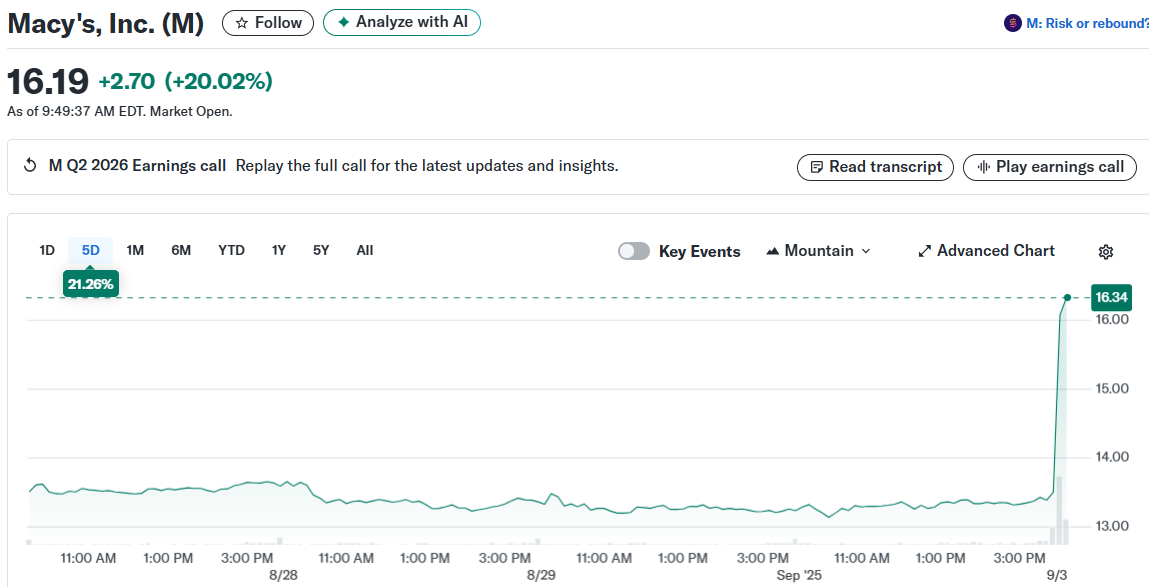

Stock Surges After Beating Q2 Earnings and Raising Full-Year Guidance")

TLDR

- Macy’s shares jumped over 10% in premarket trading after beating Q2 earnings estimates with 41 cents per share vs 18 cents expected

- The retailer posted its first positive same-store sales growth in 12 quarters, up 0.8% overall and 1.1% at focus stores

- Company raised full-year guidance for both earnings ($1.70-$2.05 vs $1.60-$2.00) and revenue ($21.15-$21.45B vs $21.0-$21.4B)

- CEO Tony Spring credited the “Bold New Chapter” turnaround strategy with improved performance at renovated stores

- Management remains cautiously optimistic despite ongoing tariff pressures and plans for selective price increases

Macy’s stock surged more than 10% in premarket trading Wednesday after the department store chain delivered earnings that crushed Wall Street expectations. The retailer posted adjusted earnings of 41 cents per share, more than doubling the 18 cents analysts had forecast.

Revenue came in at $4.81 billion, slightly ahead of the $4.76 billion estimate. While total sales dropped 2.5% year-over-year, this largely reflects the impact of over 60 store closures completed as part of the company’s restructuring plan.

The real story lies in same-store sales, which measure growth at locations open for more than a year. Macy’s posted 0.8% growth in this key metric, marking the first positive quarter after 12 straight quarters of declines.

This turnaround validates CEO Tony Spring’s “Bold New Chapter” strategy. The plan focuses resources on roughly 350 higher-performing stores while closing underperforming locations.

The 125 stores receiving priority investment with higher staffing and renovations outperformed the broader chain. These focus stores saw comparable sales growth of 1.1% on an owned basis.

“We’re just well positioned right now for the environment we’re in to take share, to deliver for our customers and to provide a better experience,” Spring told CNBC. The CEO highlighted strength in denim, women’s contemporary apparel, and watches as key growth drivers.

Strong Performance Across Brands

Macy’s portfolio extends beyond its namesake stores. Bloomingdale’s delivered comparable sales growth of 3.6% on an owned basis. Bluemercury, the company’s beauty chain, posted 1.2% growth.

Both brands have consistently outperformed the main Macy’s stores. Their continued strength provides stability as the flagship brand works through its transformation.

Credit card revenue also jumped $28 million to $153 million. This increase reflects improved customer engagement across the portfolio.

Spring emphasized the importance of multiple categories performing well. “When you think about the strength of a department store or a marketplace, it’s when multiple categories are working,” he said.

Guidance Boost Reflects Confidence

The company raised its full-year outlook on both earnings and revenue. Adjusted earnings are now expected between $1.70 and $2.05 per share, up from the previous range of $1.60 to $2.00 per share.

Revenue guidance increased to $21.15 billion to $21.45 billion from $21 billion to $21.4 billion. The modest bump reflects management’s growing confidence in the turnaround strategy.

This guidance raise comes after Macy’s slashed its outlook last quarter due to uncertainty around tariffs and consumer spending patterns. The company had previously struggled with inconsistent performance and declining foot traffic.

The updated projections assume consumers will remain “choiceful” in their spending during the second half of the year. Management expects shoppers to continue being selective about purchases.

CFO Tom Edwards said the company is exploring additional price increases on certain products due to tariff pressures. “We’re adjusting prices, but as appropriate, not broad-based and really assessing it with our partners in an effort to remain competitive,” Edwards explained.

The company has already implemented some price hikes to offset tariff costs. Spring noted that tariff impacts are now included in the company’s outlook.

Despite these challenges, Spring remains optimistic about consumer resilience. He said shoppers continue spending on new items and fashion, providing a foundation for continued growth.

The retailer’s inventory position heading into fall appears healthy. This positioning should help capitalize on seasonal shopping patterns and holiday demand.

Macy’s reported net income of $87 million, or 31 cents per share, for the quarter ended August 2. This compares to $150 million, or 53 cents per share, in the prior year period.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants