Stock: The AI Bubble Warning That Has Investors Worried")

TLDR

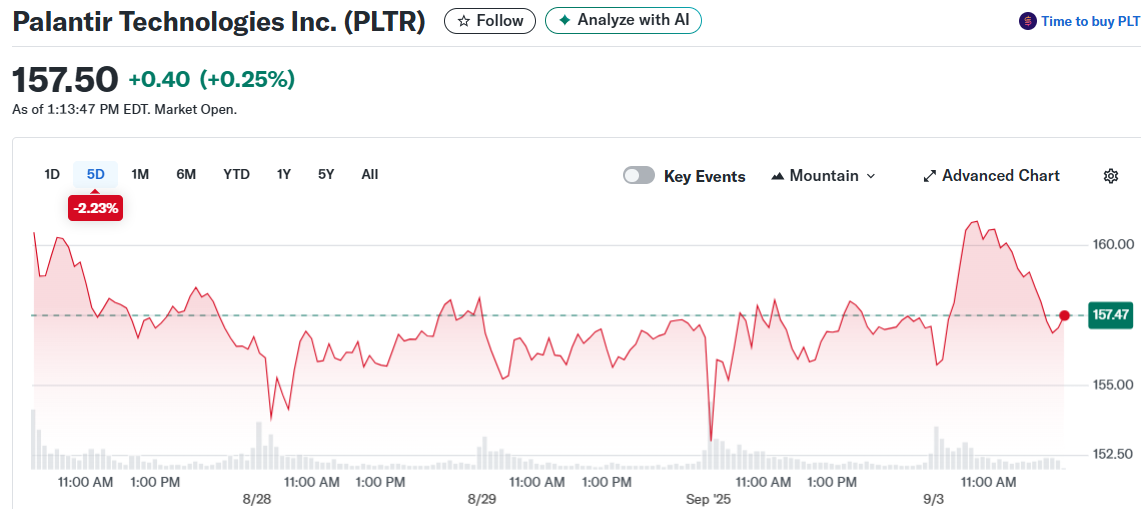

- Palantir stock has dropped 16% over three weeks despite being up over 200% year-to-date

- Company posted strong Q2 results with 48% revenue growth to $1 billion, raising full-year guidance

- Multiple Wall Street analysts raised price targets after earnings, with some reaching $200

- Federal Reserve rate cuts and AI market bubble concerns are weighing on high-multiple tech stocks

- Stock trades at extremely high valuations of 90x revenue and 245x earnings, creating downside risk

Palantir Technologies has experienced a 16% decline over the past three weeks. The drop comes despite the AI software company remaining up over 200% year-to-date.

The pullback reflects broader market concerns about high-multiple technology stocks. Federal Reserve hints about September rate cuts have surprisingly worked against AI names like Palantir.

Smaller companies appear more attractive to investors betting on lower borrowing costs. The market rotation has also affected other AI leaders, with Nvidia down nearly 7% over recent weeks.

Strong Earnings Drive Analyst Optimism

Palantir delivered impressive second-quarter results that exceeded expectations. Revenue grew 48% year-over-year to reach $1 billion for the first time.

The company raised its full-year revenue guidance substantially. New projections range from $4.14 billion to $4.15 billion, up from the previous forecast of $3.89 billion to $3.90 billion.

Adjusted operating margins expanded to 48% from 37% in the prior year quarter. The improvement demonstrates the company’s ability to scale its software business profitably.

Government business proved particularly strong during the quarter. U.S. government segment revenue jumped 53% year-over-year to $426 million.

Wall Street analysts responded enthusiastically to the results. Citigroup raised its price target to $177 from $158, citing “show-stopping” performance.

Piper Sandler increased its target to $182 from $170. The firm pointed to strong demand from both government and commercial customers.

Wedbush took the most aggressive stance, lifting its price target to $200 from $160. The firm highlighted demand for Palantir’s Artificial Intelligence Platform as the key driver.

Market Concerns Cloud the Outlook

OpenAI CEO Sam Altman recently warned about potential AI market overexcitement. He compared current conditions to the dot-com bubble of the late 1990s.

While Altman still believes in AI’s long-term potential, his comments have added caution to investor sentiment. The remarks come as many AI stocks trade at elevated valuations.

Palantir faces particular valuation concerns given its current multiples. The stock trades at roughly 90 times forward revenue and 245 times forward earnings.

These metrics leave little room for execution mistakes or growth disappointments. High-multiple growth stocks typically face sharp selloffs during economic uncertainty.

Government contract revenues can be unpredictable and lumpy in nature. Budget changes or shifting priorities could impact future growth trajectories.

The commercial market presents scaling challenges for Palantir’s complex software. Large implementation costs and lengthy sales cycles may limit expansion beyond enterprise customers.

Not all analysts share the bullish consensus on Palantir stock. Andrew Left from Citron Research considers the stock wildly overvalued at current levels.

The mixed analyst sentiment reflects the stock’s polarizing nature. Some see revolutionary AI software while others question sustainability at these valuations.

Recent trading activity shows daily volumes of around 1.3 million shares. The stock has traded in a 52-week range from $29.31 to $190.00.

Current market capitalization stands at $373 billion based on the latest share price. The company maintains gross margins above 80%, reflecting its software-focused business model.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants