Stock: Why This Real Estate Play Keeps Climbing Higher")

TLDR

- Opendoor President Shrisha Radhakrishna bought $128,340 worth of OPEN stock in late August, purchasing 30,000 shares

- OPEN stock jumped 11.3% on Tuesday due to retail investor interest and social media buzz around the “meme stock”

- The company reported Q2 revenue of $1.57 billion, beating estimates with positive adjusted EBITDA of $23 million

- Wall Street analysts maintain a “Hold” rating with price targets well below current trading levels

- Stock has gained 223% year-to-date and hit new 52-week highs at $5.14 per share

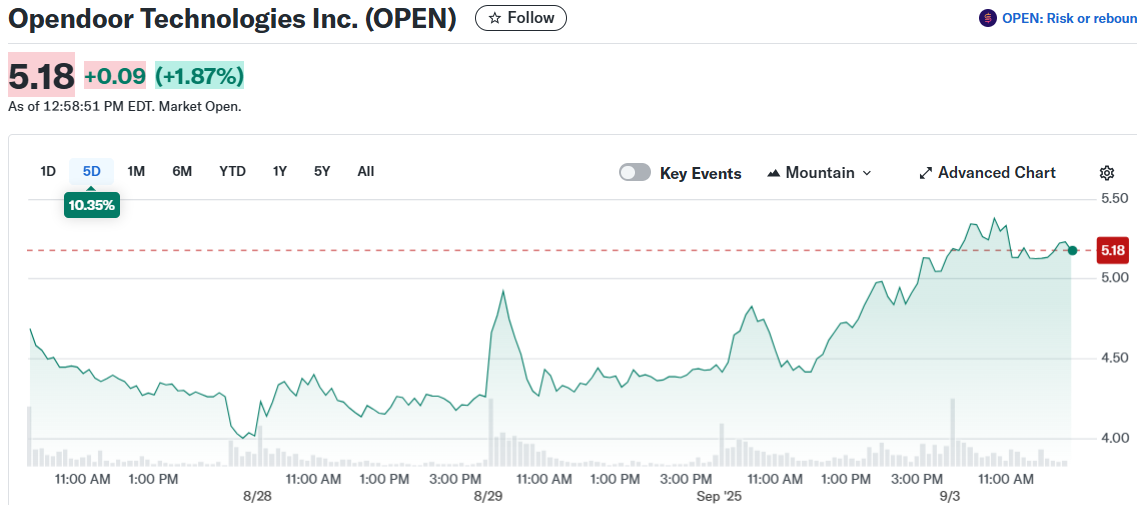

Opendoor stock surged 11.3% on Tuesday as retail investors piled into the digital real estate company following insider purchases and social media attention. The stock closed at $5.14, marking a new 52-week high.

The rally gained momentum after President Shrisha Radhakrishna purchased approximately $128,340 worth of OPEN shares in late August. He bought 28,400 shares at $4.27 and 1,600 shares at $4.42, bringing his total direct ownership to about 4.28 million shares.

The insider buying followed the departure of former CEO Carrie Wheeler. Radhakrishna’s purchase was viewed by traders as a vote of confidence in the company’s new direction.

Social media activity helped fuel Tuesday’s gains. Hedge fund manager Eric Jackson, who previously called OPEN a potential “100-bagger,” posted on X that he might meet with Opendoor’s management this week.

The stock has become popular among retail traders partly due to its high short interest. About 24.64% of available shares are sold short, making it a target for traders betting against short-sellers.

Second Quarter Results Show Progress

Opendoor reported Q2 2025 revenue of $1.57 billion, representing a 5% year-over-year increase and beating Street estimates. The company sold 4,299 homes and acquired 1,757 during the quarter.

Adjusted EBITDA turned positive at $23 million, marking an inflection point after several quarters of losses. GAAP net losses narrowed to approximately $29 million.

Free cash flow also turned positive at $821 million for the quarter. The company ended June with $789 million in unrestricted cash plus $396 million in restricted cash.

Opendoor completed a $325 million convertible notes exchange in May. This added fresh liquidity and extended debt maturities.

Management Sounds Cautious Note

Despite the positive Q2 results, CEO Wheeler warned of challenging conditions ahead. She noted a consistent slowing of the housing market as the quarter progressed.

Third-quarter revenue guidance sits at $800 to $875 million. Adjusted EBITDA guidance points to a negative range of roughly -$28 million to -$21 million.

This implies a sharp sequential pullback in volumes and margin pressure. The company is transitioning its business model during what Wheeler called “a historically difficult macro environment.”

Wall Street analysts remain cautious despite the recent rally. UBS raised its price target to $1.60 from $1.30 but warned it no longer assumes a return to year-over-year revenue growth in fiscal 2026.

Citigroup cut its rating to “Sell” with a $0.70 target, citing weaker guidance and higher execution risk. Keefe, Bruyette & Woods moved to “Underperform” with a $1.00 target.

The consensus “Hold” rating reflects analyst concerns about widening losses in the second half of 2025. Uncertainty around Opendoor’s platform pivot also weighs on sentiment.

The stock trades at 66x forward earnings, well above what analysts consider a fair valuation in the mid-single digits. OPEN shares have gained 223% year-to-date, far outpacing the broader market.

The stock’s extreme volatility continues, with 90 moves greater than 5% over the past year. Tuesday’s 11.3% gain represents one of the larger single-day moves for the company.

Investors who bought $1,000 worth of Opendoor shares five years ago would now hold an investment worth $462.20. The stock currently trades more than double Wall Street’s highest price target of $2.

President Radhakrishna’s recent share purchase totaled 30,000 shares and came as the company navigates both internal leadership changes and challenging market conditions in the housing sector.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants