Stock: What Analysts Expect Ahead of Tuesday Earnings")

TLDR

- Nike reports Q3 earnings Tuesday after close with analysts forecasting $11B revenue, down 5% year-over-year

- New CEO Elliott Hill leads turnaround efforts after company brought him back from retirement

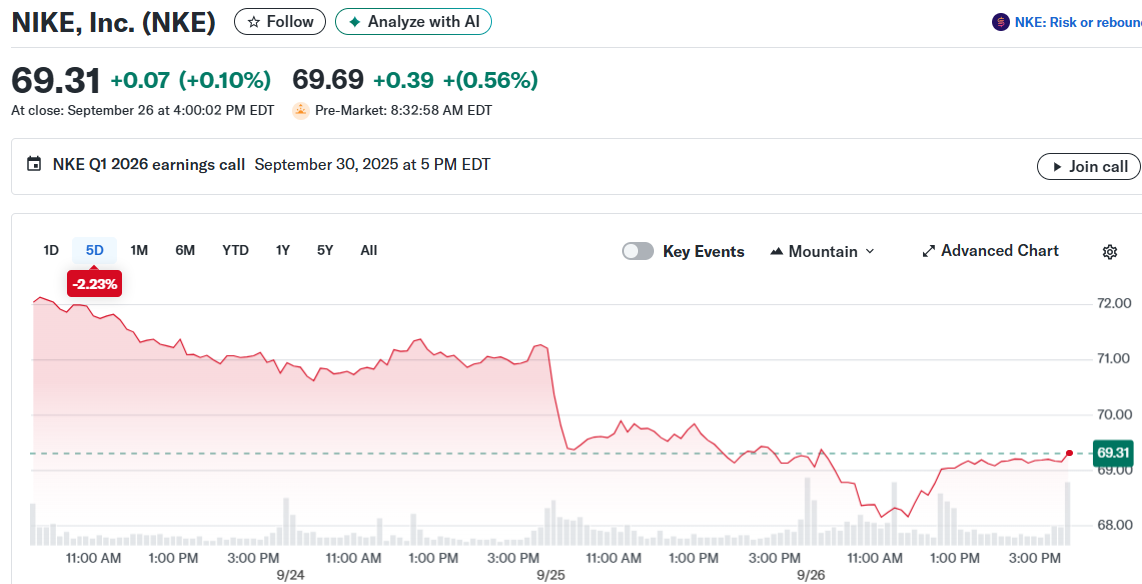

- Stock trades at $69.31 versus analyst price target of $79.57, showing potential upside

- Nike offers 2.25% dividend yield while investors wait for business recovery

- Company faces headwinds from product innovation gaps and wholesale relationship issues

Nike prepares to report third-quarter earnings Tuesday after market close as investors search for signs of recovery. Analysts expect revenue of $11 billion, representing a 5% decline from the same period last year.

The athletic apparel giant beat expectations last quarter with $11.1 billion in revenue. However, this still marked a 12% year-over-year decrease, highlighting ongoing challenges.

Wall Street forecasts adjusted earnings of $0.27 per share for the current quarter. Analyst estimates have remained relatively stable over the past month, suggesting confidence in their projections.

Nike stock has underperformed recently, dropping 6.7% over the past month. This contrasts with the broader consumer discretionary sector, which gained 1.2% during the same period.

The company currently trades at $69.31, well below the average analyst price target of $79.57. This gap suggests potential upside if Nike delivers better-than-expected results or shows progress on its turnaround plan.

New Leadership Drives Change

Nike made a strategic leadership change during fiscal 2025 by bringing back longtime executive Elliott Hill as CEO. Hill previously spent decades at the company before retiring, giving him deep institutional knowledge.

His established relationships with key wholesale partners could prove valuable. Nike has struggled with strained retailer relationships in recent years, impacting distribution and sales.

The company faces multiple challenges including lack of product innovation and softer sportswear demand. Competition from newer brands has also pressured market share in key categories.

Nike’s recovery in China has been slower than anticipated. The region represents a key growth market as middle-class populations expand with increasing disposable income.

Long-Term Investment Case

Despite near-term challenges, Nike maintains strong fundamentals for patient investors. The company’s global brand recognition and pricing power remain intact across most markets.

Nike’s gross margin of 42.21% demonstrates healthy profitability despite current pressures. The company’s $102 billion market capitalization reflects its industry-leading position.

The stock offers a 2.25% dividend yield, providing income while the turnaround develops. Nike has historically maintained dividend payments even during difficult operating periods.

Shares have declined 25% over the past three years, creating what some analysts view as an attractive entry point. The 52-week trading range spans from $52.28 to $89.75.

Developing markets including Latin America offer long-term growth potential. These regions feature expanding middle-class populations with rising athletic apparel spending.

Tuesday’s earnings report could provide clarity on Nike’s progress under Elliott Hill’s leadership. The company’s response to competitive pressures and innovation gaps will be closely watched.

Nike’s brand strength has proven resilient through previous challenges. The current difficulties appear more execution-related than fundamental brand issues.

Elliott Hill officially took the CEO role during fiscal 2025 as the company works to rebuild wholesale partnerships and accelerate product innovation.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants