Stock Price & Analysis: Can Bulls Defend $175 as China Worries Return?")

TLDR

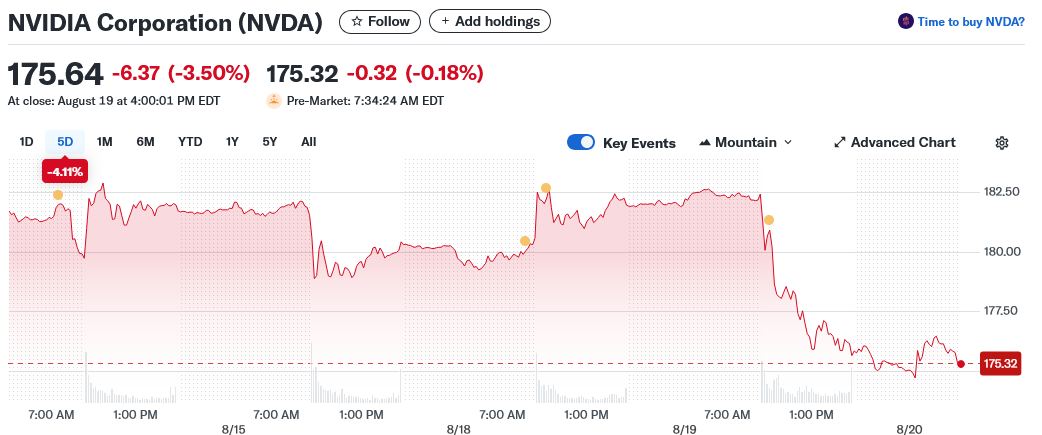

- Nvidia stock fell 3.5% to $175.64 as investors worry about China export restrictions and unclear chip strategy

- KeyBanc warns Nvidia may guide below Wall Street expectations for next quarter due to China uncertainty

- Record trading volume of $32.93 billion marks the highest turnover for Nvidia in 2025

- Technical indicators remain bullish with stock trading above all major moving averages

- KeyBanc raised price target to $215 while expecting strong underlying GPU supply growth of 40% in recent quarter

Nvidia shares dropped 3.5% to $175.64 on Tuesday as investors grappled with renewed uncertainty over the company’s China strategy. The decline came with record trading volume of $32.93 billion, the highest turnover for Nvidia stock in 2025.

The selling pressure reflects growing anxiety about potential restrictions on chip exports to China. Nvidia’s internal plans for a “B30A” chip targeted at the Chinese market remain unclear.

KeyBanc Capital Markets warned that Nvidia may deliver strong July-quarter earnings but guide below Wall Street expectations for the October quarter. The brokerage expects Nvidia’s outlook to “exclude direct revenue from China given pending license approvals and uncertainty on timing.”

If China sales were included in guidance, KeyBanc believes it would contribute an additional $2-3 billion in revenues. This would come from H20 chips and the RTX6000D (B40) products.

Despite the U.S. lifting certain AI chip restrictions, analysts expect Nvidia to take a cautious stance. The company recently resumed exports of its H20 chips to China, providing some stability.

However, ongoing discussions in Washington about tightening export controls have reintroduced downside risk. KeyBanc flagged “a potential 15% tax on AI exports and pressure from the China government for its AI providers to use domestic AI chips” as additional headwinds.

Strong Technical Foundation Remains Intact

Despite Tuesday’s decline, Nvidia’s technical picture remains healthy. The stock continues trading above its 50-day ($165.22), 100-day ($151.76), and 200-day ($137.07) moving averages.

Momentum indicators show bullish consolidation. The MACD remains positive at 5.15, while the RSI reads 64.68, neither overbought nor oversold.

Support is expected near $173.70, aligned with short-term moving average clusters. Resistance stands around $183.16, followed by a stronger ceiling near $190.

The elevated trading volume points to institutional repositioning ahead of earnings. Much of this activity appears driven by high-frequency and options-based strategies.

Supply Growth Continues Despite Headwinds

KeyBanc highlighted strong underlying drivers for Nvidia’s business. GPU supply grew 40% in the recent quarter and is projected to increase another 20% in the current quarter.

The growth comes from the ramp of Nvidia’s Blackwell (B200) chips. The newer Blackwell Ultra (B300) is set to begin shipping in the October quarter.

Blackwell Ultra could represent half of all Blackwell shipments. Rack production is also improving as manufacturing yields approach 85%.

KeyBanc believes rack shipments are on track to exit the fourth quarter at 15,000-17,000 racks. Full-year rack shipments are tracking closer to 30,000 versus prior estimates of 25,000.

The brokerage reiterated its Overweight rating and raised its price target to $215 from $190. Nvidia reports quarterly results on August 27.

Analysts expect the base-case scenario points toward recovery in the $195-$205 range in coming weeks. This assumes no major escalation in U.S.-China trade tensions and constructive updates on chip deliveries in the next earnings release.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants