Stock Surges as Three Analysts Raise Price Targets. Here’s Why")

TLDR

- Multiple Wall Street analysts raised Micron price targets in two days, with Wedbush setting highest at $200

- Strong demand for AI memory chips drives optimism, with HBM production sold out through 2025 and strong 2026 outlook

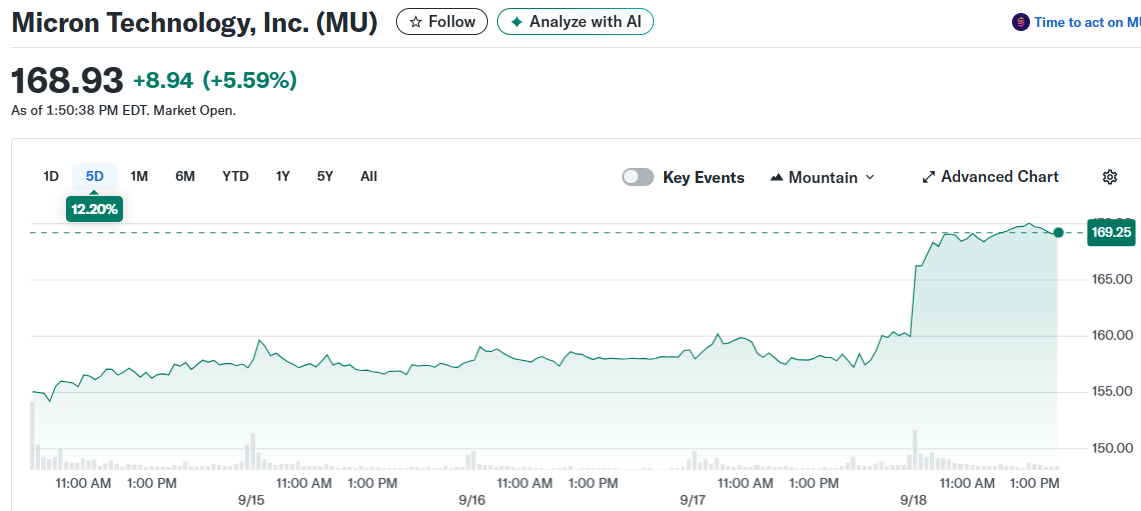

- Stock jumped 5.4% on analyst upgrades, reaching new 52-week high of $168.09

- DRAM pricing remains resilient while NAND flash demand grows due to hard drive supply shortages

- Analysts expect earnings to be 10x higher in 2025 compared to 2024, potentially doubling by 2027

Micron Technology stock surged 5.4% in morning trading as a wave of analyst upgrades highlighted the company’s position in the artificial intelligence memory market. Three major research firms raised their price targets within 48 hours.

The rally began yesterday when Wolfe Research and Susquehanna both increased their targets. Wolfe Research set a $180 price target, citing resilient DRAM pricing and growing NAND flash demand.

Susquehanna went higher with a $200 target. The firm pointed to strong high-bandwidth memory pricing that should hold through 2026.

Today brought the third upgrade from Wedbush, which matched Susquehanna’s $200 price target. The firm values Micron at 10 times peak earnings for next year.

Memory Demand Drives Analyst Confidence

The upgrades center on Micron’s role as a key supplier of specialized memory for AI applications. The company produces high-bandwidth memory chips essential for platforms like Nvidia’s Blackwell GB200.

Demand has been so strong that Micron’s HBM production is already sold out for 2025. The company also sees strong demand extending into 2026.

DRAM memory pricing has remained stable despite typical industry cycles. This resilience comes as AI applications require more advanced memory solutions.

NAND flash memory demand is also growing. Hard disk drive supply shortages are pushing customers toward flash storage alternatives.

Stock Performance Reflects Market Optimism

Micron shares hit a new 52-week high of $168.09 during the session. The stock has gained 92.5% since the beginning of the year.

The recent move follows another analyst upgrade just six days ago. Citigroup raised its price target to $175 from $150, maintaining a buy rating.

Wedbush argues that Micron could achieve better gross margins than during the last cyclical peak in 2018. This could lead to higher profits than current estimates suggest.

Analysts expect Micron’s 2025 earnings to be 10 times higher than 2024 results. Some forecasts show earnings potentially doubling again by 2027 to $13.70 per share.

The stock has been volatile over the past year with 26 moves greater than 5%. Today’s gain reflects meaningful news but not a fundamental shift in market perception.

Investors who bought $1,000 worth of Micron shares five years ago would now hold an investment worth $3,313. The company has benefited from the broader shift toward AI infrastructure and memory-intensive applications.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants