Stock: Shares Jump After E-commerce Giant Crushes Q2 Expectations")

TLDR

- PDD Holdings beat Q2 earnings expectations with 22.07 yuan per ADS vs 15.53 yuan expected

- Revenue rose 7% year-over-year to 103.98 billion yuan, beating analyst estimates of 102.7 billion yuan

- Stock rallied over 3% in early trading following the earnings announcement

- Operating profit declined 21% and net income fell 5% compared to last year

- Company faces challenges from intense competition and sluggish Chinese consumer spending

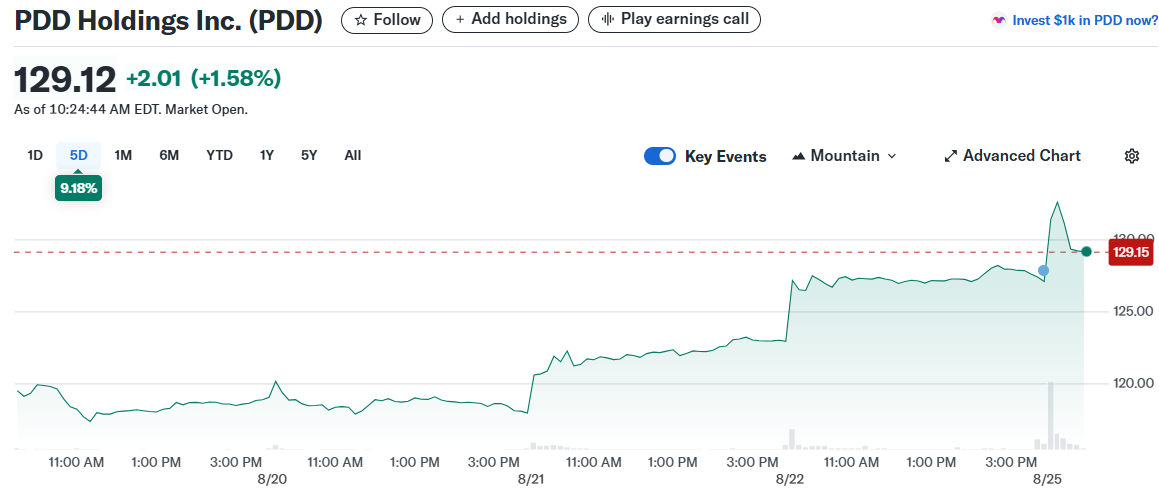

PDD Holdings shares jumped in Monday trading after the Temu parent company delivered second-quarter results that topped Wall Street expectations. The stock climbed more than 3% to 130.62 in early trades.

The Chinese e-commerce giant reported adjusted earnings of 22.07 yuan per American depositary share for the June quarter. This figure came in well above the 15.53 yuan per ADS that analysts surveyed by FactSet had predicted.

Revenue growth also exceeded forecasts, rising 7% year-over-year to 103.98 billion yuan or $14.5 billion. Analysts had estimated revenue of 102.7 billion yuan for the period.

The earnings beat provided a bright spot for investors despite broader challenges facing the company. PDD’s adjusted earnings were down 5% from the same quarter last year, showing the pressure on profitability.

Profitability Under Pressure

Operating metrics revealed the company’s ongoing investment strategy is weighing on margins. Non-GAAP operating profit decreased 21% year-over-year to 27.75 billion yuan in the quarter.

Net income attributable to shareholders fell 5% to 32.71 billion yuan compared to the same period in 2024. The declines reflect PDD’s continued spending on merchant support and platform improvements.

PDD operates both the Pinduoduo platform in China and the international Temu marketplace. The domestic business continues to face headwinds from weak consumer spending in China.

Temu encounters its own set of challenges in international markets. The elimination of the de minimis tariff exemption for small imports poses a particular concern for the platform’s business model.

The de minimis provision ends this week for all packages entering the United States. This policy change expands beyond just parcels from China and Hong Kong to affect all international shipments.

Growth Momentum Slowing

PDD’s revenue growth has decelerated from the rapid expansion seen during Temu’s breakout period. The company posted 86% growth in early 2024, followed by 44% and 24% in subsequent quarters.

First quarter growth slowed to 10% before the current 7% rate. This trend reflects the maturing of Temu’s international expansion and intensifying competition in both markets.

“Revenues growth further moderated this quarter due to intense competition,” said Jun Liu, PDD’s VP of Finance. The company remains focused on long-term value creation over short-term profits.

Revenue from online marketing services increased 13% to 55.70 billion yuan during the quarter. Transaction services revenue stayed relatively flat at 48.28 billion yuan.

Total operating expenses rose 5% to 32.33 billion yuan, driven primarily by higher sales and marketing costs. These investments support the company’s merchant ecosystem development efforts.

Lei Chen, Chairman and Co-CEO, highlighted progress in platform sustainability. “We continued to invest in merchant support initiatives and are encouraged by the progress made towards a healthier platform ecosystem,” Chen stated.

Year-to-date, PDD stock has gained 31.7% including a 12% rally in August. However, shares remain down 9% compared to twelve months ago, showing the volatile nature of the stock’s performance.

The company maintains strong technical ratings with an IBD Composite Rating of 89 out of 99. Its Relative Strength Rating stands at 56, indicating outperformance versus 56% of stocks over the past year.

PDD’s latest results demonstrate the company’s ability to exceed earnings expectations while navigating competitive pressures in both domestic and international markets.

Get 3 Free Stock Ebooks

Discover top-performing stocks in AI, Crypto, and Technology with expert analysis.

- Top 10 AI Stocks - Leading AI companies

- Top 10 Crypto Stocks - Blockchain leaders

- Top 10 Tech Stocks - Tech giants