Stock: Citi Slaps Sell Rating Despite Nvidia Partnership")

TLDR

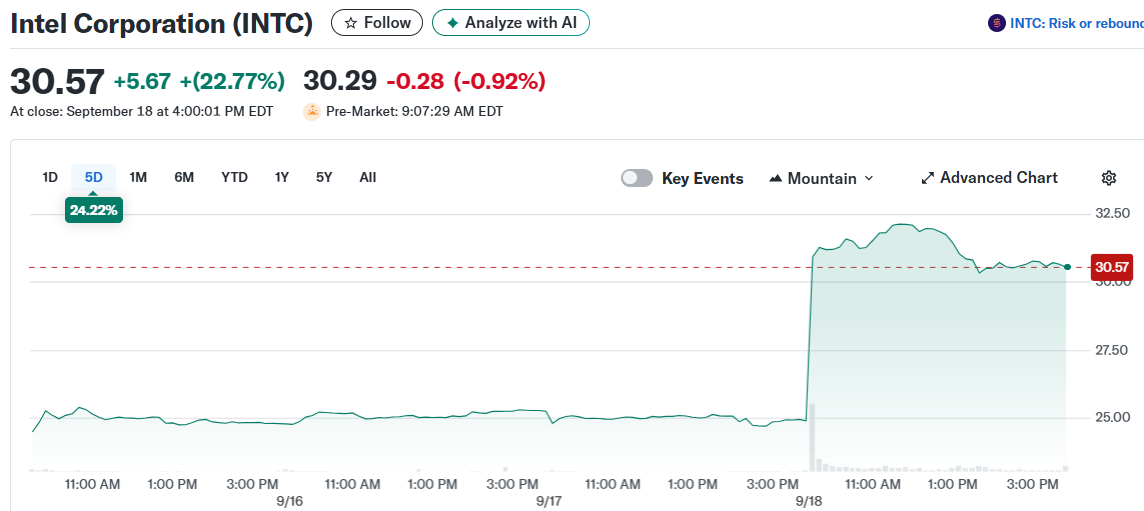

- Citi downgraded Intel stock to Sell from Neutral despite raising price target to $29

- Intel surged 23% Thursday on $5 billion Nvidia investment announcement

- Analyst believes Intel’s foundry business cannot compete with Taiwan Semiconductor

- Stock has rallied 50% since August, pricing in unlikely foundry success

- Wall Street consensus remains Hold with 22% downside implied by price targets

Intel stock tumbled in premarket trading Friday after Citi analyst Christopher Danely issued a surprise downgrade to Sell from Neutral. The move came just hours after Intel shares posted their biggest single-day gain in months following the Nvidia partnership announcement.

Danely raised his price target to $29 from $24 but warned that Intel’s recent 50% rally has pushed the stock beyond reasonable valuations. The analyst believes current prices assume a foundry turnaround that has minimal chances of success.

Thursday’s bombshell announcement revealed Nvidia would invest $5 billion for a 4% Intel stake. The partnership includes Intel building custom CPUs for Nvidia’s AI platforms and developing x86 processors with integrated Nvidia graphics for PC markets.

Intel stock has surged approximately 50% since early August on speculation that the Nvidia deal signals broader foundry opportunities. However, Citi disagrees with this optimistic market reaction.

Why Citi Sees Limited Upside

Danely expressed skepticism about Intel’s ability to compete against established foundry leaders like Taiwan Semiconductor Manufacturing. He noted Intel’s foundry operations remain “years behind TSMC” technologically.

The analyst sees minimal improvement from the Nvidia partnership itself. Enhanced graphics won’t make Intel CPUs superior to AMD processors, since the CPU remains the primary performance driver for most applications.

Citi estimates the Nvidia AI platform opportunity represents only $1-$2 billion in potential revenue for Intel. This accounts for roughly 3% of projected 2026 sales, making it a relatively small business segment.

Market expectations for additional foundry deals appear overly optimistic given Intel’s technological disadvantages, according to the Citi analysis.

Valuation Concerns Drive Downgrade

Danely’s primary concern centers on Intel’s current valuation rather than operational improvements. The recent rally has pushed shares to levels that assume a complete business transformation has already occurred.

The analyst argues Intel’s foundry business faces steep odds of achieving the success current stock prices reflect. This creates an unfavorable risk-reward scenario for investors at present levels.

Current market expectations appear to discount the substantial challenges Intel faces catching up to foundry leaders. The company must overcome years of technological gaps while competing against well-established rivals.

Wall Street maintains a Hold consensus on Intel stock based on one Buy, 26 Hold, and three Sell ratings over the past three months. The average price target of $23.61 implies 22% downside risk from current levels.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants