Stock Jumps as Citi Raises Price Target to $175 Ahead of Earnings")

TLDR

- Citi boosted Micron’s price target to $175 from $150, maintaining a Buy rating ahead of September 23 earnings

- Analysts expect Micron’s Q1 guidance to exceed consensus due to higher DRAM and NAND pricing

- Memory upturn driven by limited production and strong data center demand, which represents over half of Micron’s revenue

- Citi’s fiscal 2026 earnings estimate sits 26% above Wall Street consensus at $15.02 per share

- AI demand for NAND memory expected to reach 34% of global market by 2029, worth $29 billion

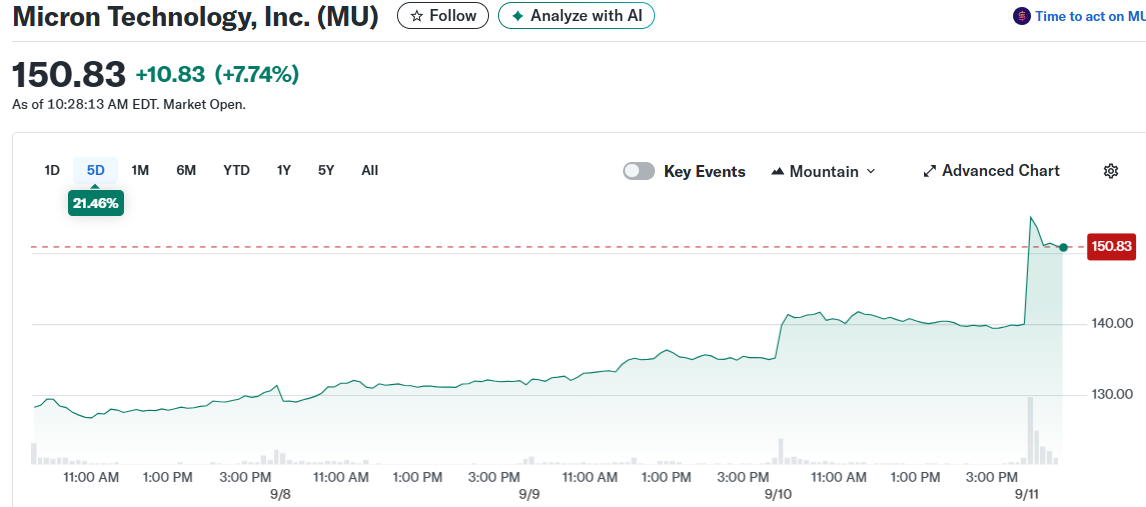

Micron Technology shares jumped 3.6% in premarket trading Thursday after Citi analyst Christopher Danely raised his price target on the memory chip maker. The new target of $175 represents a $25 increase from the previous $150 target.

Danely maintained his Buy rating on the stock. The price adjustment comes just days before Micron reports fiscal fourth-quarter earnings on September 23 after market close.

The analyst expects Micron to deliver in-line results for the quarter. However, he believes the company’s first-quarter guidance could surprise investors by coming in well above Wall Street expectations.

This optimistic outlook stems from anticipated higher sales and pricing for both DRAM and NAND flash memory products. The memory market continues to benefit from constrained production capacity meeting robust demand.

Data center customers drive much of this demand surge. This market segment now represents more than half of Micron’s total revenue, according to Citi’s research team.

Memory Market Dynamics

The ongoing memory upturn reflects a combination of supply and demand factors. Limited production capacity across the industry has helped maintain pricing power for memory manufacturers.

At the same time, demand has exceeded expectations, particularly from enterprise customers. Data centers require increasing amounts of memory to support cloud computing and artificial intelligence workloads.

Citi’s bullish stance on Micron extends beyond the immediate quarter. The firm’s fiscal 2026 earnings estimate of $15.02 per share sits 26% above the current Wall Street consensus.

This aggressive forecast reflects Danely’s confidence in the DRAM market recovery. He also highlighted Micron’s growing exposure to AI-related demand as a key growth driver.

AI Market Opportunity

The artificial intelligence boom has created new opportunities for memory chip companies. Morgan Stanley research indicates that AI applications will drive substantial growth in NAND flash memory demand.

The investment bank estimates that AI-related NAND demand will capture 34% of the global market by 2029. This represents an incremental $29 billion addition to the total addressable market.

Micron competes with Samsung, SK Hynix, Kioxia, and Western Digital in the global NAND market. The company has been gaining market share in enterprise solid-state drives in recent years.

According to Morgan Stanley, Micron’s revenue share in the eSSD segment now approaches that of SK Hynix and Solidigm combined. This represents a notable achievement given Micron’s historically smaller scale in NAND production.

The company posted record revenue in its fiscal third quarter, driven partly by AI-related demand. Last month, Micron raised its current quarter guidance, citing improved DRAM pricing and strong execution.

Citi’s new $175 price target makes the firm one of the more optimistic voices on Wall Street. Baird, Rosenblatt Securities, and J.P. Morgan maintain even higher targets above $185 per share.

The analyst community remains broadly positive on Micron’s prospects. Of 42 analysts tracked by FactSet, 36 rate the stock at Buy or equivalent ratings.

Analysts surveyed by FactSet expect fourth-quarter adjusted earnings of $2.53 per share on revenue of $11.1 billion. Peers Applied Materials gained 3.62% while Advanced Micro Devices declined 2.21% in Thursday’s premarket session.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants