TLDR

- Oil prices plunged over 4% on Monday as diplomatic talks between the US and Iran reduced fears of supply disruptions in the Middle East.

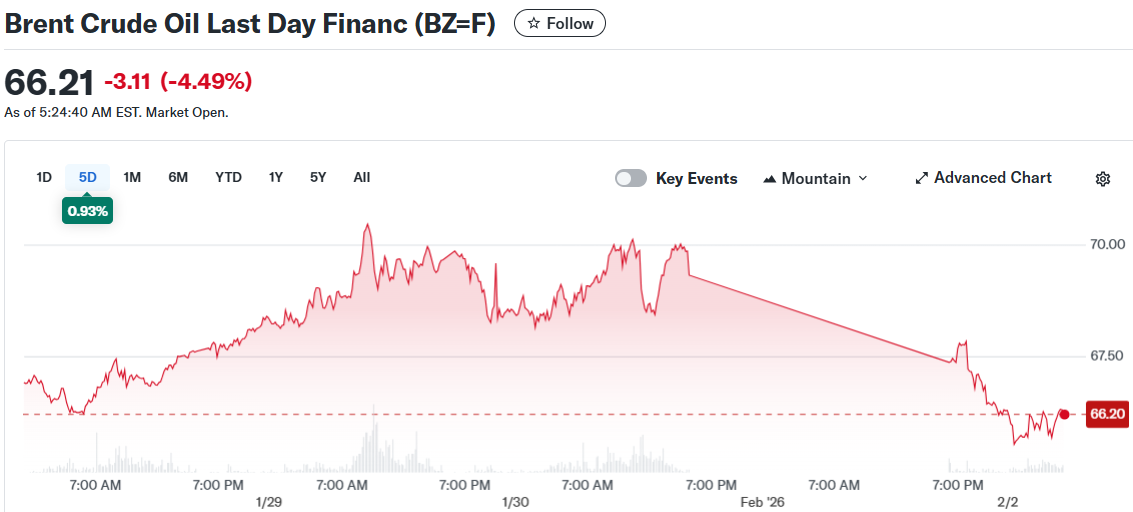

- Brent crude fell 4.6% to $66.10 per barrel while WTI crude dropped 4.7% to $60.92 per barrel during Monday’s trading session.

- President Trump confirmed Iran is engaging in serious negotiations with Washington, easing tensions after weeks of military threats.

- OPEC+ decided Sunday to keep oil production unchanged for March with no guidance on future output plans.

- A rallying US dollar and profit-taking after oil hit six-month highs last week contributed to Monday’s price decline.

Oil markets experienced sharp declines on Monday following reports of diplomatic engagement between Washington and Tehran. The price drop reversed recent gains that pushed crude to six-month highs.

Brent crude futures slid 4.6% to $66.10 per barrel in Monday’s session. West Texas Intermediate crude tumbled 4.7% to $60.92 per barrel. The losses reflected changing market sentiment about Middle East supply risks.

President Trump told reporters Iran was “seriously talking” with his administration during weekend comments. Iranian officials had previously confirmed they were preparing for negotiations with the United States. The diplomatic opening reduced market anxiety about potential military confrontation in the region.

Trump had threatened military strikes against Iran over its nuclear program in recent weeks. The US deployed naval forces to the Middle East region. These actions drove oil prices higher as markets priced in supply disruption risks.

Geopolitical Risk Premium Fades

The possibility of US-Iran dialogue removed geopolitical risk premium from crude markets. Traders had been factoring in potential strikes on Iranian oil facilities or wider regional instability. ANZ analysts said the diplomatic news lowered immediate concerns though military presence in the area continues growing.

Oil had rallied to August 2025 levels last week. Severe winter weather in North America and a Kazakhstan production disruption had also lifted prices. Monday’s selloff included profit-taking from traders after those recent gains.

The US dollar strengthened following Trump’s nomination of Kevin Warsh for Federal Reserve Chairman. Currency strength pressured dollar-denominated commodities by making them costlier for foreign buyers. This added to downward momentum in oil markets.

OPEC+ Maintains Current Output

The Organization of Petroleum Exporting Countries and allies convened Sunday for their regular policy meeting. Members agreed to maintain existing oil production levels for March. The group provided no signals about future production decisions.

OPEC+ had raised output by approximately 2.9 million barrels per day through 2025. The cartel announced an indefinite halt to further increases last November. Crude prices had dropped around 20% over the prior year before last week’s surge.

The absence of forward guidance suggests uncertainty about global economic conditions and geopolitical developments. OPEC+ appears to be monitoring market conditions before committing to policy changes.

Fundamentals Return to Focus

TD Securities commodity strategist Ryan McKay indicated additional price weakness could emerge. He suggested this would happen if declining geopolitical risks meet softening market fundamentals. Concerns about weak global demand and potential supply gluts have pressured oil throughout 2025.

The wider commodities sector also faced selling pressure on Monday. Synchronized declines across commodity markets amplified oil’s losses. Market attention shifted from supply threats back to demand trends and inventory levels.

The diplomatic breakthrough between the US and Iran changes the narrative for crude markets. Weather issues and geopolitical tensions had temporarily overshadowed demand weakness. Negotiations now refocus traders on underlying market fundamentals and economic data.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants