Stock: Is This AI Selloff Creating a Contrarian Buying Opportunity?")

TLDR

- Oracle stock fell 5% in August 2025 due to leadership changes, job cuts, and broader AI market skepticism

- The company trades at 12x trailing revenues versus its four-year average of 6.5x, representing an 85% valuation expansion

- Cloud infrastructure revenue grew 52% year-over-year with $25 billion planned CAPEX for fiscal 2026

- Oracle holds a distant fourth position in cloud market with less than 5% market share behind AWS, Microsoft, and Google

- The stock has shown higher volatility than broader markets, declining 41% during 2022 inflation shock versus S&P 500’s 25% drop

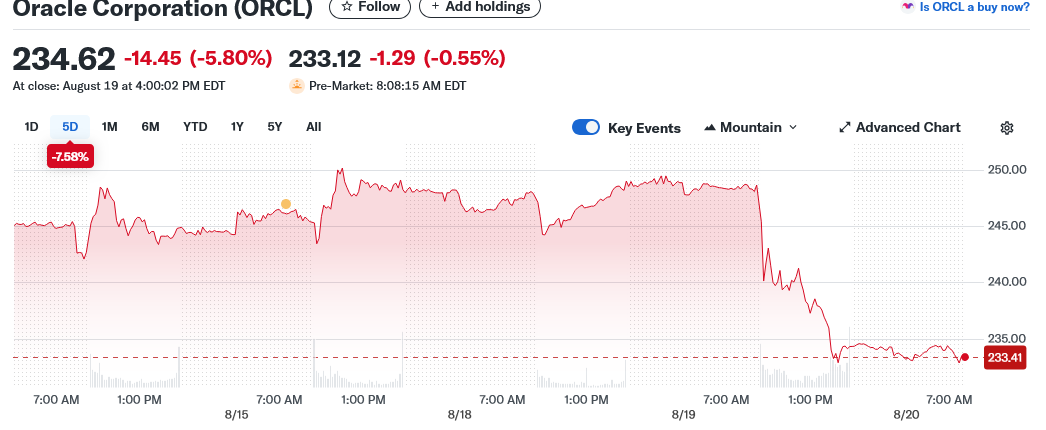

Oracle stock dropped over 5% in August 2025, creating debate among investors about whether the decline represents a buying opportunity or reflects deeper structural concerns. The database giant’s shares have surged 40% year-to-date on AI infrastructure enthusiasm but now face multiple headwinds.

The recent selloff stems from several internal and external factors. Chief Security Officer Mary Ann Davidson departed the company while job cuts hit the cloud infrastructure division. These moves raised questions about leadership stability and operational efficiency during a critical growth phase.

Broader market skepticism about AI sustainability also weighed on shares. Lukewarm reception of OpenAI’s GPT-5 models and warnings from industry leaders created doubt about the AI-driven stock rally. The technology sector grappled with whether current AI investments would translate into sustainable profits.

Oracle’s cloud infrastructure revenue grew 52% year-over-year in Q2 2025, validating its aggressive AI strategy. The company partners with OpenAI to build 4.5 gigawatts of data center capacity. Cloud consumption revenue jumped 62% in Q4 fiscal 2025, showing strong customer demand.

The job cuts, while concerning to some investors, reflect a strategic shift toward high-margin AI infrastructure. Oracle is moving resources away from slower-growth segments to focus on AI-native solutions. This pivot aligns with the company’s massive capital expenditure plans.

Oracle trades at elevated valuation metrics that raise downside risk concerns. The stock’s price-to-earnings ratio of 54.8 and PEG ratio of 3 suggest overvaluation if growth expectations aren’t met. The company now trades at 12x trailing revenues compared to its four-year average of 6.5x.

This 85% valuation expansion leaves little margin of safety for execution disappointments. Oracle has historically shown higher volatility than broader markets during stress periods. The stock declined 41.1% during 2022’s inflation shock while the S&P 500 fell 25.4%.

Competitive Position and Market Share

Oracle remains the distant fourth player in cloud infrastructure behind Amazon AWS, Microsoft Azure, and Google Cloud. Its estimated market share of less than 5% limits pricing power and market influence. This scale disadvantage could hinder long-term growth prospects.

The company faces a developer ecosystem gap that creates barriers to organic growth. Oracle’s platform has a steep learning curve for new developers compared to larger competitors. The smaller open-source ecosystem reduces viral adoption among enterprises and increases switching costs.

Oracle’s strategic differentiation lies in AI-first infrastructure development. The company deployed zettascale superclusters with over 65,000 NVIDIA H200 GPUs for complex AI model processing. Oracle Database 23ai includes vector search capabilities for AI applications.

The Oracle Cloud@Customer model brings on-premises AI capabilities to enterprises. This approach differs from AWS and Azure’s general-purpose cloud optimization strategies. Oracle bets this AI-native focus will capture growing infrastructure demand.

Financial Metrics and Investment Outlook

Oracle plans $25 billion in CAPEX for fiscal 2026, representing 37% of revenue. This exceeds the typical 15-25% range for cloud peers but reflects the capital-intensive nature of AI infrastructure. The company’s negative free cash flow of $2.92 billion in Q2 2025 highlights investment strain.

However, Oracle maintains $107.4 billion in cash reserves and $138 billion in remaining performance obligations. These provide financial cushion for the aggressive expansion strategy. The massive backlog creates execution pressure but demonstrates customer commitment.

AI demand sustainability presents future questions as buildouts may reach saturation. Model efficiency improvements could reduce compute power requirements over time. Enterprise AI spending might normalize after initial deployment phases complete.

Oracle projects cloud infrastructure revenue growth exceeding 70% in fiscal 2026. The company’s fiscal first-quarter 2026 earnings report will provide validation of these targets. Investors await concrete progress on the ambitious growth projections.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants