Stock: Technical Consolidation Ahead of August 27 Results")

TLDR

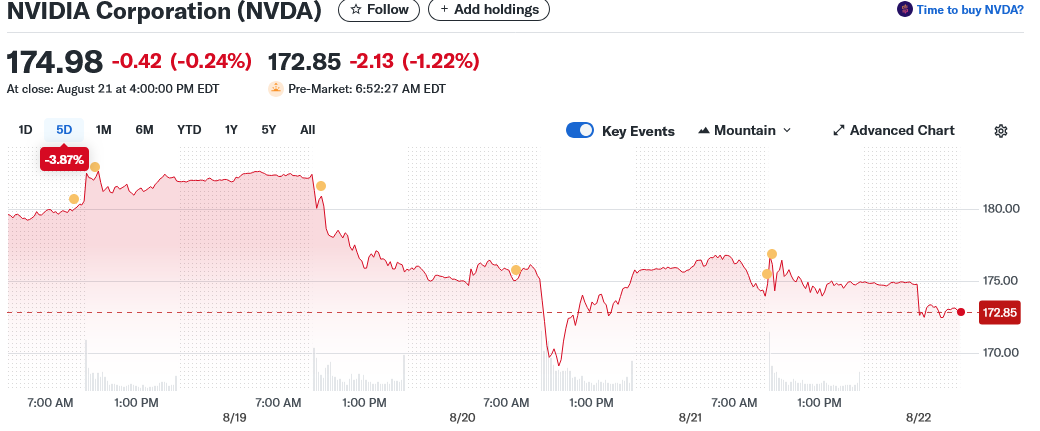

- Nvidia stock trades at $174.98, down 0.24%, showing technical consolidation ahead of Q2 earnings on August 27

- Company secured deal with Trump Administration allowing 15% revenue-sharing to resume H20 chip sales to China

- Nvidia developing new B30A processor for China market, delivering 50% power of flagship Blackwell B300 chip

- Wall Street analysts raise price targets despite AI sector skepticism, with Susquehanna lifting target to $210

- China AI chip market could reach $50 billion annually, representing major revenue opportunity for Nvidia

Nvidia stock trades at $174.98, reflecting a modest 0.24% decline as investors position ahead of quarterly results.

Short-term technical indicators present a mixed picture for the AI chip leader. The stock faces resistance at $180 and $185.50, while support levels sit at $172 and $165. Moving averages tell a tale of two timeframes, with short-term signals flashing bullish while longer-term indicators lean bearish.

Trading volume has declined recently, suggesting market participants are holding back until fresh catalysts emerge. The compression in Bollinger Bands points to reduced volatility and a potential breakout move following earnings.

Revenue Sharing Deal Opens China Door

Nvidia CEO Jensen Huang’s lobbying efforts have paid dividends. The company struck a deal with the Trump Administration that allows resumed sales of H20 chips to China through a 15% revenue-sharing arrangement with the U.S. government.

The agreement comes after Nvidia took a $4.5 billion charge in Q1 related to suspended H20 chip sales. These specialized processors were designed to meet strict U.S. export restrictions while providing computational power for AI applications.

China represented $17 billion in sales during fiscal 2025, accounting for roughly 13% of total revenue. Wall Street had projected a potential $26 billion revenue hit from the suspension.

The revenue-sharing structure may pressure margins but preserves access to a crucial market. Huang estimates China’s AI chip market could reach $50 billion annually in coming years.

Reports indicate Nvidia is developing a new processor specifically for Chinese customers. The B30A chip would be based on the company’s Blackwell architecture but deliver half the computational power of the flagship B300 processor.

President Trump previously indicated openness to a reduced-capacity Blackwell chip, suggesting he’d consider a deal on a processor with “30% to 50%” less computing power. The B30A appears to align with this framework.

Analyst Targets Rise Despite Sector Caution

Wall Street firms continue lifting price targets despite growing skepticism around AI valuations. Susquehanna raised its 12-month target from $180 to $210 on August 21, citing optimism around AI infrastructure demand and Blackwell chip expectations.

KeyBanc followed with a revised target of $215. TD Cowen projects shares reaching $235, reflecting confidence in the company’s market position.

The upgrades come as broader tech indices face pressure and traders question AI stock valuations. Nvidia serves as the primary barometer for AI sector sentiment, making earnings results particularly consequential.

Analysts and investors await clarity on China revenue guidance during the August 27 earnings call. The inclusion of H20 chip shipments and potential B30A sales could materially impact forward-looking statements.

Export licensing requirements and the 15% government revenue share add complexity to China-related projections. Management guidance on these factors will likely influence post-earnings stock movement.

Current Wall Street estimates project $200 billion in fiscal 2026 revenue, $257 billion in fiscal 2027, and $302 billion in fiscal 2028. These models may not fully reflect the restored China opportunity.

Technical Setup Points to Breakout Potential

The stock’s current consolidation pattern suggests a decisive move following earnings. Technical analysis indicates NVDA could break above $185.50 on strong results, potentially targeting previous highs above $200.

Conversely, disappointing earnings or weak guidance could trigger a decline below $172 support. Such a move might open the path toward $165, testing investor conviction in the AI growth story.

The company’s valuation sits below 30 times next year’s projected sales. This multiple appears reasonable given the growth trajectory and market opportunity, particularly with China access restored.

Nvidia’s position in AI infrastructure remains dominant as demand for advanced processors continues growing. The Blackwell architecture represents the next generation of AI computing power, even in reduced-capacity versions designed for export compliance.

The B30A development demonstrates Nvidia’s ability to navigate regulatory constraints while maintaining market access. This adaptability strengthens the investment thesis for those betting on continued AI adoption.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants