Stock Drops as Hedge Fund Manager Calls Business Model ‘Total Garbage’")

TLDR

- Hedge fund veteran George Noble slammed Opendoor as “total garbage” causing 12% stock drop

- OPEN trades at 22x enterprise value/revenue while profitable rival Compass trades at 0.9x

- Eric Jackson shifted focus to Better Home & Finance (BETR) which surged 47%

- Wall Street analysts target $1.02 price representing 88% potential downside

- Stock still up 424% year-to-date despite fundamental weaknesses

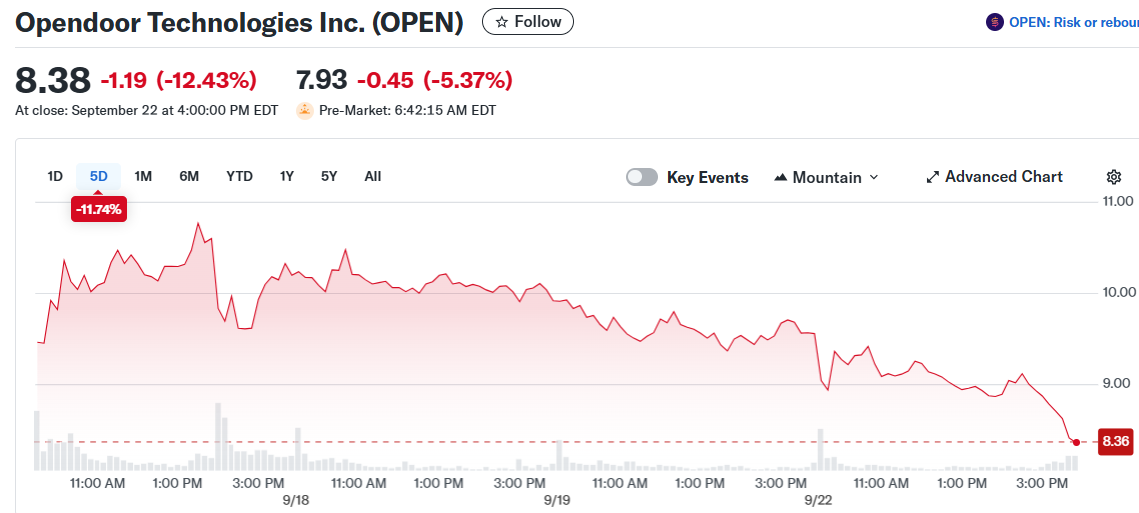

Opendoor stock plummeted 12% Monday after hedge fund manager George Noble delivered a scathing assessment of the real estate technology company. Noble, who founded two billion-dollar hedge funds and worked alongside investment legend Peter Lynch, called Opendoor “total garbage” on social media.

The brutal critique continued in Tuesday’s pre-market trading with OPEN shares falling an additional 4%. Noble’s comments targeted the company’s core business model and persistent losses since inception.

“Go ahead and speculate if you wish, but don’t DARE pretend that there is a fundamental case,” Noble warned investors. He highlighted Opendoor’s “atrocious” unit economics and questioned whether cost reduction efforts could fix fundamental problems.

Valuation Gap Exposes Market Reality

Noble drew stark comparisons between Opendoor and its competitors to illustrate his concerns. OPEN currently trades at 22 times enterprise value to revenue despite being unprofitable since launch.

Meanwhile, rival Compass trades at just 0.9 times enterprise value to revenue while maintaining profitability and a strong balance sheet. The valuation disconnect underscores Noble’s argument about speculative pricing versus fundamental value.

GuruFocus rates Opendoor as “Overvalued” with concerning financial metrics. The company carries a debt-to-equity ratio of 3.46 and negative earnings per share of -0.43. An Altman Z-score of 2.49 places the company in a gray area for potential financial distress.

Market dynamics shifted further when Eric Jackson announced his new investment in Better Home & Finance Holding (BETR). Jackson, whose July endorsement sparked Opendoor’s meme stock rally, compared BETR to “Shopify for mortgages.” BETR shares exploded 47% higher following his endorsement.

Wall Street Maintains Bearish Outlook

Professional analysts remain skeptical despite Opendoor’s 424% year-to-date gains. Wall Street consensus shows a Moderate Sell rating based on one Buy, two Hold, and five Sell recommendations.

The average analyst price target of $1.02 suggests potential downside of 88% from current levels. This bearish outlook aligns with Noble’s fundamental concerns about the business model.

Real estate sector consolidation adds pressure with Compass acquiring Anywhere Real Estate for $4.2 billion. The move highlights competitive challenges facing Opendoor’s technology-first approach.

Some positive indicators exist including insider purchases of over 481,000 shares in recent months. The company’s Beneish M-Score suggests low probability of earnings manipulation.

However, Opendoor’s price-to-book ratio of 9.74 sits near five-year highs while the company continues burning cash. The disconnect between valuation and fundamentals supports Noble’s harsh assessment.

Trading volumes remained elevated as investors digested the criticism from the veteran fund manager. Noble’s track record and direct approach carried weight with institutional investors reassessing their positions.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants