Stock: Co-Founder Snaps Up $2M Despite Margins Under 10%")

TLDR

- Opendoor co-founder Eric Wu purchased 300,752 shares worth $2 million at $6.65 per share

- Company’s gross profit margin remains at 8.2% while cost of sales consumes 92% of revenue

- Opendoor reported net losses for four consecutive quarters despite 4% revenue growth

- New CEO plans AI-driven transformation to improve pricing and operational efficiency

- Competitors Zillow and Redfin previously abandoned iBuying due to unpredictable pricing challenges

Opendoor Technologies received a vote of confidence from within its own ranks this week. Co-founder and director Eric Wu purchased $2 million worth of stock, acquiring 300,752 shares at $6.65 each.

The purchase increases Wu’s direct ownership to nearly 1.95 million shares. Insider buying typically draws investor attention because it suggests leadership believes in the company’s future prospects.

The move comes during a challenging period for the iBuying platform. Opendoor’s latest quarterly results highlight the core problem facing the business.

Margin Problems Continue to Plague Opendoor

Revenue grew nearly 4% to $1.6 billion in the quarter ending June 30. However, gross profit actually decreased year over year, falling from $129 million to $128 million.

Gross profit margin sits at just 8.2% of revenue. This means cost of sales represents roughly 92% of the company’s top line. For an iBuying business, these costs include home purchase prices, repairs, renovations, and selling expenses.

The company reduced operating expenses by 30% to $141 million last quarter. Despite this cost cutting, Opendoor still recorded a net loss. The company has now posted losses in four consecutive quarters.

Without improved gross margins, profitability remains elusive. Even aggressive overhead reduction only helps if there’s enough gross profit to cover those costs.

Where Zillow and Redfin Failed

Opendoor faces the same challenges that drove competitors out of iBuying. Both Zillow and Redfin exited the business after struggling with unpredictable home price forecasting.

Former Zillow CEO Rich Barton stated “the unpredictability in forecasting home prices far exceeds what we anticipated.” The business model created excessive volatility for both companies.

For Opendoor to succeed where others failed, it needs consistently better pricing. This requires either finding undervalued homes or selling at premium prices. Neither strategy proves easy to execute reliably.

New Leadership Bets on AI Solutions

CEO Kaz Nejatian, who assumed the role in September, plans an AI-driven transformation. The strategy focuses on enhancing the pricing engine, automating marketing functions, and streamlining home assessments.

Whether AI can solve structural margin problems remains uncertain. Many companies investing heavily in artificial intelligence have yet to demonstrate clear returns on those investments.

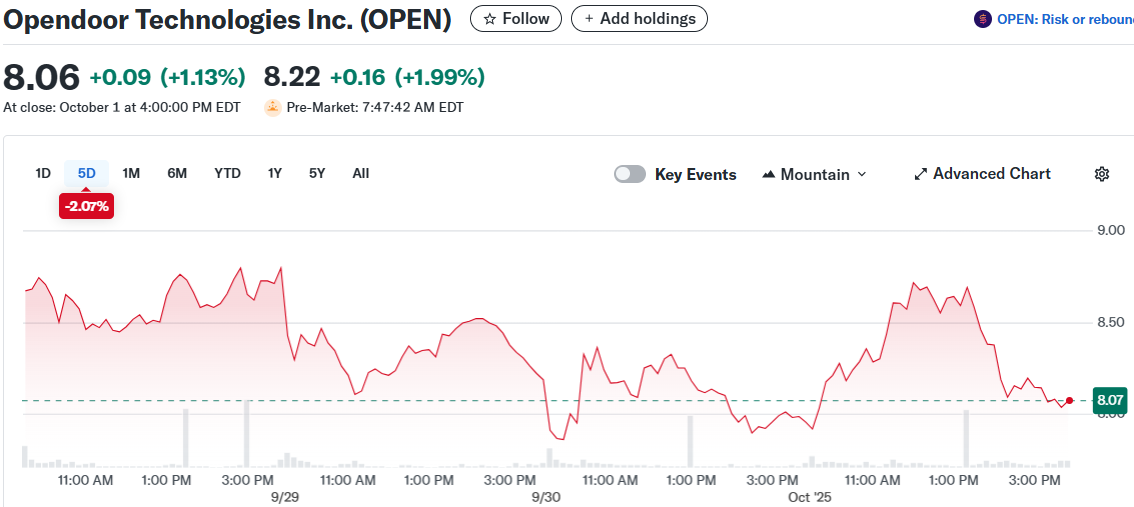

The stock has surged approximately 410% year to date through late September. This gain appears speculation-driven rather than based on improved fundamentals. Shares traded at $8.02 in after-hours trading Tuesday, up 0.63% following news of Wu’s purchase.

Wu bought shares at $6.65. The stock closed at $8.06 on October 1, already above his purchase price.

His $2 million investment signals personal confidence in Opendoor’s turnaround potential. For investors, the question remains whether operational improvements and AI integration can deliver the margin expansion necessary for sustainable profitability.

Declining mortgage rates could increase housing market activity, providing more transaction opportunities. However, volume growth alone won’t solve the fundamental margin issue if each transaction continues generating only 8% gross profit.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants