Stock Soars as Top Analyst More Than Doubles Price Target")

TLDR

- RBC Capital upgraded Jumia Technologies from Sector Perform to Outperform with a price target increase from $6.50 to $15.00

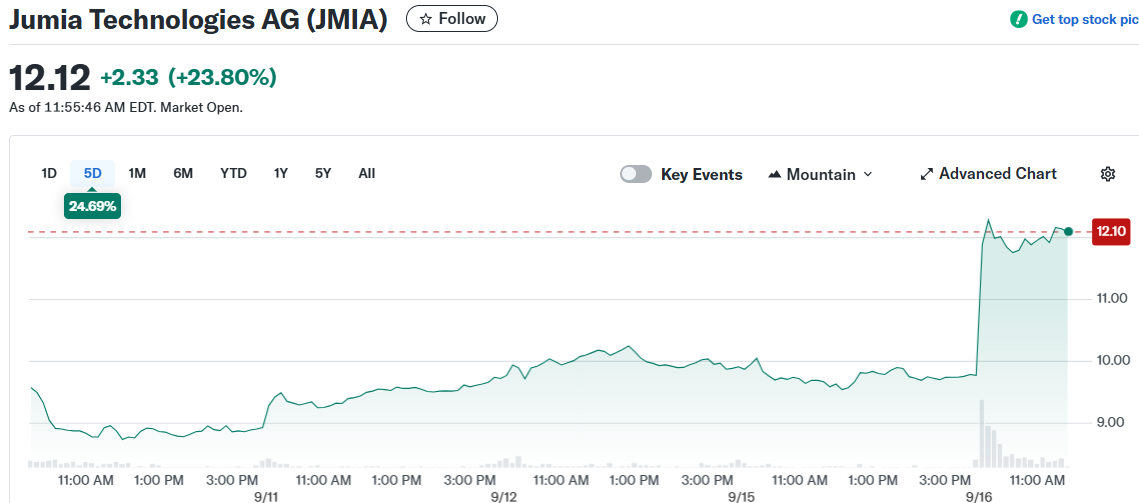

- The stock has surged over 318% in the past six months and traded at $9.79 following the upgrade

- Q2 2025 revenue hit $45.6 million, beating analyst expectations and showing 25% year-over-year growth

- RBC cited easing foreign exchange pressures as a key factor enabling supply expansion and order growth

- The analyst believes previous estimates may have been too conservative and sees potential for further upside

Jumia Technologies got a major vote of confidence from Wall Street as RBC Capital upgraded the African e-commerce company from Sector Perform to Outperform. The analyst firm also more than doubled its price target to $15.00 from $6.50.

The upgrade sent JMIA stock climbing, adding to what has already been a stellar run. The shares have surged over 318% in the past six months and currently trade at $9.79.

RBC analyst Brad Erickson made the call following virtual investor meetings with Jumia’s CEO and CFO. The sessions left the firm “incrementally positive” about the company’s outlook.

The analyst pointed to easing foreign exchange pressures as a key catalyst. RBC noted it had “underappreciated the magnitude of the headwinds” Jumia faced last year due to currency volatility.

Currency stability could enable further supply expansion and accelerate order growth. This represents a major shift from the challenges that previously weighed on the business.

Strong Q2 Results Drive Confidence

The upgrade comes on the heels of Jumia’s Q2 2025 earnings report. The company delivered revenue of $45.6 million, surpassing analyst expectations.

This marked a 25% increase compared to the same period last year. The revenue beat helped fuel investor optimism about the company’s trajectory.

Jumia also reported gross merchandise value growth of 6% to over $180 million. Management raised full-year 2025 guidance for both total orders and GMV.

The company maintains a healthy gross margin of 55.24%. However, profitability remains elusive with negative EBITDA of $69.49 million.

New Valuation Framework Reflects Growth Optimism

RBC’s new $15 price target uses a 6.8x EV/2026E revenue multiple. This compares to the previous target of $6.50 based on 2.7x EV/2026E revenue.

The higher valuation multiple reflects increased confidence in Jumia’s growth trajectory. The analyst believes the company can capitalize on improving operating conditions.

Erickson suggested his estimates “could still prove conservative.” This hints at potential for additional upside beyond the revised outlook.

The analyst zeroed in on order count development as a key metric. He theorized this could bring the company to profitability sooner than expected.

RBC speculated Jumia could hit breakeven by the end of 2026. This would represent a major milestone for the loss-making e-commerce platform.

Despite the upgrade, challenges remain. The company reported an operating loss that deepened to over $20 million from $16.5 million a year ago.

Earnings per share came in at -$0.12, slightly missing the forecast of -$0.11. The EPS miss was overshadowed by the strong revenue performance.

The stock surge reflects growing investor confidence in Jumia’s turnaround story. Currency headwinds that previously hampered growth appear to be subsiding.

RBC’s upgrade and price target hike represent a major shift in sentiment toward the African e-commerce play.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants