Key Takeaways

- Bitcoin climbed 2.5% to reach $67,884 on Tuesday while remaining trapped below the $70,000 threshold amid heightened U.S.-Iran geopolitical tensions

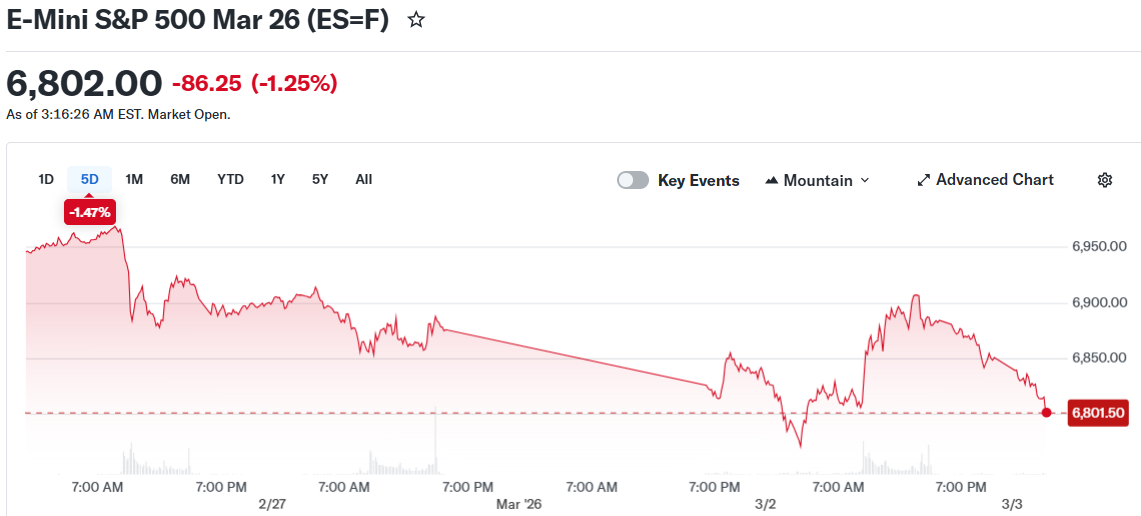

- Stock market futures declined following Monday’s late-session recovery from significant intraday selloffs

- Defense contractors and energy companies outperformed; notable gains in Lockheed Martin, Palantir, and Nvidia climbing approximately 3%

- Crude oil markets rallied sharply on concerns that Strait of Hormuz disruptions could trigger supply shortages and inflationary pressures

- Market participants are closely monitoring Friday’s employment data and upcoming Federal Reserve commentary for monetary policy signals

Bitcoin registered modest gains on Tuesday, advancing 2.5% to settle at $67,884. This uptick occurred alongside Wall Street’s efforts to stage a recovery, although caution continued to dominate both asset classes.

The digital currency landscape has remained largely stagnant throughout February. Bitcoin has been confined to a trading corridor between $60,000 and $70,000 for several weeks, posting a 22% decline year-to-date in 2026.

During Monday’s session, Bitcoin reached an intraday peak of $69,213 before retreating. The flagship cryptocurrency has struggled to maintain levels above $70,000 since the closing days of January.

Market sentiment across all asset classes has been influenced by intensifying Middle Eastern hostilities. Joint military operations conducted by the U.S. and Israel resulted in the death of Iran’s Supreme Leader, Ayatollah Ali Khamenei, during the conflict’s opening phase.

President Trump indicated the military campaign might extend four to five weeks, while acknowledging the possibility of a prolonged engagement. As of Tuesday, leadership in all three nations demonstrated minimal willingness to de-escalate.

Energy Markets Surge on Supply Chain Disruption Concerns

Oil prices experienced substantial increases following reports of Strait of Hormuz closures. Threats directed at maritime vessels attempting passage through this critical waterway intensified anxieties regarding worldwide supply chain interruptions.

Energy sector equities and defense industry stocks commanded Monday’s market gains. Lockheed Martin and Palantir registered notable advances, with Nvidia posting approximately 3% growth.

Overnight trading showed weakness in U.S. equity futures. S&P 500 futures contracted 0.2%, Nasdaq 100 futures declined 0.3%, while Dow futures similarly retreated approximately 0.2%.

Notwithstanding overnight futures weakness, major equity benchmarks concluded Monday’s session in positive territory. The S&P 500 finished marginally higher, with the Nasdaq Composite also posting gains.

Market participants appeared to capitalize on intraday price weakness throughout Monday’s trading. The Dow Jones Industrial Average recouped the majority of its early session losses by market close.

Digital Asset Performance and Upcoming Economic Indicators

The wider cryptocurrency market posted Tuesday gains while failing to surpass Monday’s session highs. Ethereum appreciated 2.6% to reach $1,993. XRP increased 0.9%, Solana advanced 2.9%, and BNB strengthened 2.5%.

Dogecoin decreased 0.6%, whereas $TRUMP climbed 1.5%. Cardano experienced a 1.1% decline.

Strategy’s recent corporate Bitcoin acquisitions failed to meaningfully impact prevailing market sentiment. Bitcoin remains more than 40% below its October 2025 all-time high.

Market participants are anticipating Friday’s February employment report. This economic data release is anticipated to influence Federal Reserve interest rate policy expectations.

Multiple Federal Reserve officials have scheduled public appearances before Friday’s data publication. Interest rate trajectory expectations carry significant implications for cryptocurrency valuations, given their heightened sensitivity to liquidity dynamics.

Retail sector earnings announcements are also commanding investor attention this week. Target is slated to release quarterly results Tuesday, with Costco’s earnings report scheduled for later in the week.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants