Stock: Analysts Raise Price Targets Ahead of Earnings. Time To Buy?")

TLDR

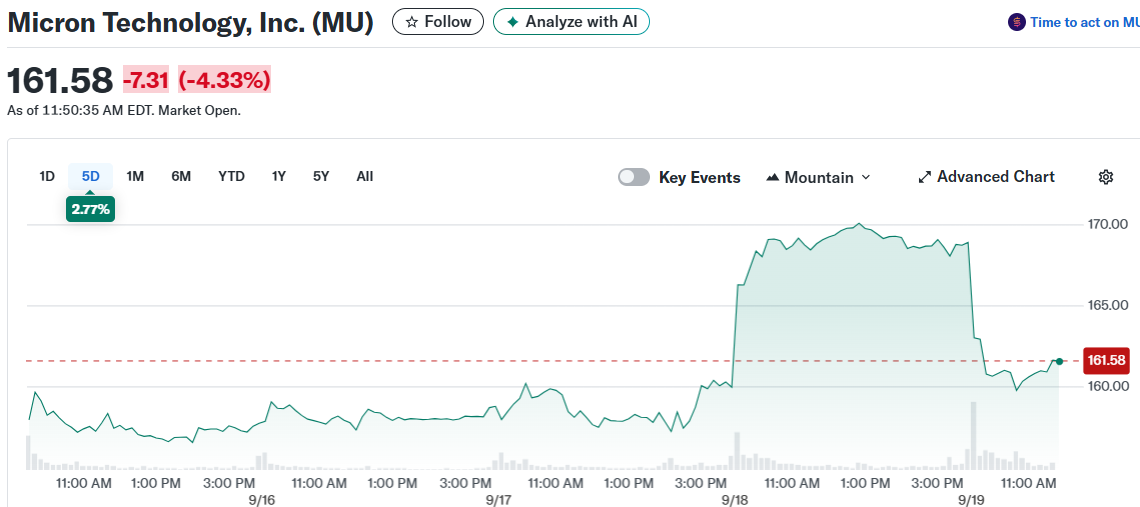

- Micron stock ended a 12-day winning streak with a 4% drop to $161.70, but still maintains 43% gains over that period

- Wedbush raised price target to $200 and Barclays to $175, both citing stronger cloud demand and improved memory pricing

- Analysts report an “unexpected uptick” in memory orders from cloud service providers in recent weeks

- The company is set to report fiscal fourth-quarter earnings Tuesday after market close, with analysts expecting earnings to more than double

- Wall Street consensus shows Strong Buy rating with average price target of $157.33

Micron Technology stock pulled back Thursday, falling about 4% to roughly $161.70 after closing at a record $168.89 the day before. The decline ended a remarkable 12-session winning streak that delivered 43% gains and marked the company’s best 12-day performance since March 2009.

The recent surge wasn’t driven by a single event. Instead, momentum built around better memory pricing and rising demand for AI infrastructure. Pullbacks after such strong runs are typical, even when the underlying story remains positive.

Wall Street Sees More Room to Run

Despite the pause, analysts remain bullish heading into next week’s earnings report. Wedbush maintained its Outperform rating while raising its price target to $200 from $165. The firm pointed to a clear pickup in orders from cloud service providers in recent weeks.

Barclays also stayed positive, reiterating its Outperform rating and lifting its target to $175 from $140. The firm expects results to come in ahead of guidance with a stronger outlook for upcoming quarters.

The combination of higher targets and steady ratings suggests Wall Street believes Micron’s earnings power can continue expanding. This confidence comes even after the stock’s impressive run.

Wedbush highlighted an “unexpected uptick” in memory demand from cloud players over recent weeks. This includes both DRAM and NAND memory tied to AI training and data-heavy workloads. When major cloud companies scramble for capacity, pricing and utilization typically improve.

Barclays suggested some of the NAND demand spike may relate to “large procurement efforts last week” in Silicon Valley. Even if timing plays a role, concentrated buying can tighten supply and strengthen pricing power.

Earnings in Focus

Micron is scheduled to report fiscal fourth-quarter results Tuesday after market close. Analysts polled by FactSet expect earnings to more than double to $2.79 per share, with revenue jumping 44% to $11.1 billion.

The company already raised guidance during its previous quarter. Management said August-quarter revenue would reach about $10.7 billion, well above the $9.9 billion analysts had projected at the time.

Data center revenue more than doubled in the May quarter as AI infrastructure buildouts accelerated. Profit soared 208% to $1.91 per share while revenue increased 37% to $9.3 billion.

The Federal Reserve’s recent quarter-point rate cut to a range of 4% to 4.25% has added fuel to the broader market rally. The move was widely expected but still triggered fresh buying across technology stocks.

Micron’s products enable AI models to learn and operate more efficiently. The rapid growth of data centers has created strong demand for the company’s memory and storage solutions.

Today’s pullback puts the prior record close at $168.89 as a key reference point for traders. Holding most of the recent gains into earnings would signal buyers remain in control.

The stock now trades with a Wall Street consensus Strong Buy rating among 29 analysts. This rating includes 25 Buy recommendations and four Hold ratings assigned over the past three months.

Micron’s average price target of $157.33 implies about 2% downside from current levels, though several recent upgrades suggest analysts see more upside potential than the consensus reflects.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants