Stock: Bitcoin Miner Hit All-Time High – Here’s Why")

TLDR

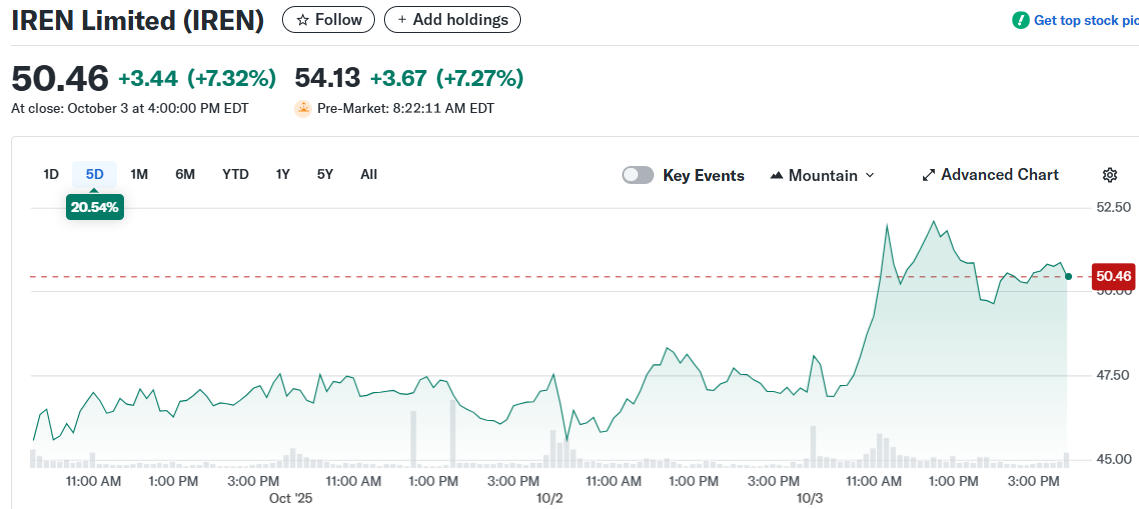

- Iris Energy stock reached $49.44 on October 3 and jumped to $53 in pre-market trading on October 6, 2025

- FY2025 revenue hit $501 million, up 168% year-over-year, with net income of $86.9 million

- Company purchased $674 million in GPUs, doubling fleet to 23,000 units for AI cloud expansion

- Stock has gained 460-500% over the past year with analysts setting price targets between $24 and $82

- Bitcoin mining operations benefit from $0.038/kWh power costs and 70-75% gross margins at current BTC prices

Iris Energy shares hit an all-time high of $49.44 on October 3, 2025. The stock climbed another 5% in pre-market trading on October 6, reaching approximately $53.

The surge caps a remarkable year for the bitcoin mining company. Shares have gained roughly 460-500% over the past 12 months.

Year-to-date gains stand at 382% as of early October. Trading volume spiked to over 16 million shares on October 3, well above normal levels.

The company reported record FY2025 results with revenue of $501 million, up 168% from the prior year. Net income reached $86.9 million, a turnaround from losses in FY2024.

Fourth quarter revenue hit $187.3 million with earnings per share of $0.19. Both figures topped analyst estimates.

Adjusted EBITDA nearly quadrupled year-over-year, climbing 395% to $269.7 million. Bitcoin prices more than doubled over the year, recently trading above $124,000 per coin.

Iris operates with average power costs of just $0.038 per kilowatt-hour using 100% renewable energy. That translates to breakeven costs around $34,000-$36,000 per bitcoin.

With current bitcoin prices, the company enjoys gross margins of 70-75% on mined coins. The April 2024 halving made low-cost operations more valuable as higher-cost miners struggled.

Major GPU Investment Targets AI Revenue

Iris announced a $674 million hardware purchase on September 22. The company bought 12,400 additional GPU accelerators from Nvidia and AMD.

That purchase doubled the total GPU fleet to approximately 23,000 units. Management raised its AI cloud revenue target to $200-250 million annually by December 2025.

The company expects AI cloud revenue to exceed $500 million by early 2026. For context, the segment generated only $16 million in FY2025.

Iris secured Nvidia “Preferred Partner” status in August. The company is building liquid-cooled facilities in British Columbia and Texas for the power-hungry hardware.

By late September, over 10,000 GPUs were online with thousands more arriving. Hash rate capacity reached 50 exahashes per second, about five times higher than a year prior.

The company secured 2.91 gigawatts of contracted power availability across sites, up 35% year-over-year. Operating data center capacity hit 810 megawatts by mid-2025.

A flagship project in Sweetwater, Texas features 2.0 gigawatt capacity. The first 750 megawatt phase is under construction for 2026.

Analysts Split on Valuation

Roth Capital quadrupled its price target from $35 to $82. Arete Research initiated coverage with a Buy rating and $78 target.

Bernstein raised its target from $20 to $75, valuing Iris like a data center provider rather than a traditional miner. Compass Point lifted its target to $50.

However, JPMorgan downgraded the stock to Underweight with a $24 price target. The firm warned shares might already price in future expectations requiring heavy capital expenditure.

As of early October, the stock carries 11 Buy ratings versus one Sell. The consensus price target sits around $47-$50.

The stock recently traded at over 100 times trailing earnings compared to 17 times for peer Marathon Digital. Bulls see unique positioning across crypto and AI while bears focus on execution risk.

Institutional interest has grown with 148 investors adding shares versus 115 reducing positions last quarter. Fidelity’s FMR LLC added 8.65 million shares worth approximately $126 million.

Company co-CEOs Daniel and Will Roberts each sold approximately one million shares in September as planned transactions. The company ended Q3 FY25 with $184 million in cash and a debt-to-equity ratio of 0.5.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants