Key Highlights

- Investors await March CPI and February PCE inflation reports, the initial data since Iran conflict escalation

- March employment data showed 178,000 new positions, significantly exceeding forecasts of 65,000

- Crude oil has surged more than 50% following conflict outbreak, pushing national gasoline average beyond $4

- Delta Air Lines earnings release Wednesday will provide critical insight into aviation sector fuel cost pressures

- Major equity benchmarks concluded their five-week decline, posting gains exceeding 3%

Investors are preparing for an eventful trading week as critical inflation metrics, quarterly corporate results, and continuing Middle East conflict dynamics converge.

The S&P 500 advanced 1.6% over the previous five trading days, while the Dow Jones Industrial Average climbed 1.2%, and the Nasdaq Composite surged 2.2%. These gains halted a five-week downward trajectory across all three benchmarks. Year-to-date, the S&P 500 and Dow remain lower by 3.8% and 3.2%, respectively.

Last Friday’s employment situation report for March significantly outperformed analyst projections. The U.S. economy generated 178,000 nonfarm positions, substantially surpassing the consensus estimate of 65,000. This represented a sharp reversal from February’s 92,000 job decline.

“The key message is equilibrium,” stated Gina Bolvin, president of Bolvin Wealth Management Group. “Robust employment growth diminishes the immediate need for monetary easing, yet doesn’t alter the overall decelerating trajectory.”

Michael Feroli, JPMorgan Chase’s chief US economist, remarked the figures provided “somewhat greater assurance that economic expansion can endure the current energy cost spike without substantial lasting harm.”

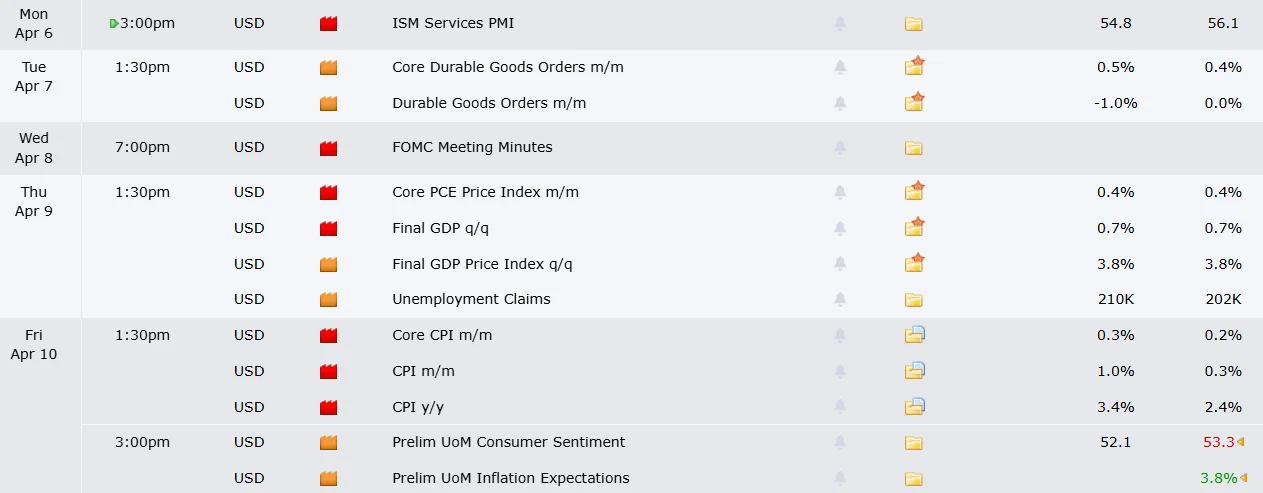

Critical Inflation Metrics Command Attention

Thursday will deliver the February Personal Consumption Expenditures index, a crucial inflation gauge closely monitored by Federal Reserve policymakers. Analyst consensus projects a 0.4% monthly advance and a 2.8% annual increase.

Friday presents the more significant release: March’s Consumer Price Index. Economic forecasters anticipate prices climbed 0.9% from the previous month and 3.4% on an annual basis. February’s CPI registered at 2.4% year-over-year. This upcoming release will mark the first measurement incorporating the Iran conflict’s inflationary impact.

National gasoline prices surpassed $4 per gallon during the past week, per AAA data. Goldman Sachs analyst Ben Shumway noted escalating prices are “contributing to further deterioration in consumer sentiment from already depressed levels.”

Andy Schneider, senior US economist at BNP Paribas, observed that “disruption in the Strait of Hormuz has materialized while tariff transmission continues,” noting that “the initial wave of crude price transmission will have appeared in March data.”

Goldman economist Manuel Abecasis characterized the current supply disruption as “less troubling than previous instances that generated inflation challenges,” pointing to its constrained magnitude and scope.

Corporate Results and Geopolitical Developments

Delta Air Lines releases quarterly earnings Wednesday during pre-market hours. The carrier’s financial performance is anticipated to reveal the aviation industry’s exposure to elevated jet fuel expenditures. Constellation Brands and Levi Strauss will also announce results during the week.

According to FactSet data, Wall Street forecasters project earnings expansion exceeding 13% for S&P 500 constituents overall.

Oil prices have climbed more than 50% since hostilities commenced five weeks prior. Maritime traffic through the Strait of Hormuz remains virtually nonexistent. President Trump conducted a Monday briefing alongside military leadership as a self-established deadline for strait reopening nears.

Capital.com analyst Daniela Hathorn observed that “financial markets have shifted from pricing in de-escalation optimism to assessing escalation likelihood.”

Paola Rodriguez-Masiu, Rystad Energy’s chief oil analyst, indicated the temporary cushion that previously constrained prices from pre-conflict petroleum inventories is now exhausted.

The Federal Reserve’s March policy meeting minutes will be published Wednesday at 2 p.m. ET. Market participants broadly anticipate the central bank will maintain current interest rates at its upcoming session later this month.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants