Stock: Jensen Huang’s $4 Trillion AI Prediction Sparks Investor Interest")

TLDR

- JPMorgan reiterates Overweight rating with $215 price target following company meetings

- Q2 revenue hits $46.7 billion, beating analyst expectations by $510 million

- Blackwell Ultra chips represent 50% of product mix as demand exceeds supply

- CEO projects $4 trillion AI infrastructure spending through 2030

- Stock trades at 38.7 forward P/E ratio, below historical 60.6 average

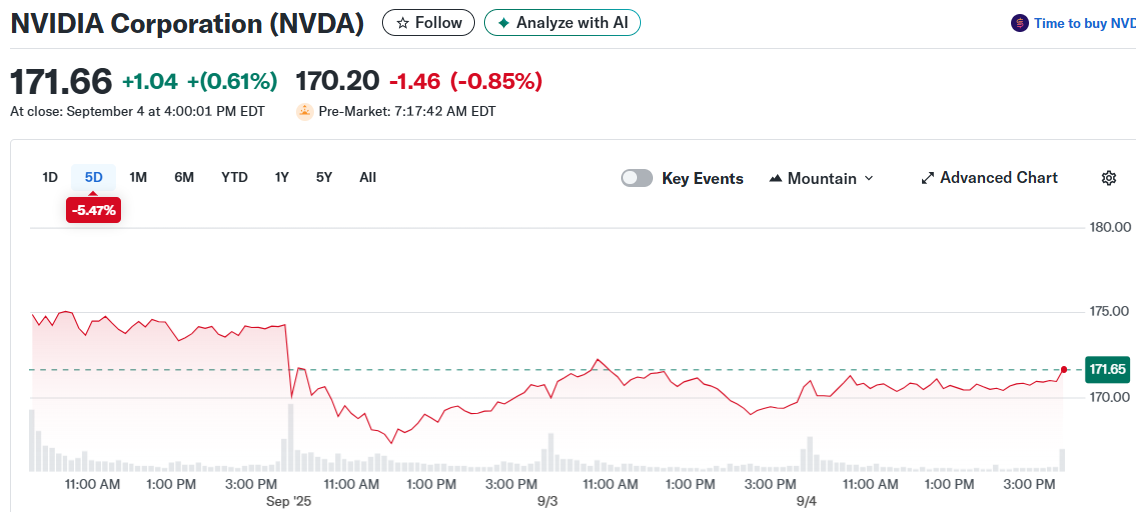

Nvidia stock continues attracting Wall Street support as JPMorgan reaffirmed its Overweight rating with a $215 price target. The investment bank’s confidence follows meetings with company executives about ongoing demand trends.

The AI chipmaker reported second-quarter revenue of $46.74 billion, surpassing analyst expectations of $46.23 billion. Earnings per share of $1.05 also beat the $1.01 consensus estimate.

Data center revenue drove 88% of total sales as customers ramp AI infrastructure investments. Lead times remain stretched at “quarters, not months” despite increased production capacity.

Blackwell Ultra chips now account for approximately 50% of Nvidia’s Blackwell product lineup. This rapid adoption shows customers prioritizing the latest AI processing capabilities.

Strong Customer Spending Pipeline

Major cloud providers have increased their 2025 capital expenditure forecasts. Alphabet raised its capex guidance from $75 billion to $85 billion for the current calendar year.

Meta Platforms boosted the low end of its spending range from $64 billion to $66 billion. The company could deploy as much as $72 billion on infrastructure projects.

Amazon’s 2025 capex might exceed $118 billion based on recent company guidance. Microsoft allocated $88 billion in fiscal 2025 and plans higher spending this year.

These four companies alone represent over $350 billion in annual AI infrastructure investments. Nvidia stands positioned to capture significant chip-related spending given its market leadership.

CEO Jensen Huang provided longer-term perspective during the earnings call. He expects data center operators to invest up to $4 trillion on AI infrastructure between now and 2030.

Next-Generation Technology Development

The company confirmed its Vera Rubin platform stays on schedule for second-half 2026 launch. This timeline addresses recent market speculation about potential delays in next-generation chip development.

All six chips comprising the Vera Rubin architecture have completed tape-out at Taiwan Semiconductor. Management maintains expectations for continued growth through calendar 2026.

The upcoming Rubin platform could deliver 3.3 times more performance than current Blackwell Ultra processors. This improvement targets emerging AI applications requiring increased computational power.

Gaming revenue provided upside surprise at $4.3 billion, well above market forecasts. This diversification helps reduce concentration risk from data center sales.

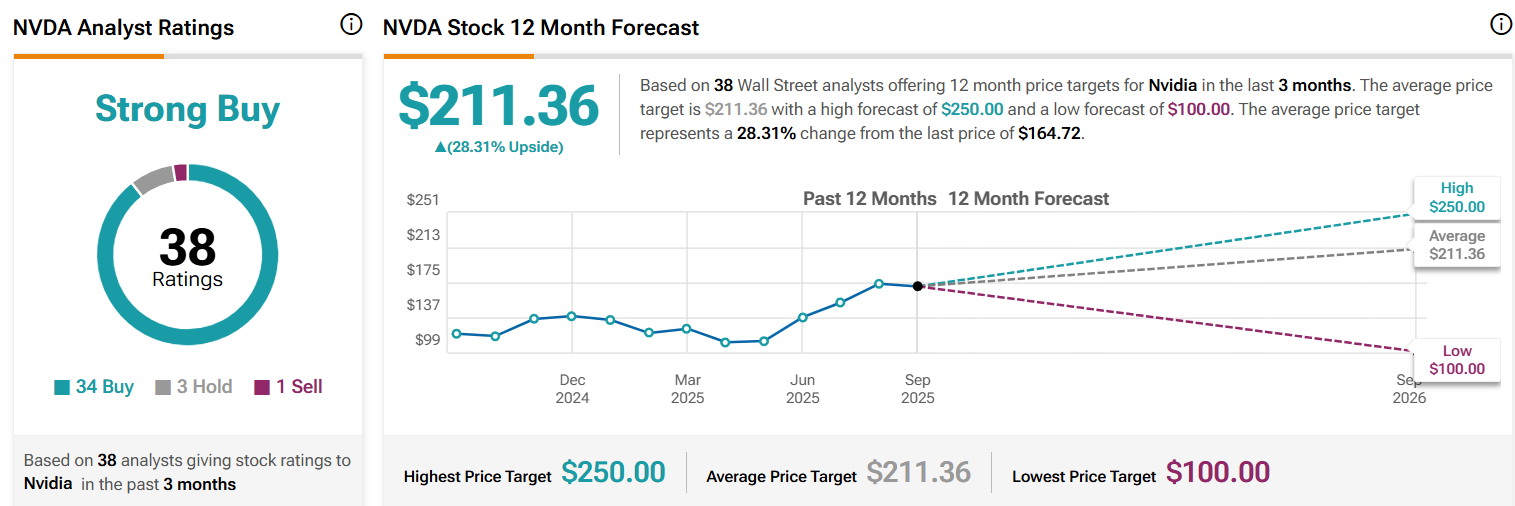

Wall Street analysts project fiscal 2026 earnings of $4.48 per share, putting the stock at a forward P/E of 38.7. Several firms increased price targets following the earnings beat, with Craig-Hallum raising its target to $245.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants