Stock: Reaches All-Time High as Top Analyst Says ‘Load Up’ Now")

TLDR

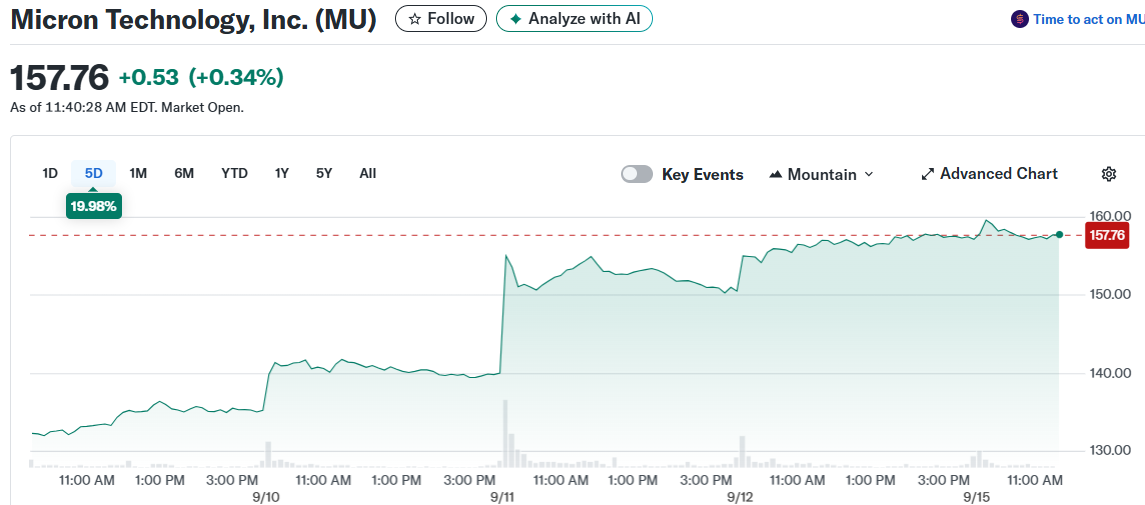

- Micron Technology (MU) stock hit an all-time high of $158.38 as the company prepares for Q4 earnings on September 23

- Deutsche Bank analyst Sidney Ho raised his price target to $175 and maintained a Buy rating, citing tight DRAM supply and stronger NAND pricing

- Wall Street expects Q4 earnings of $2.78 per share on revenues of $11.12 billion

- The stock has surged 80.37% over the past year with analysts maintaining a Strong Buy consensus rating

- Ho predicts gross margins above 50% driven by favorable supply-demand dynamics in memory markets

Micron Technology stock reached a new all-time high of $158.38 on Monday, setting the stage for what could be a pivotal earnings report next week. The memory chip maker is scheduled to release its fourth-quarter fiscal 2025 results on September 23.

Wall Street analysts are expecting earnings per share of $2.78 on revenues of $11.12 billion for the quarter. The company’s market capitalization now stands at $177 billion following the recent rally.

The stock’s impressive performance continues a strong upward trend that has seen shares climb 80.37% over the past year. This surge reflects growing investor confidence in the semiconductor company’s market position.

Deutsche Bank analyst Sidney Ho, who holds a 5-star rating, recently boosted his price target for Micron to $175 from $155. He maintained his Buy rating on the stock while pointing to several positive factors driving his outlook.

Memory Market Dynamics Support Growth

Ho highlighted tight supply conditions in the DRAM market as a key driver for Micron’s prospects. DRAM serves as fast memory for data that computers and servers need immediately.

The analyst expects DRAM supply to remain constrained into 2026. This constraint stems from high-bandwidth memory absorbing a growing share of bit capacity in the market.

These supply-demand dynamics are pushing up average selling prices for DRAM products. Ho believes this favorable pricing environment should support sustained margin expansion for Micron.

The analyst predicts gross margins will climb above 50% as these market conditions persist. This would represent a strong improvement in profitability for the company.

NAND Flash Market Shows Momentum

Ho also sees positive trends developing in the NAND flash storage market. NAND provides long-term storage used in solid-state drives and smartphones.

Device makers are increasing storage content in their products, creating stronger demand. Recent phone launches have contributed to this trend.

Enterprise demand for SSDs from hyperscale cloud providers is also helping support NAND pricing. This enterprise demand provides another revenue stream for memory companies like Micron.

Analyst Raises Revenue Projections

Based on these market trends, Ho increased his revenue forecast for calendar year 2026 to $54.3 billion. This represents a 3% increase from his previous estimates.

The analyst also raised his earnings per share projection for 2026 to $15.45, up 6% from his prior forecast of $14.55. These revisions reflect his confidence in Micron’s market position.

Ho addressed investor concerns about high-bandwidth memory pricing in 2026. He considers these worries overstated given Micron’s strong position in AI-related demand.

The analyst believes Micron can maintain market share and profitability in HBM even if pricing normalizes. This view contrasts with some investor fears about future pricing pressure.

Wall Street maintains a Strong Buy consensus rating on Micron stock. The rating is based on 25 Buy recommendations and four Hold ratings issued over the past three months.

The average price target among analysts stands at $153.19, which now implies about 2.57% downside from current trading levels. UBS has set an even higher price target of $185 for the stock.

Ho noted that management is unlikely to provide new details on HBM contract negotiations during the upcoming earnings call. This relates to uncertainty around 2026 supply and customer product launches.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants