Stock: Earnings Beat Fails to Stop Share Decline. Here’s Why")

TLDR

- General Mills reported 86 cents per share, beating analyst estimates of 81 cents

- Revenue dropped 6.8% to $4.52 billion despite exceeding forecasts

- North America retail sales fell 13% while international sales grew 6%

- Company maintained fiscal 2026 guidance with flat to 1% organic sales growth

- Stock declined 1.2% in premarket trading following results

General Mills delivered mixed quarterly results that highlighted the ongoing challenges facing the packaged food industry. The company behind Cheerios and Betty Crocker beat earnings expectations but couldn’t escape declining sales trends.

The food manufacturer posted adjusted earnings of 86 cents per share, surpassing Wall Street’s forecast of 81 cents. First-quarter revenue reached $4.52 billion, slightly above estimates but down 6.8% from the prior year period.

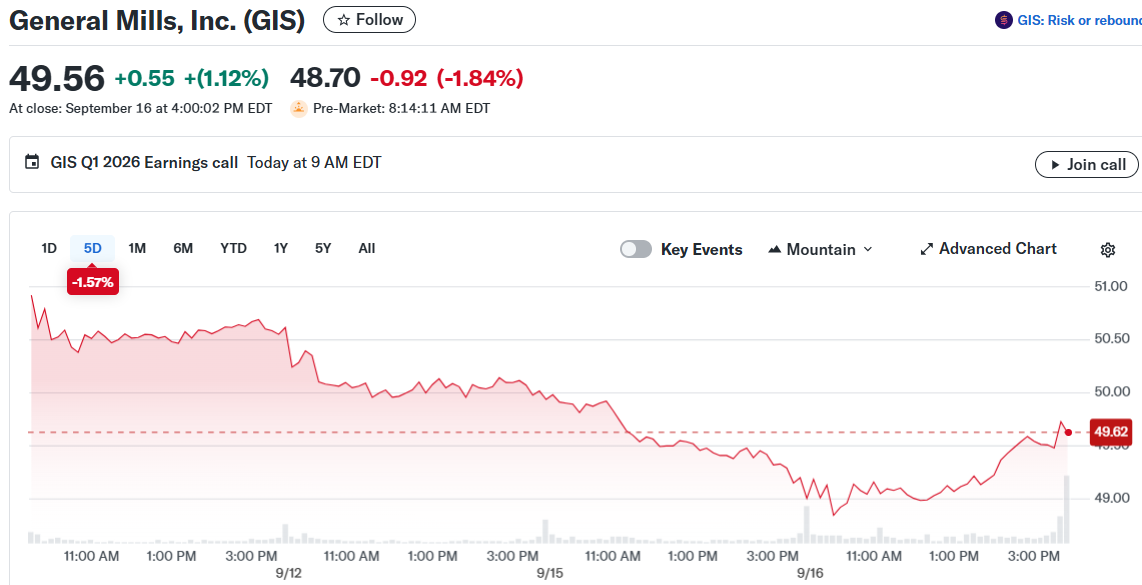

Despite the earnings beat, investors weren’t impressed. General Mills stock dropped 1.2% to $48.99 in premarket trading, reflecting concerns about the company’s sales trajectory.

Revenue Decline Spans Multiple Categories

The sales weakness wasn’t confined to a single business segment. North America retail sales plummeted 13% during the quarter, while the region’s foodservice division saw a 4% decline to $517 million.

International operations provided some relief, with sales climbing 6% to $760 million. This growth helped cushion the domestic downturn but couldn’t prevent the overall revenue decline.

Consumer behavior shifts continue pressuring packaged food companies. Shoppers increasingly choose cheaper private-label alternatives as inflation concerns persist. The rising popularity of weight-management medications has also reduced overall food consumption.

General Mills has experienced declining net sales in five of the past six quarters, excluding November. This pattern underscores the structural challenges facing traditional food manufacturers.

Management Remains Optimistic About Turnaround

CEO Jeff Harmening expressed confidence in the company’s recovery strategy. He highlighted investments in product innovation, consumer value, and marketing initiatives.

“Our primary goal in fiscal 2026 is to restore organic sales growth,” Harmening stated. The executive emphasized new product launches including Cheerios Protein and high-protein Pitmaster Soups.

General Mills maintained its full-year guidance despite ongoing headwinds. The company expects organic net sales between down 1% and up 1% for fiscal 2026. Adjusted earnings are projected to fall 10% to 15% in constant currency.

Management acknowledged that category growth would likely underperform long-term targets due to challenging consumer conditions.

Cost Reduction and Growth Initiatives

The pet food division showed resilience with 6% growth, though below analyst expectations of 8.5%. Blue Buffalo is expanding into fresh pet food to compete with brands like Freshpet.

General Mills plans additional cost-saving measures targeting $100 million in fiscal 2026. The company previously closed its innovation unit and paused venture capital investments as part of efficiency efforts.

Increased advertising spending and in-store promotional activities support the turnaround strategy. These investments aim to rebuild brand loyalty and drive volume growth.

The stock has declined 22% year-to-date, underperforming the S&P 500 Consumer Staples Index’s 1.8% gain. General Mills trades at 13 times forward earnings, below many packaged food peers.

The company reported international sales growth of 6% to $760 million while domestic operations continued facing pressure from changing consumer preferences and competitive dynamics.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants