Stock: Wall Street Consensus Shows Strong Buy Rating Ahead of Earnings")

TLDR

- Micron expects Q4 EPS of $2.86 on $11.2B revenue, representing 45% annual growth

- August guidance raise signals strong AI data center memory demand exceeding expectations

- Stock surged 38% in September as analysts raised price targets following positive demand checks

- High-bandwidth memory pricing remains strong despite typical cycle expectations

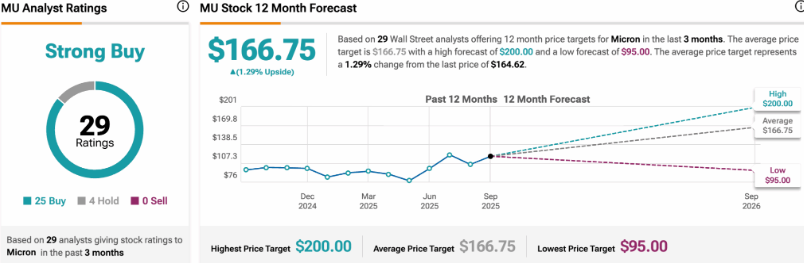

- 25 of 29 Wall Street analysts rate MU stock a buy ahead of Tuesday earnings

Micron Technology enters its fourth-quarter earnings report with exceptional momentum. The memory chip maker reports results Tuesday afternoon after raising guidance in August.

Wall Street analysts project adjusted earnings of $2.86 per share on revenue of $11.2 billion. These figures represent massive growth from last year’s $1.18 earnings per share.

AI Data Centers Drive Memory Revolution

The artificial intelligence investment boom has transformed Micron’s business model. Traditional memory cycles brought volatile demand and sharp price declines after initial strength.

This cycle breaks that pattern. AI training clusters require high-bandwidth memory positioned next to processors, creating sustained premium demand.

Micron now ships a larger portion of memory chips to data centers that prioritize performance over cost. This shift has improved profit margins and pricing stability.

The company’s August guidance increase came just weeks before quarter end. Such late-cycle adjustments typically indicate results locked in better than expected.

Ten analysts raised price targets in the past week alone. The average target reaches $166.44, slightly above current trading levels near $164.62.

Memory Pricing Defies Traditional Expectations

TD Cowen analyst Krish Sankar reports memory prices should continue rising in coming quarters. This defies typical patterns where prices drop deep into up-cycles.

Supply remains tight in DRAM while NAND trends improve. High-bandwidth memory continues as the standout performer driving growth.

Inventory levels stayed leaner than previous cycles. Cloud providers signed forward supply agreements, providing visibility and stability.

Q1 Outlook Critical for Sustained Growth

Tuesday’s Q4 results matter, but first-quarter guidance carries equal weight. Analysts expect Q1 revenue of $11.9 billion, up over 30% annually.

Management commentary on capacity additions and customer visibility will drive post-earnings moves. HBM production ramps and yield improvements remain key metrics.

Capital expenditure plans and manufacturing node transitions also factor into investor decisions. Supply discipline across the industry supports margin expectations.

Out of 29 covering analysts, 25 rate Micron a buy while four assign hold ratings. No analysts recommend selling the stock.

The memory maker’s strategic focus on AI applications has paid dividends through two years of growth. Whether this momentum continues depends on sustained data center buildouts.

Micron’s August guidance raise removed some earnings surprise potential. Attention now shifts to whether management can beat raised expectations and provide confident forward guidance.

The stock’s September rally has raised performance expectations. Strong results and optimistic guidance could extend gains, while any disappointment might trigger profit-taking.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants