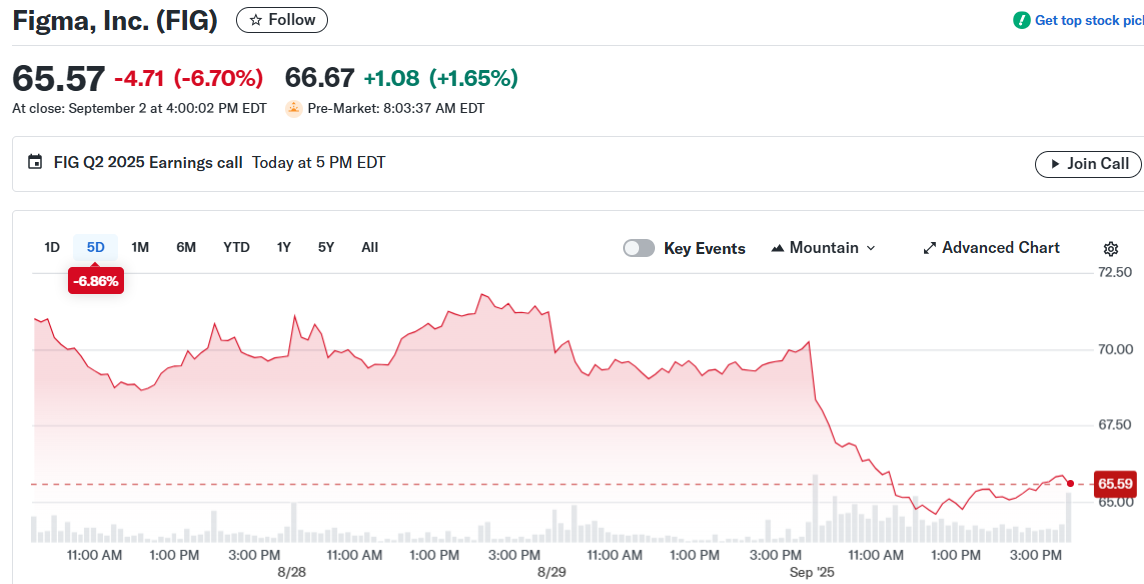

- Figma (FIG) stock dropped 6.7% to $65.57 ahead of its first public earnings report on September 3

- The company expects Q2 earnings of 9 cents per share on $250 million revenue, up 40% year-over-year

- Only 4 of 11 Wall Street analysts rate Figma as a Buy, with 7 giving Hold ratings due to high valuation concerns

- Figma trades at over 200 times earnings estimates, compared to rival Adobe’s 17 times earnings multiple

- Key metrics to watch include 132% Net Dollar Retention rate and 47% growth in customers paying over $100K annually

Figma stock tumbled 6.7% to $65.57 on Tuesday as investors braced for the design software company’s first quarterly earnings report as a public entity. Trading volume hit $520 million, ranking 197th in market activity.

The company will report second-quarter results after market close on Wednesday. Wall Street expects earnings of 9 cents per share on revenue of $250 million, marking a 40% jump from the same period last year.

Figma went public on July 31 at $33 per share and rocketed 250% on its debut day. The stock peaked near $143 on its second trading day before cooling off to current levels.

The company now carries a market value of nearly $35 billion. That puts shares at more than 200 times this year’s earnings estimates.

For comparison, rival Adobe trades at just 17 times forward earnings. Adobe had agreed to buy Figma for $20 billion in 2022, but regulators killed the deal in December 2023 over competition concerns.

Wall Street Remains Cautious

Only four of eleven analysts covering Figma rate the stock a Buy. Seven analysts give it Hold ratings, reflecting concerns about the rich valuation.

BofA Securities analyst Brad Sills called Figma’s valuation a “big premium to the large-cap software group” in an August 25 report. He rates the stock Neutral and thinks “near-term upside is largely priced in.”

Sills also worries about competition that “could take share and cause disruption.” He sees artificial intelligence potentially leading to more automation, which could hurt Figma’s revenue growth.

RBC Capital Markets analyst Rishi Jaluria takes a different view on AI risks. He thinks AI could actually help Figma through tools like Figma Make, an AI-powered prototyping feature the company is developing.

But Jaluria still rates Figma as Sector Perform, equivalent to a Hold. He wrote that shares look “fully valued” and advised investors to “wait for a better entry.”

Key Metrics in Focus

Investors will watch Figma’s Net Dollar Retention rate closely. This metric stood at 132% as of March 2025, showing strong customer loyalty and spending growth.

Figma raised prices in March 2025, which should boost both revenue and retention rates. However, analysts expect this effect to normalize by early 2026.

Another important number is customers paying over $100,000 annually. This group grew 47% year-over-year to 1,031 customers, showing Figma’s ability to land big enterprise deals.

Figma’s gross margin sits at 91%, highlighting the profitable nature of its software business. But the company’s AI investments may pressure margins going forward.

Analysts project gross margins could drop to 87% in 2025 and 83% in 2026 as Figma spends on new technology.

The forward price-to-earnings ratio of 240 times remains sky-high. This puts pressure on management to show strong growth to justify the valuation.

Figma has joined other recent IPOs that saw massive first-day pops but later gave back gains. Circle Internet Group went public at $31 in June and now trades around $132, well below its peak near $300.

Medical imaging company Heartflow and crypto platform Bullish have shown similar patterns of early euphoria followed by more measured trading.

The earnings report will test whether Figma can live up to investor expectations. The company lost money in the second quarter of 2024, making the path to profitability a key storyline.

Figma’s business model centers on design collaboration tools used by companies to create digital products. The platform has gained popularity as more businesses focus on user experience and digital transformation.

The company faces competition from established players like Adobe and newer entrants building AI-powered design tools. How Figma addresses these competitive threats will likely shape investor sentiment going forward.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants