TLDR

- Mizuho Securities analyst Vijay Rakesh raised NIO’s price target to $6 from $3.50 while maintaining a Neutral rating after Q2 earnings

- NIO reported Q2 revenue of $2.65 billion, up 9% year-over-year but missed consensus estimates of $2.73 billion

- The company posted adjusted EPS of $0.32, beating the forecast of $0.31, though reported a loss of $0.32 per share missing expectations by $0.02

- NIO guided for 89,000 deliveries in Q3, representing 44% year-over-year growth, but full-year targets of 120,000-150,000 units may be challenging

- Stock traded up 3% to $6.58 following earnings, with institutional investors increasing stakes and mixed analyst sentiment across Wall Street

NIO Inc. delivered mixed second-quarter results that prompted one top analyst to boost his price target while warning of challenges ahead. The Chinese electric vehicle maker reported revenue of $2.65 billion for Q2, representing a 9% increase from the same period last year.

The revenue figure fell short of Wall Street’s consensus estimate of $2.73 billion. However, the company managed to beat earnings expectations on an adjusted basis. NIO posted adjusted earnings per ADS of $0.32, topping the forecast of $0.31.

The earnings picture was more complicated when looking at reported figures. The company posted a loss of $0.32 per share, missing analyst expectations of a $0.30 loss by $0.02. This miss highlighted ongoing profitability challenges facing the EV maker.

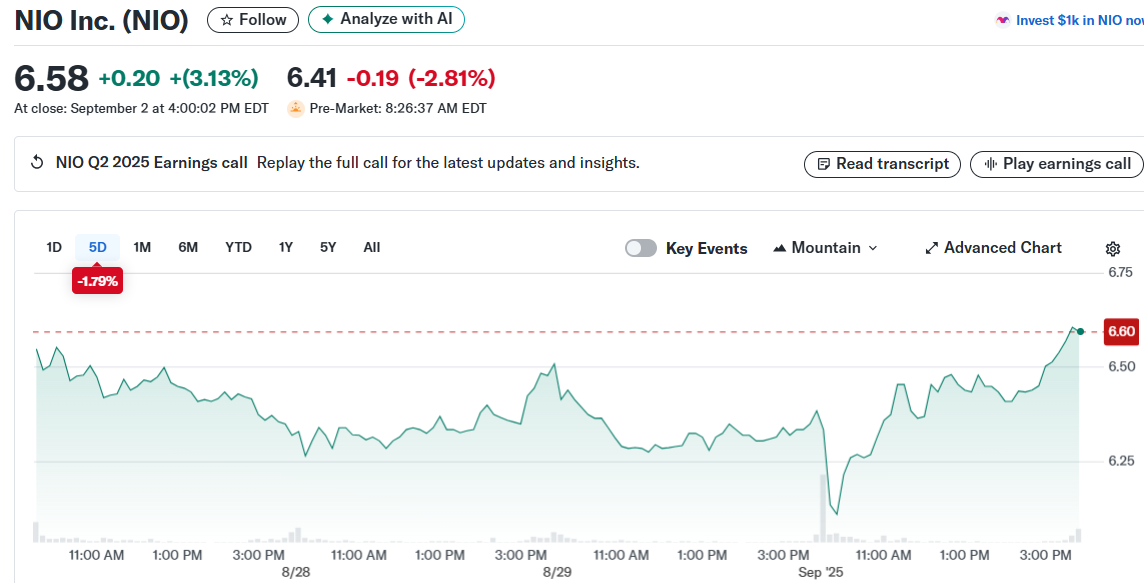

Following the earnings release, NIO stock climbed 3% to close at $6.58. The positive market reaction came despite the revenue shortfall. Investors appeared to focus on the adjusted earnings beat and forward-looking guidance.

Mizuho Securities analyst Vijay Rakesh responded to the results by raising his price target on NIO to $6 from $3.50 per share. He maintained his Neutral rating on the stock. Rakesh ranks 121 out of more than 10,000 analysts tracked by TipRanks and has a 60% success rate with an average return of 21.20% per rating.

Production Ramp and Delivery Outlook

Rakesh highlighted stronger demand for NIO’s newer vehicle models in his analysis. The ES8 and Onvo L90 are seeing increased production as the company scales manufacturing. NIO provided guidance for 89,000 deliveries in the third quarter, which would represent 44% growth compared to Q3 2024.

The delivery outlook faces some hurdles according to the analyst. NIO’s full-year target of 120,000 to 150,000 units may prove difficult to achieve. The company would need to increase its current monthly delivery pace of approximately 37,000 vehicles to reach the higher end of that range.

Production improvements have started to show up in the company’s margins. Vehicle gross margins improved to 10.3% in the second quarter. Overall gross margin came in at 10%, which was slightly below analyst forecasts.

Rakesh expects margins to continue improving in Q3, projecting gross margins of around 10.7%. Lower material costs and increased sales of the L90 model should drive the improvement. The analyst cautioned that NIO’s long-term margin targets above 20% remain challenging given intense price competition in China’s EV market.

Future Product Pipeline and Valuation

NIO has several new models planned for 2026 that could serve as growth catalysts. The ES9 and ES7 are expected to launch next year. The company’s upcoming Investor Day in late September will showcase the ES8 and NIO’s proprietary NX1931 chip technology.

While new product launches could boost demand, Rakesh expressed caution about maintaining momentum beyond initial release periods. The competitive landscape in China’s EV market continues to intensify with numerous manufacturers vying for market share.

From a valuation perspective, NIO currently trades at approximately 0.8x projected 2026 sales. This multiple is roughly in line with peers XPeng and Li Auto. Rakesh views the stock as fairly valued given the balance between improving EV demand and ongoing margin pressures.

Institutional investors have been actively adjusting their positions in NIO. Franklin Resources increased its stake by 50.9% in Q2, while First Trust Advisors boosted its holdings by 67.4%. Vident Advisory more than doubled its position with a 110.4% increase. Institutional investors and hedge funds now own 48.55% of NIO’s stock.

The broader analyst community remains divided on NIO’s prospects. Recent price target changes have ranged from Barclays lowering its target to $3.00 to JPMorgan upgrading shares with an $8.00 target. The stock currently has a Hold rating based on six Buy ratings, five Hold ratings, and one Sell rating among analysts.

NIO stock has gained 51% year-to-date despite the recent earnings-related volatility. The company trades with a market capitalization of $13.31 billion and maintains a beta of 1.20. The stock’s 50-day moving average sits at $4.61, while the 200-day average is $4.20.

The company reported a negative net margin of 35.51% and a negative return on equity of 286.45% in the most recent quarter. NIO updated its Q3 2025 guidance following the earnings release but did not provide specific EPS projections.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants