Stock: Why This Nuclear Energy Company Just Got a 29% Upgrade")

TLDR

- Bank of America initiated coverage on Oklo with a Buy rating and $92 price target, representing 29% upside potential

- BofA analyst believes Oklo is well-positioned for AI energy demands with 14 gigawatts in pipeline agreements

- Stock jumped 6% today following the bullish analyst coverage, continuing its massive 924% gain over the past year

- UBS previously issued a neutral rating with $65 price target, showing mixed analyst sentiment

- Company still lacks Nuclear Regulatory Commission licensed reactor design, making it a higher-risk investment

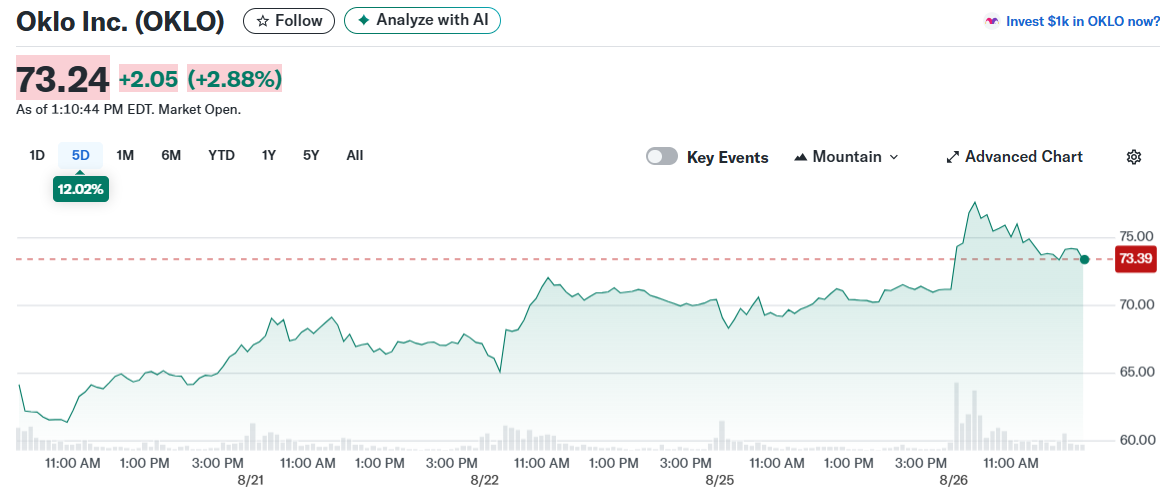

Oklo stock climbed 6% today after Bank of America Securities initiated coverage with a Buy rating and $92 price target. The nuclear energy company closed at $71.19 yesterday, making the analyst’s target a 29% upside call.

Bank of America analyst Dimple Gosai based her bullish outlook on Oklo’s positioning for artificial intelligence energy demands. She highlighted the company’s pipeline of memoranda of understanding totaling approximately 14 gigawatts.

The analyst praised Oklo’s build-own-operate business model despite its capital-intensive nature. BofA believes this approach allows the company to deliver “fully wrapped, bankable PPAs” while capturing full independent power producer economics.

BofA projects Oklo’s first 75 MW projects could achieve roughly 13% unlevered internal rate of return. Later deployments could reach 26% IRRs as the company benefits from design repetition and supply chain scale.

The investment bank estimates Oklo could achieve over 60% EBITDA margins at scale. This would far exceed peers who typically see mid-teen margins in the sector.

Mixed Analyst Views

Not every analyst shares BofA’s enthusiasm for the small modular reactor developer. UBS initiated coverage last week with a neutral rating and $65 price target.

The divergent price targets reflect the speculative nature of investing in Oklo. Analyst targets currently range from $14 to $90 across Wall Street firms.

Oklo still lacks a design licensed by the Nuclear Regulatory Commission. This regulatory hurdle represents a key risk factor for potential investors.

Financial Performance and Position

The company has posted a 924% return over the past year according to recent data. Oklo maintains a strong balance sheet with more cash than debt.

The company’s current ratio stands at 71.27x, indicating strong liquidity. This financial cushion provides runway as Oklo works toward commercialization.

Recent Developments

Oklo was recently selected for three U.S. Department of Energy reactor pilot projects. The company and its subsidiary Atomic Alchemy will lead or manage these initiatives.

The projects are part of the Reactor Pilot Program aiming to demonstrate criticality in test reactors by July 4, 2026. This government backing provides validation for Oklo’s technology approach.

Oklo has also established a digital monitoring room at its headquarters with ABB. The facility serves as an operator training and simulation center using advanced automation features.

BofA’s price target uses an 80/20 blend of peer multiples and discounted cash flow methodology. The firm identified several risks including licensing delays, slower power purchase agreement conversions, and HALEU supply challenges.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants