Stock: Surges After Hours as Wholesale Strength Lifts Sentiment Despite Profit Drop")

TLDR

- Nike’s Q1 revenue edges up, but margins shrink and profits tumble 31%.

- Wholesale strength offsets digital slump in Nike’s mixed Q1 2026 report.

- Nike Q1 beats sentiment: shares rise despite profit and margin squeeze.

- Digital drop hits Nike Direct as wholesale sales drive modest growth.

- Nike stock jumps after hours as Q1 shows resilience in wholesale gains.

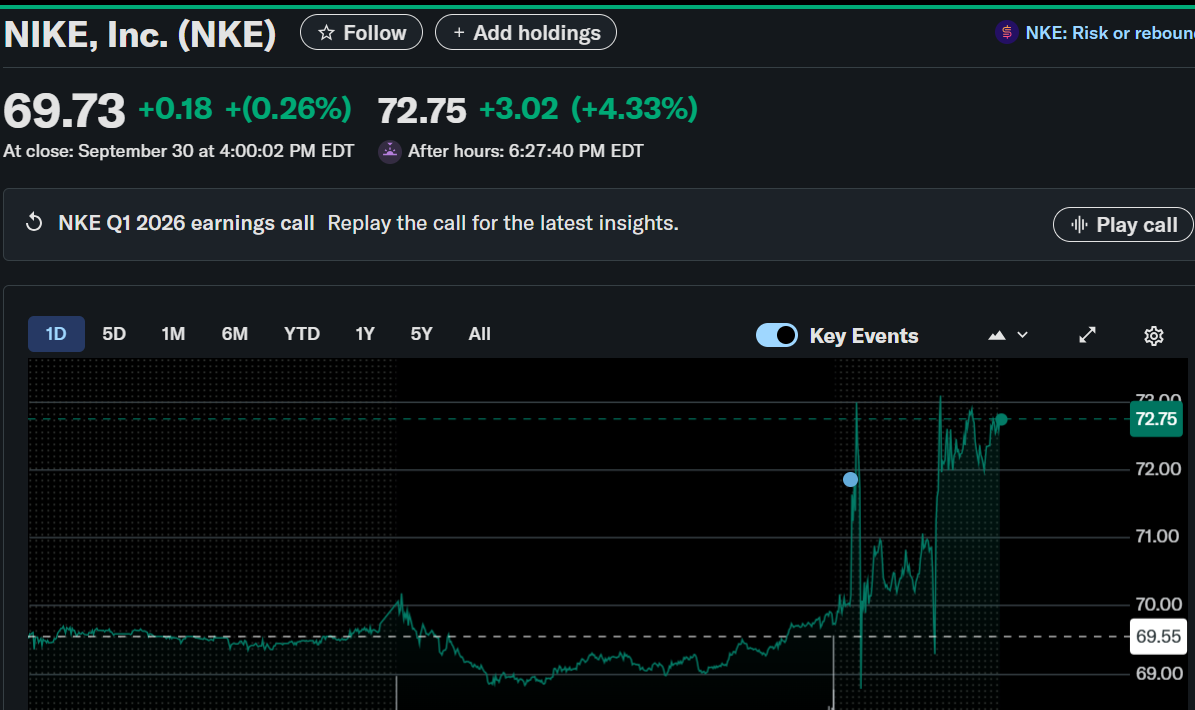

Nike Inc. experienced a noticeable market reaction following the release of its Q1 2026 earnings report. The stock rose modestly by 0.26% during regular hours to $69.73 and surged 4.33% after hours to $72.75. The after-hours gain came despite a sharp decline in net income and earnings per share.

Wholesale Growth and Mixed Revenue Trends Boost Market Response

Nike posted $11.7 billion in total revenue for the quarter ending August 31, 2025. This marked a 1% increase on a reported basis, but a 1% decline when adjusted for currency effects. While top-line growth was limited, wholesale revenues rose 7% to $6.8 billion, offsetting weaknesses elsewhere.

Nike Direct revenues fell 4% to $4.5 billion, due to a 12% drop in digital sales. Retail store revenues declined by 1%, signaling continued pressure in consumer-facing channels. However, the wholesale channel’s resilience contributed to stronger-than-expected sentiment post-market.

Brand performance was uneven across geographies, with North America showing strength and Greater China weighing down overall results. The NIKE Brand pulled in $11.4 billion in revenue, up 2% on a reported basis and flat when adjusted for currency. Converse revenue tumbled 27% to $366 million, showing sharp weakness globally.

Margin Contraction and Profit Slide Reflect Pricing Pressures

Gross margin shrank by 320 basis points to 42.2%, driven by lower average selling prices and an unfavorable channel mix. Tariff-related costs in North America further pressured margins, as did elevated discounts across key product lines. This erosion in margin directly impacted earnings.

Nike’s net income fell 31% to $0.7 billion compared to the prior year. Diluted earnings per share decreased by 30%, landing at $0.49 for the quarter. Despite reduced selling and administrative expenses, profit declines signaled ongoing challenges in restoring full operational efficiency.

Operating overhead stayed flat at $2.8 billion, while demand creation expense dropped 3% to $1.2 billion. The decrease in marketing investment reflected fewer marquee sports events this year. However, higher spending on sports partnerships provided partial offset.

Strategic Focus and Shareholder Returns Anchor Long-Term View

Nike highlighted ongoing progress in North America, Running, and Wholesale through its “Win Now” actions. The company remains focused on realigning operations to improve execution across all categories and regions. Management reiterated its long-term commitment to unlocking value through a reshaped strategy.

The quarter ended with $8.6 billion in cash and equivalents, down $1.7 billion year-over-year. Inventory stood at $8.1 billion, falling 2% despite increased product costs from tariffs. The company continues managing inventory proactively amid shifting demand patterns.

Nike returned $714 million to shareholders, with $591 million paid in dividends and $123 million spent on share repurchases. The ongoing $18 billion repurchase program has now retired 124.4 million shares worth $12.1 billion. This consistent capital return track record supports confidence in future performance.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants