Stock: JPMorgan Raises Price Target to $100 After Earnings Beat")

TLDR

- Nike reported Q1 earnings of 49 cents per share, crushing analyst estimates of 27 cents, while revenue grew 1% to $11.7 billion versus expectations for a 5% decline

- Wholesale revenue surged 7% year over year with running products leading the way, and the spring order book shows growth compared to last year

- Gross margin dropped 3.2 percentage points to 42.2% due to discounting and tariffs, while China sales fell 9% and Converse revenue declined 27%

- JPMorgan lifted its price target to $100 from $93 and raised fiscal 2026 EPS forecast to $1.42, maintaining an Overweight rating

- Nike shares jumped 3.5% in after-hours trading to $72.15, though the stock remains down 7.8% year to date

Nike delivered first quarter results that exceeded Wall Street expectations. The athletic apparel company reported earnings of 49 cents per share for the quarter ended August 31.

Analysts had forecast just 27 cents per share. Revenue reached $11.7 billion, climbing 1% from the prior year.

The Street expected $11 billion in revenue. That would have marked a 5% drop.

The wholesale business showed real strength. Wholesale revenues jumped 7% year over year.

Running products powered much of the growth. The category resonated with consumers.

CEO Elliott Hill has focused on rebuilding wholesale partnerships. Previous management had distanced the company from these retailers.

Strong Order Book Points to Future Growth

The spring order book offers encouraging data. Orders are running above last year’s levels.

This suggests full-year wholesale revenue could return to growth. Nike expects second-quarter revenue to decline by a low single-digit percentage.

This matches analyst projections for a 3% decrease. The company forecasts gross margins will fall between 3 and 3.75 percentage points.

However, challenges remain visible in the numbers. Gross margin declined 3.2 percentage points to 42.2% in Q1.

Discounting to clear old inventory drove the margin pressure. Higher North American tariffs added to the squeeze.

Net income dropped 31% from last year despite the earnings beat. The Converse brand struggled with a 27% sales decline.

Direct-to-consumer sales fell 4%. China sales dropped 9% as store traffic weakened.

Tariffs and Consumer Caution Create Headwinds

More discounting was needed to drive Chinese demand. Hill said the team is moving urgently to improve China performance.

They’re emphasizing performance wear and refreshing inventory. These efforts will take time to deliver results.

CFO Matthew Friend acknowledged the recovery path won’t be smooth. He said progress will vary across different business segments.

External factors are weighing on performance. U.S. consumers remain cautious with spending.

Tariffs have escalated quickly. Southeast Asia tariffs stood around 10% at the last earnings report.

Now they’re closer to 20%. The company expects annual tariff costs of roughly $1.5 billion.

That’s up from a previous $1 billion estimate. Hill told investors Nike has much left to prove.

JPMorgan raised its Nike price target to $100 from $93. The bank kept its Overweight rating.

JPMorgan increased its fiscal 2026 earnings forecast to $1.42 per share from $1.32. Other analysts also adjusted their targets higher.

Morgan Stanley moved to $72. Stifel increased to $68.

HSBC lifted its target to $90. Nike shares are down 7.8% this year.

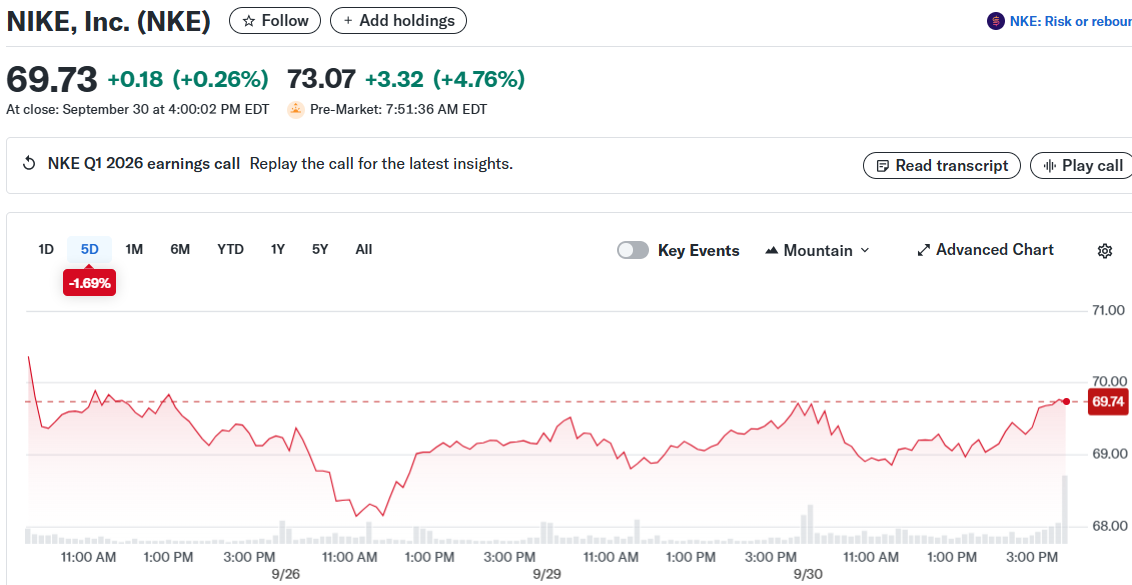

The stock has fallen roughly 30% over three years. Shares closed at $69.65 and rose to $72.15 after hours.

The higher spring order book provides concrete evidence that wholesale partners are restocking Nike inventory. This marks a turnaround from the previous strategy that pulled back from wholesale distribution.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants