Stock: Analysts Raise Target Before Wednesday Earnings. Here’s Why")

TLDR

- Nvidia stock flat at $177.93 before Wednesday earnings despite China H20 processor sales uncertainty

- Stifel raises price target to $212 from $202 on resumed shipments and GB300 demand

- Chinese government reportedly banned domestic companies from buying H20 chips

- Analysts expect beat-and-raise quarter from Blackwell GPU volume deployments

- Second quarter likely generated zero China revenue despite export control reversals

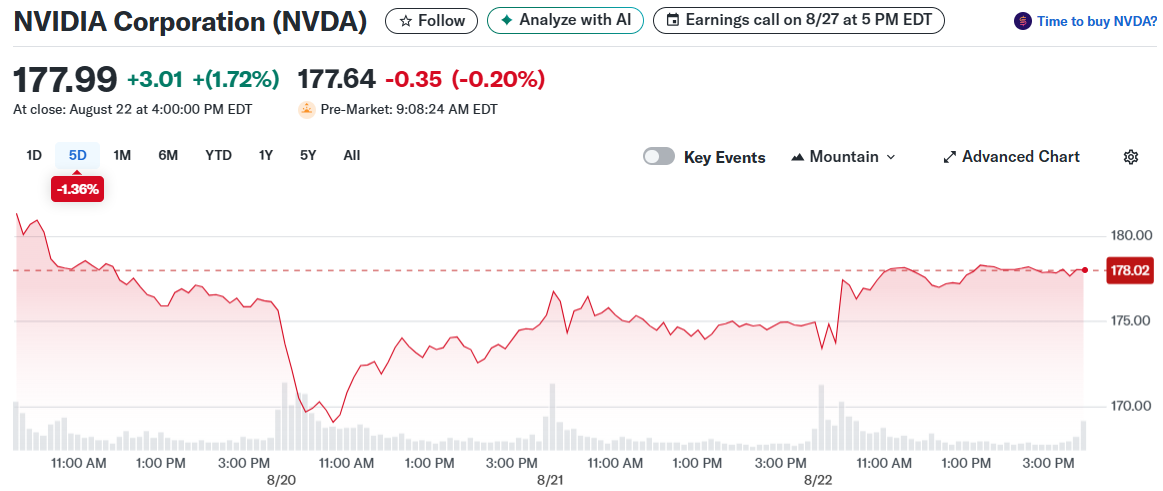

Nvidia stock remained unchanged in premarket trading as investors balanced China sales concerns against strong analyst sentiment ahead of Wednesday’s earnings report.

Shares traded at $177.93 Monday morning after gaining 1.7% Friday during the broader market rally. The AI chip leader faces questions about maintaining momentum in its second-largest market.

China Export Restrictions Create Headwinds

Recent reports suggest China’s government instructed domestic companies to stop purchasing Nvidia’s H20 processors designed specifically for the Chinese market.

Nvidia reportedly told partners to halt H20-related manufacturing work following these developments. The Wall Street Journal cited sources familiar with the situation.

The semiconductor giant hasn’t directly addressed H20 production reports. Company representatives previously stated they constantly adjust supply chains based on market conditions.

Zero China revenue likely contributed to second-quarter results despite reversed export controls. However, analysts expect H20 revenue inclusion to benefit second-half guidance.

Nvidia seeks U.S. approval to sell more advanced AI chips than the H20 in China. This potential catalyst could unlock future growth opportunities.

Analyst Upgrades Signal Confidence

Stifel boosted its price target to $212 from $202 while maintaining a Buy rating. The firm cited resumed July H20 shipments and accelerating GB300 infrastructure demand.

William Blair analyst Sebastien Naji expects another “beat-and-raise quarter powered by volume deployments of Blackwell GPUs and NVL72 racks.”

Supply chain discussions indicate ramping GB300 orders through year-end alongside sustained GB200 demand. These next-generation processors offer 50% higher FP4 performance than previous models.

UBS projects second-quarter revenue reaching $46 billion with third-quarter guidance potentially hitting $57 billion including China sales.

Three key investor concerns remain: hyperscaler demand sustainability, China export restriction impacts, and possible margin pressure during early GB300 production ramps.

Market Position Remains Strong

Stifel believes Nvidia’s AI infrastructure leadership stays unchallenged despite geopolitical headwinds. The company’s technological advantages continue attracting enterprise customers globally.

Other chip stocks showed mixed premarket action with AMD falling 0.7% and Broadcom dropping 0.5%.

Recent product launches include Spectrum-XGS Ethernet technology connecting dispersed data centers into unified AI computing facilities.

Evercore ISI previously raised its target to $214 from $190 on continued AI leadership expectations.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants