Stock: Director Sells $3M as Competition Concerns Mount")

TLDR

- Palantir director Alexander Moore sold $3.1 million in shares on September 2 under pre-arranged trading plan

- PLTR stock surged 107% in 2025 with 417% annual return, trading at $156.14

- William Blair maintains Hold rating despite expecting 103% commercial revenue growth next quarter

- Competition concerns emerge from OpenAI and AI startups copying Palantir’s model

- Wall Street consensus Hold with $155.39 price target indicates minimal downside

Palantir Technologies director Alexander Moore unloaded $3.1 million worth of shares this week as the data analytics stock continues its meteoric rise. The insider sale comes as analysts warn of emerging competitive threats despite strong growth prospects.

Moore sold 19,999 Class A shares on September 2 at prices between $151.56 and $157.68 per share. The transaction was executed under a Rule 10b5-1 trading plan established last November.

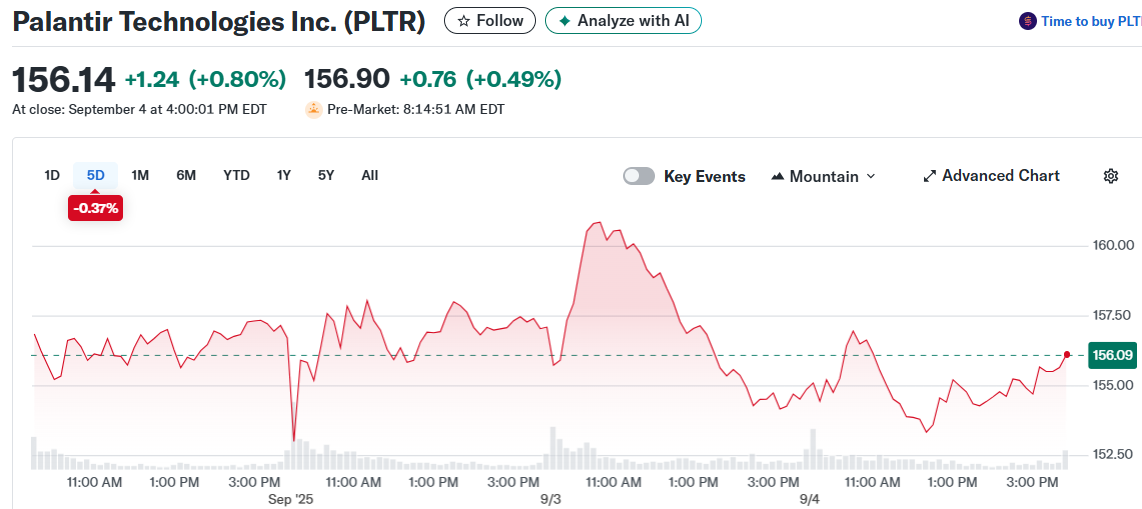

The sale reduces Moore’s direct holdings to 1,272,978 shares. PLTR currently trades at $156.14, giving the company a market cap of $367.48 billion.

Stock Performance Remains Strong

Palantir stock has delivered exceptional returns for investors. The shares jumped 107% year-to-date and posted a staggering 417% gain over the past year.

This performance has been driven by strong demand for Palantir’s AI-powered platforms. The company showcased over 70 clients at its recent AIPCon 8 event on September 4.

William Blair analyst Louie DiPalma expects the U.S. commercial business to show 103% revenue growth in the September quarter. This pace could mark one of Palantir’s strongest quarters to date.

The defense segment also remains robust with several new contracts secured this quarter. This diversified growth supports the company’s expansion strategy.

Competitive Threats Emerge

Despite strong near-term prospects, DiPalma highlighted longer-term competitive risks. OpenAI and other well-funded AI startups are aggressively targeting Palantir’s markets.

These rivals are raising large amounts of capital and recruiting talent from established players. They’re copying Palantir’s engineer-led model while pursuing both enterprise and defense contracts.

The competitive landscape in AI and data analytics continues evolving rapidly. New entrants with substantial funding could challenge Palantir’s market position over time.

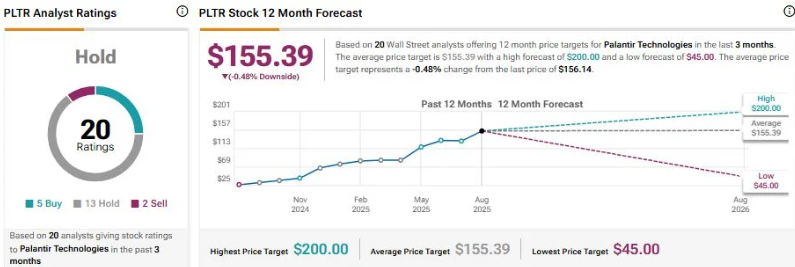

Wall Street maintains a cautious stance despite the stock’s strong performance. The consensus rating is Hold based on five Buy ratings, 13 Hold ratings, and two Sell ratings.

The average price target of $155.39 suggests minimal downside of 0.48% from current levels. Palantir has already secured several defense contracts in the September quarter while maintaining strong commercial momentum.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants