Stock: August Delivery Records and Q2 Earnings Drive JPMorgan Upgrade")

TLDR

- NIO hit record 31,305 August deliveries, up 55.2% year-over-year

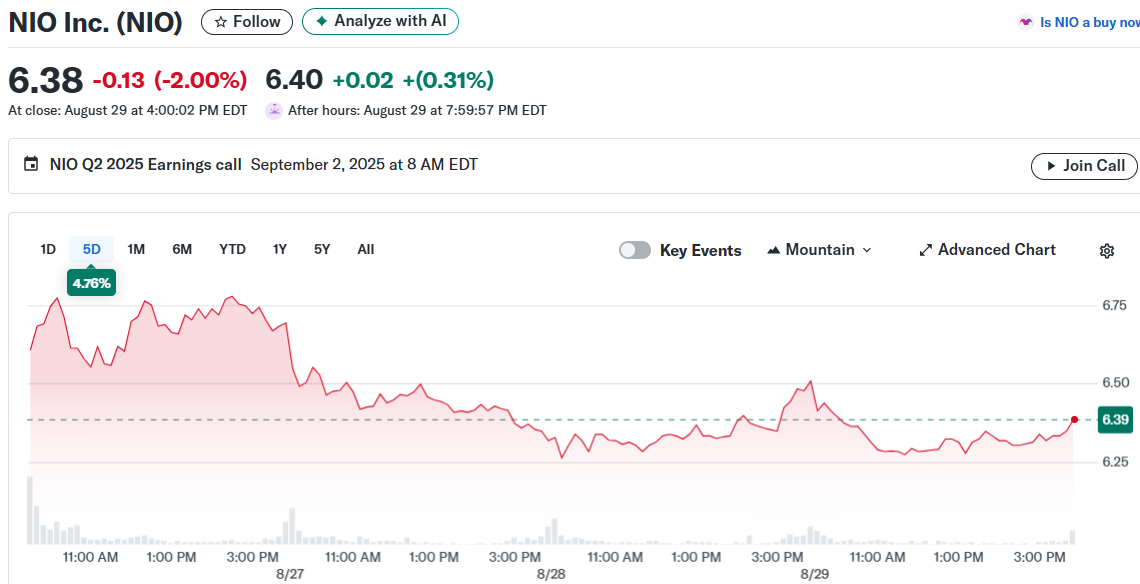

- Q2 earnings due September 2 with expected $0.31 loss per share improvement

- JPMorgan upgraded to Buy, $8 price target citing product expansion

- Stock gained 46.3% year-to-date on ES8 launch and Onvo brand growth

- Wall Street maintains Moderate Buy with $5.01 average price target

NIO crushed delivery expectations in August 2025 with a record 31,305 vehicles delivered. The 55.2% year-over-year jump marks the Chinese EV maker’s strongest monthly performance ever.

Total deliveries now stand at 838,036 vehicles through August 2025. The surge comes from all three NIO brands: premium NIO vehicles, family-focused ONVO, and compact FIREFLY models.

Shares have rocketed 46.3% year-to-date ahead of Q2 earnings on September 2. The strong rally reflects investor confidence in NIO’s expanding product lineup and pricing strategy.

Wall Street expects a $0.31 per share loss for Q2, improving from the $0.34 loss a year ago. Revenue forecasts center on $2.73 billion, with estimates between $2.52 billion and $2.91 billion.

Product Strategy Powers Growth

NIO recently launched the ES8 three-row SUV, now available for pre-orders across China. The company also cut prices on its long-range models to compete directly with Tesla’s six-seater offerings.

The mass-market Onvo brand has emerged as a key growth driver. The L90 SUV leads this lineup, targeting price-conscious families seeking premium EV features.

Analyst Optimism Builds

JPMorgan’s Nick Lai upgraded NIO to Buy from Hold, raising his price target to $8 from $4.80. The 26% upside potential reflects confidence in NIO’s broader product range and improving consumer sentiment.

Lai projects 50% delivery growth in 2025 and 47% in 2026. He expects profitability by late 2026 if margins continue recovering from current levels.

The analyst placed NIO on “positive catalyst watch” for upcoming events. These include Q2 earnings, Nio Day in September, and November’s Guangzhou Auto Show.

Wall Street maintains a Moderate Buy consensus with four Buy ratings, five Holds, and one Sell. The $5.01 average price target suggests 21% downside from current levels.

China’s economic slowdown and fierce EV competition remain key risks. Consumer spending has weakened while dozens of domestic brands compete for market share.

NIO’s record August delivery performance positions the company well heading into Q2 earnings. Investors will watch for margin improvements and 2025 delivery guidance updates.

The company’s three-brand strategy appears to be gaining traction with Chinese consumers. August’s 31,305 deliveries represent NIO’s highest monthly total on record.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants